This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

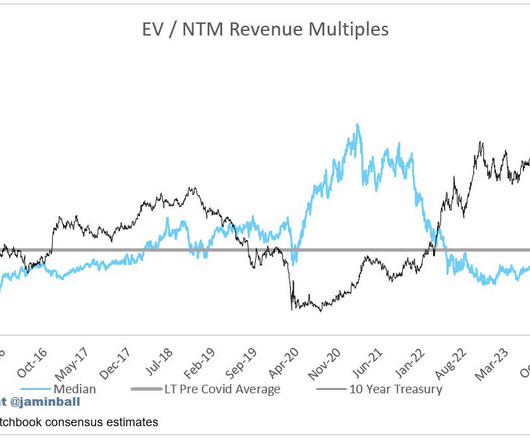

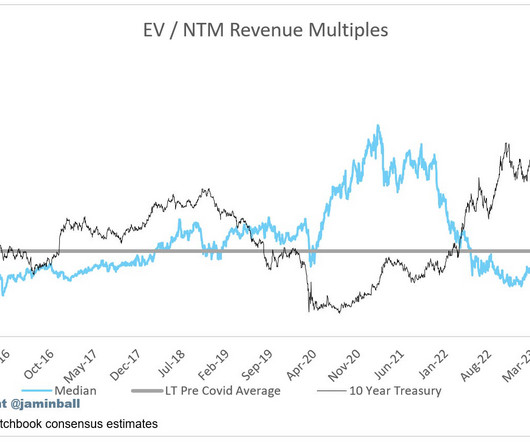

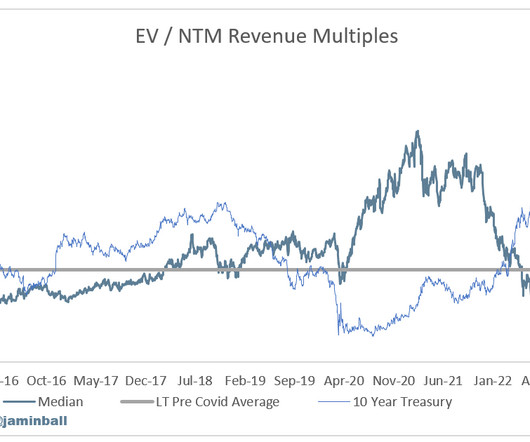

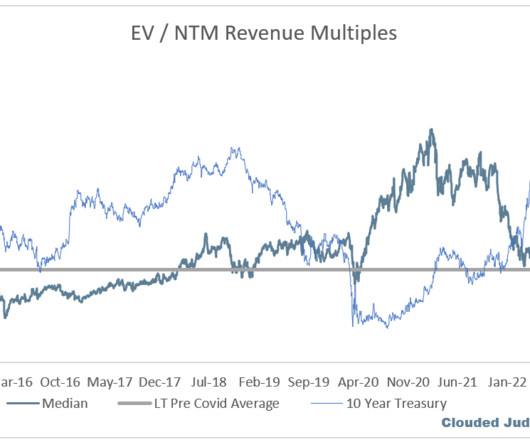

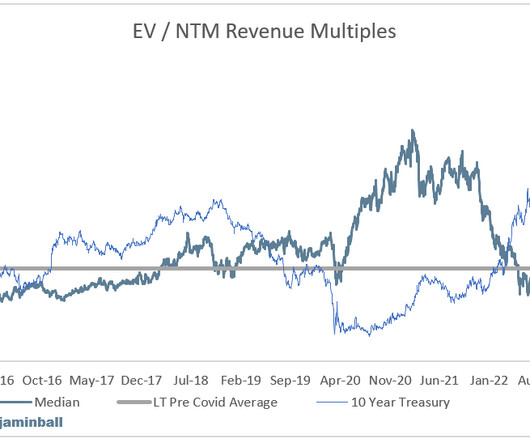

It’s worth pointing out that Azure is a bit above the long term trendline, while AWS is still below (but accelerating up). It’s worth pointing out that Azure is a bit above the long term trendline, while AWS is still below (but accelerating up). The graph below shows the median net retention going back to 2020.

We all know 2020 and 2021 was the year of excessive software buying fueled by ZIRP. The hyperscalers (AWS, Azure, GCP) are always some of the first companies to report earnings during earnings season (coming up in 2 weeks), and there’s always a read through for consumption names (meaning people believe there’s a correlation).

We now have results from the three hypersclaers (AWS / Azure / GCP). This is lower than Q1 2020 (right at the onset of Covid) when everyone seemed to guide lower given the unknowns of Covid. Most public companies don’t report net new ARR, so I’m taking an implied ARR metric (quarterly subscription revenue x 4).

For context on a 10Y at 5% - from 2010 to 2020 the 10Y averaged roughly ~2.5%. Said another way, the 10Y today is double what it averaged from 2010 to 2020. Hyperscaler Preview Next week Amazon, Microsoft and Google report earnings and we’ll see Q3 data for AWS, Azure and Google Cloud.

It looks at the YoY dollar change in quarterly revenue from the hyperscalers (just looking at Azure / AWS because the data goes back further) going back a few years. If you look at the historical data you’ll see there’s a very clear trendline through the end of 2020. This is the data point shown for Q4 ‘23.

What you’ll see in that cloud spend box is actually Gartner’s 2020 estimate for infrastructure as a service spending for companies, which was $50 billion. And IDG just recently released the 2020 Cloud Computing Survey that showed over one third of IT budgets are spent on cloud computing technologies.

Azure / Confluent / Datadog reported a few weeks back (they all had March quarter ends), and their commentary suggested the worst was behind us. In 2020 and 2021, it was growth at all costs and the mentality was let it rip. Companies that do not disclose subscription rev have been left out of the analysis and are listed as NA.

This growth adjusted premium also comes at a time when the 10Y is nearly double what it was from 2010 to 2020. Maybe with the exception of hyperscalers (particularly Azure). Most public companies don’t report net new ARR, so I’m taking an implied ARR metric (quarterly subscription revenue x 4).

On the Microsoft earnings call they said (related to Azure): “But at some point, workloads just can't be optimized much further. To calculate implied ARR I take the subscription revenue in a quarter and multiply it by 4. My interpretation is we’re in the bottoming phase.

Our mission is to build the world’s most powerful subscription analytics platform for the SaaS community. Building the leading subscriptions analytics platform means listening to our customers, and implementing changes to the product that bring them the most value. What’s new in ChartMogul in 2021? ChartMogul is a product-led company.

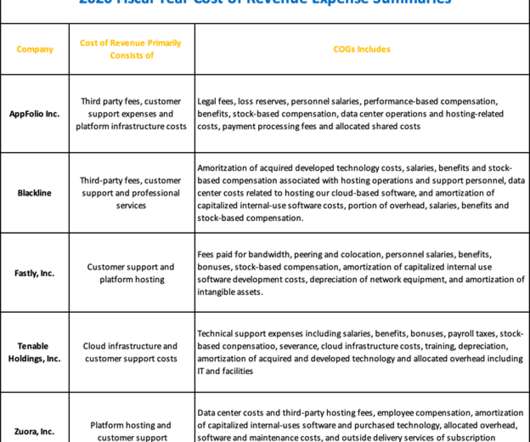

Self-hosted SaaS environments that don’t leverage third-party vendors must also proportionally split their self-hosting expenses between company use for business operation and customer subscription platform usage. . Professional services are billable implementation and customization services sold to customers. The Devil is in the Details .

This statistic will likely change in the coming months as new data rolls in, but Statista reports that there were a whopping 540 data breaches in 2020. For example, with Azure RBAC you can: Allow one user to manage virtual machines in a subscription and another user to manage virtual networks.

Cloud service models in 2020. Some SaaS products allow the user to download the application, but require an internet connection to confirm their subscription for it to operate. Many business owners do not know the difference between these offerings and are therefore unaware of which option is best for their company.

For example, in March 2019, security researchers found that dozens of major tech companies and corporations had inadvertently exposed sensitive data through misconfigured Box accounts. Researchers discovered bank account and Social Security numbers, passwords, employee lists, and financial data like invoices, receipts, and customer data.

We kept growing over the years, and by 2019 we found ourselves looking at a fleet of somewhere around 50 machines in constant need of management, software updates, security patches, and so on. And with new projects in our pipeline, we expected our compute power needs to double by the end of 2020. Why move and why now? Team expertise.

The report also highlighted that the spending in space went up to 170% in 2020. The company offers a data analytics platform based on Amazon Web Services (AWS), Google Clouds, and Microsoft Azure. Based on this, it can be said that Indian-origin SaaS companies could capture an 8% to 9% share of the international SaaS market.

And then there was this great workplace experience of 2020, which we’re still living now. So now we’re in this, like you call it, the great workplace experiment of 2020, where we’re forced to be a hundred percent remote. Someone forgot to turn the security on, the elastic database. Justin Bedecarre: Right.

It really does need to be broken down into parse and process the invoice, then check the ERP, then do these things. You know, like there, there’s one kind of case to be made where let’s say, you know, I have an AI agent that I want to send my invoices and follow up on invoices. There was an obvious way to.

We organize all of the trending information in your field so you don't have to. Join 80,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content