This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

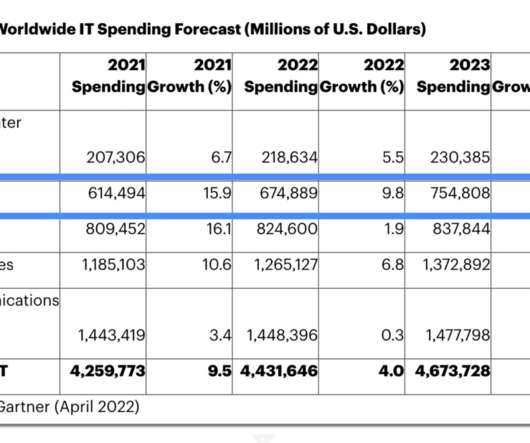

So follow AWS, Azure and Google Cloud. Let’s look a whole level up to the real canaries-in-the-coalmine: AWS, Azure and Google Cloud. And Gartner is still predicted SaaS purchase rates will accelerate in 2023 : AWS, Azure and Google Cloud say Yes. Enterprise software spending globally was $529B in 2020, per Gartner.

But are AWS, Azure and Google Cloud just too big for us to learn from? NPS up +13 points in 2020. Google Cloud continues its march upmarket, competing with Azure. AWS vs. Azure vs. Google Cloud is one of the greatest case studies of all time. Zoom certainly hasn’t been wounded by the revival of Google Meet.

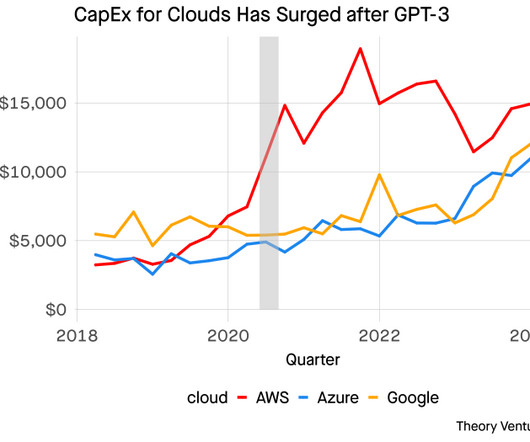

Cloud Capex in Q1 AWS $14 billion Azure $14 billion Google Cloud $12 billion These are not one-time investments, but part of a broader trend that started to occur after the introduction of GPT 3 in mid-2020 Amazon was the first to invest significantly.

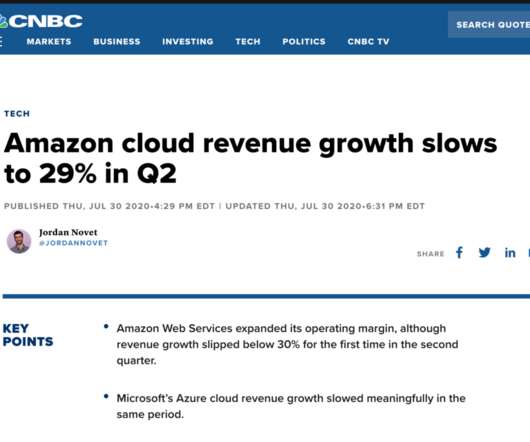

But they also both warned of potential lower growth during the rest of 2020. Azure and Google Cloud also saw growth begin to slow. And that economy has taken the steepest fall in history. This week there were 2 quiet flags. Amazon/AWS and Atlassian both had huge Q2’s. The same with Atlassian. It could just be a bump.

Growth in public cloud services (AWS, Azure, Google Cloud, Snowflake, etc.) As compared to late 2020 and 2021, when change was the name of the game. will grow the fastest at 20.4%, and price increases and increased utilization at existing vendors will consume a significant amount of that growth.

Reaccelerated growth to 29% after a rough 2020 of 4+ flat quarters. Many Cloud leaders took an initial hit from Covid, but C3 had a tough 2020 overall. Partners are key — Baker Hughes (a customer and partner) makes up a massive 30% of revenue, and claim Microsoft Azure has contributed $200m in total bookings.

2020 is the decade of data. Look no further than the massive companies pushing the public & the private market forward: Snowflake, Databricks, Amazon, Azure, Google Cloud. It’s quite possible that data products have created more market cap than any other subsegment of SaaS in the last five years.

Focusing on smaller developers, in some ways it’s been a bit overshadowed by AWS, Azure, and Google Cloud. From so-so NRR (101% in 2020) to Top-Tier for SMBs (116%) in 2 years. DigitialOcean doesn’t want to take AWS, Azure and Google on in the enterprise and doesn’t really try.

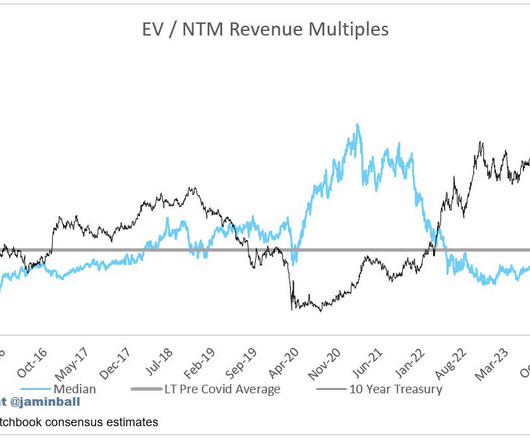

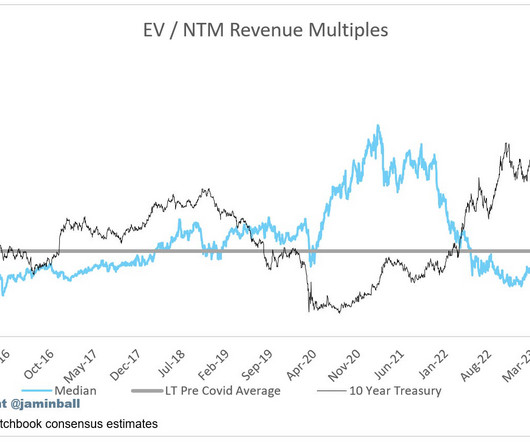

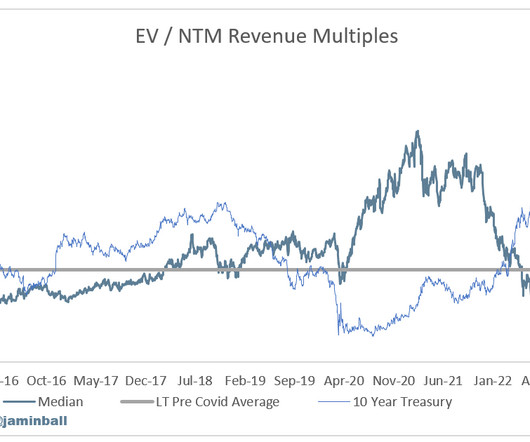

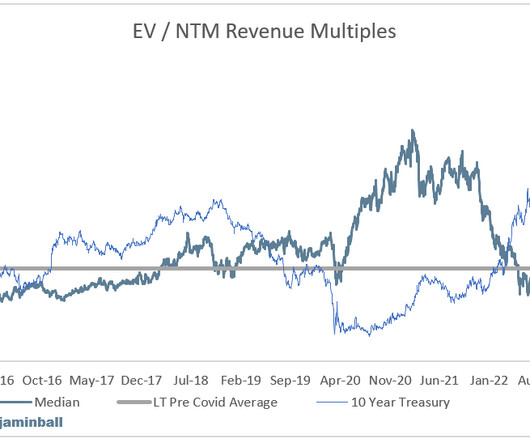

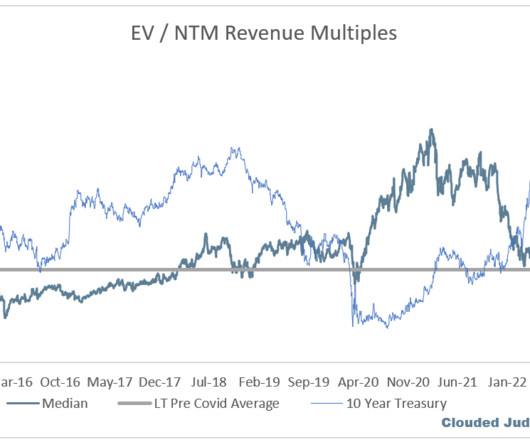

It’s worth pointing out that Azure is a bit above the long term trendline, while AWS is still below (but accelerating up). It’s worth pointing out that Azure is a bit above the long term trendline, while AWS is still below (but accelerating up). The graph below shows the median net retention going back to 2020.

Amazon AWS, Microsoft Azure and even Google Cloud are on fire, adding insane amounts of revenue this year. With revenue multiples higher than pre-March 2020 but lower than the peak: I don’t see too many folks arguing the Bull Case, but they should be. Customers are buying more than ever. It’s not all tough news, folks.

After polling CIOs, Gartner found that total SaaS spend will grow from $100B in 2020 to $140B in 2022: A few interesting implications and learnings: The growth in SaaS buying should give you a +20% a year boost on top of your other sales and marketing efforts. But that’s just the start. This is your time, folks. Go make it happen.

We all know 2020 and 2021 was the year of excessive software buying fueled by ZIRP. The hyperscalers (AWS, Azure, GCP) are always some of the first companies to report earnings during earnings season (coming up in 2 weeks), and there’s always a read through for consumption names (meaning people believe there’s a correlation).

For fiscal 2022, large customers represented 61% of total revenue compared to 54% of total revenue in 2021 and 46% in 2020… Overall NDR fell, but enterprise spending remains steady. Yesterday, Cloudflare announced earnings. I’m adding Cloudflare to the list of tracked companies for this series.

What you’ll see in that cloud spend box is actually Gartner’s 2020 estimate for infrastructure as a service spending for companies, which was $50 billion. And IDG just recently released the 2020 Cloud Computing Survey that showed over one third of IT budgets are spent on cloud computing technologies.

Here’s what makes NP Digital one of the best analytic companies in 2020: Founder expertise – Neil Patel is a rockstar in the digital marketing world, having started out in the space in 2001 as a teenager. Known as their “AI Factory”, Artefact also works with cloud service providers like Azure to ensure they have a robust infrastructure.

We now have results from the three hypersclaers (AWS / Azure / GCP). This is lower than Q1 2020 (right at the onset of Covid) when everyone seemed to guide lower given the unknowns of Covid. Subscribe now Cloud Giants Report Q1 + Early Look at Software Results Q1 earnings seasons has officially kicked off!

In a 2020 survey, 22% purchased software through a cloud marketplace versus 60% in 2021. The role of AWS, Azure, and Google Cloud Marketplace is becoming increasingly important. “45% Some call this the ‘ecommercization of software,’ and this trend signals a highly disruptive shift in how we go to market with software.

For context on a 10Y at 5% - from 2010 to 2020 the 10Y averaged roughly ~2.5%. Said another way, the 10Y today is double what it averaged from 2010 to 2020. Hyperscaler Preview Next week Amazon, Microsoft and Google report earnings and we’ll see Q3 data for AWS, Azure and Google Cloud.

But, spoiler alert, most of those improvements were already in the 20H2 release (Windows 10 October 2020 Update) edition. Or, if you want more control and features, there's Windows 365 Enterprise or Azure Virtual Desktop. My reasoning was that it came with compatibility problems and really added nothing to Windows 10.

It looks at the YoY dollar change in quarterly revenue from the hyperscalers (just looking at Azure / AWS because the data goes back further) going back a few years. If you look at the historical data you’ll see there’s a very clear trendline through the end of 2020. This is the data point shown for Q4 ‘23.

Investment in cybersecurity companies has increased more than thirteenfold since 2011, and despite the COVID-19 pandemic, 2020 was a record year for cybersecurity with over $7.8 Just over halfway into 2021, 2020’s record has already been blown out of the water, with another $11 billion invested thus far. Headquarters: Dallas, Texas.

Can you believe that it’s been two weeks since we wrapped up Altitude 2020? But if you’d rather get them all in one place, here are just four of the biggest product announcements from Altitude 2020. Integrations with Azure AD, Google Shared Drives, and Workday. Yeah, neither can we. Introducing BetterCloud Discover.

Since Wiz’s founding in 2020, their approach has enabled them to deploy rapidly and deliver value to their customers nearly immediately. Over the past three years of getting to know them, we have been continually floored by the relentless drive to deliver, razor sharp product instincts and velocity, and camaraderie as a team.

This growth adjusted premium also comes at a time when the 10Y is nearly double what it was from 2010 to 2020. Maybe with the exception of hyperscalers (particularly Azure). So what’s holding up software stocks valuations?? It’s actually the complete opposite - there will be more deceleration in Q4 (according to guides).

Azure / Confluent / Datadog reported a few weeks back (they all had March quarter ends), and their commentary suggested the worst was behind us. In 2020 and 2021, it was growth at all costs and the mentality was let it rip. This means we got commentary for the first time on May trends.

As the close of 2019 approaches, with extreme stock market volatility and mixed economic signals, SaaS Finance execs building plans for 2020 and 2-5 years beyond don’t have an easy time. The 2020 projection is now 3.4%, compared with 3.6% in 2019 and are only projecting 3% growth worldwide in 2020, with 2% growth in the US.

On the Microsoft earnings call they said (related to Azure): “But at some point, workloads just can't be optimized much further. My interpretation is we’re in the bottoming phase. The macro environment isn’t getting worse, but it’s not necessarily getting better yet.

#TBT to my last pre-pandemic, non social distance #WeeklyWalk with Edna Conway , VP and GM Global Security, Risk and Compliance, Azure at Microsoft. She let us in on her 2020 security theme, where she believes VCs should be investing their money, and what she’s cooking us for Sunday dinner (when this is all over).

2020 left no doubt: the growth of cloud computing is firmly grounded in the SaaS business model. Control the scope of downstream interactions SaaS predict platforms can also take advantage of Container Clusters or Serverless Platforms such as AWS Lambda, GCP Functions, and Azure Functions to attach IAM roles for Silo Compute Isolation.

Then we’re going to do some work together to figure out how to take those models, those platform building blocks, and get them deployed into products that Microsoft offers, like GitHub Copilot, as well as deploy these things into environments like Azure and Azure OpenAI API, where people can just build their own software on top of it.”

It’s clear that buyers are racing to the Cloud Marketplace, like those offered by AWS, Azure, GCP, and IBM / Red Hat, and sellers are eager to tap into the Cloud budget to help their buyers get started fast or scale contracts fueled by cloud budget growth. All of them said they were likely or extremely likely to purchase this way again. .

Cloud service models in 2020. Windows Azure — Built on their Azure platform, this offering from Microsoft allows developers to use Windows through a cloud-based virtual desktop and develop applications from anywhere using Visual Studio Online. Hubspot — Along with Salesforce, Hubspot is one of the leaders in inbound marketing.

Running your own server to handle your customer's valuable data requires a huge investment to match the same level of security and reliability that comes baked into services like Amazon AWS and Microsoft Azure cloud. They beat their revenue forecast for the second quarter of 2020, hitting 21% growth over the previous quarter.

This statistic will likely change in the coming months as new data rolls in, but Statista reports that there were a whopping 540 data breaches in 2020. For example, with Azure RBAC you can: Allow one user to manage virtual machines in a subscription and another user to manage virtual networks. Excess permissioning increases risk.

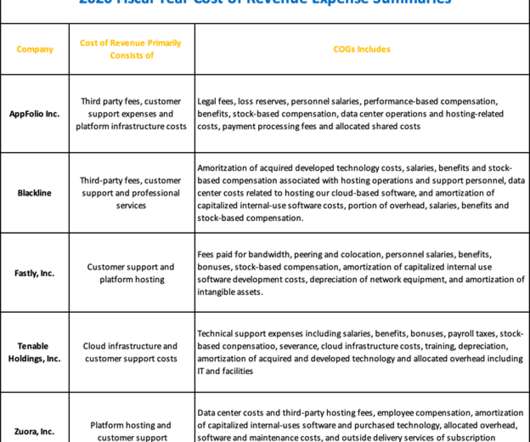

It includes the 2020 fiscal year COGs and gross margin data of Bessemer Cloud Index companies, with annual revenues ranging from $250M-$500M. The prevalence and extremity of outliers reflected within this cohort highlight the substantial differences in business models between SaaS companies in 2020. The Devil is in the Details .

You can still register for Altitude 2020 to view this keynote and the rest of the week’s previous sessions. To support the growing number of Microsoft-based SaaS environments, Brennan announced that a new Azure AD integration will be available in Q4 of this year. These updates focused on improving the product in three key ways.

To say that 2020 has been unusual, and unprecedented, and momentous would all be understatements. Coincidentally, SaaStr Annual was slated to be February 5th, 2020 this year, where we were going to reveal that the cloud had passed the one trillion market cap mark, which was exactly one year after the SaaStr Annual 2019.

41% of respondents cited a lack of digital capabilities as the reason they were likely to switch insurance carriers in 2020. Industry Cloud Consulting A team of industry cloud professionals can have considerable experience with insurance cloud-native systems and competence in top hyperscalers like AWS and Azure.

In February 2020, the public cloud market surpassed a $1 trillion market cap, with a 45% growth rate, as reported in Bessemer Venture Partners’ 2020 State of Cloud report. If you want to learn more about cloud marketplace macro trends, read the full State of Cloud Marketplaces 2020. .

BetterCloud’s 2020 State of SaaSOps report shows that after using automation to discover the number of SaaS apps running on the corporate network, on average, the total is 3 times higher than IT originally thought. IAM products such as Azure Active Directory can enable: Single sign-on (SSO). Difficulty achieving visibility.

And with new projects in our pipeline, we expected our compute power needs to double by the end of 2020. Our options were Amazon Web Services (AWS), Google Cloud (GCP), and Azure. Why move and why now? As great of a choice DigitalOcean was, our organic growth was pushing the boundaries of our setup over the years. Team expertise.

We will support exports to Amazon S3, Microsoft Azure Blob, and Google cloud storage. You can find the ones from past years here – 2020 , 2019 , 2018 , 2017 , and 2016. Cloud destinations (coming soon) — we are in process of adding the ability to export your MRR movements data from ChartMogul onto the cloud.

Google Cloud , Azure, and GitLab, all tied directly or indirectly to AI, are seeing massive acceleration. But Google Cloud, Azure, and GitLab are all benefiting and on fire. Security and compliance are strong, with Wiz turning down billions from Google. Crowdstrike is up and still grew 35%. Is there a bubble? Does it matter?

If you didn’t catch it the other day … and you can read about it on SaaStr …Microsoft and Google Cloud both had extremely strong quarters, Microsoft Azure grew 40% last quarter , and a record number of nine-figure and billion-dollar deals. Microsoft Azure’s at incredible scale and it still grew 40% last quarter.

We organize all of the trending information in your field so you don't have to. Join 80,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content