This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

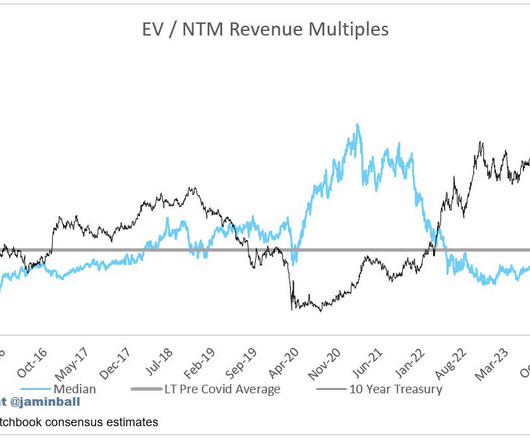

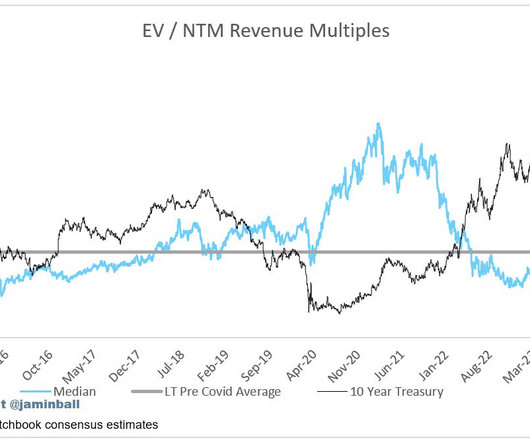

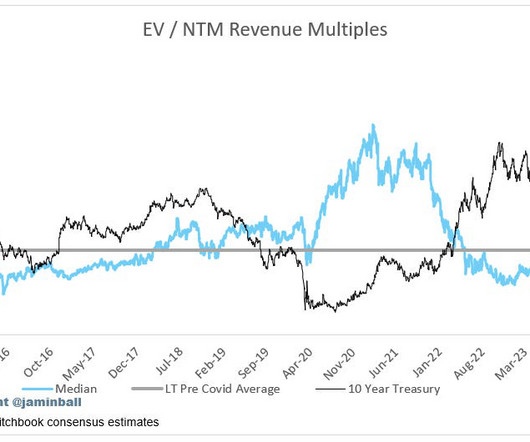

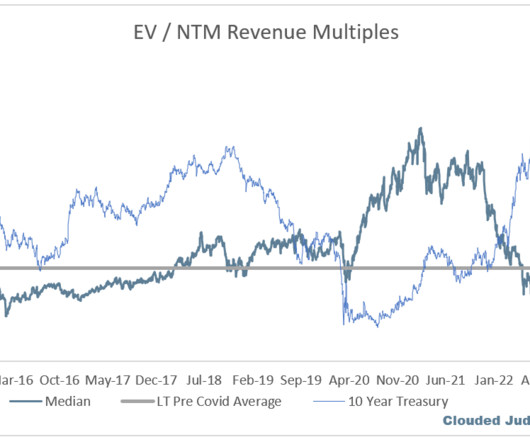

However, if we rewind the clock to a year ago, the budget flush at the end of 2023 felt stronger than most years. Selling software remained challenging in 2023 - despite budgets starting to grow again. All of that could create a good setup for software in Q4! This concept is nothing new and has been going on for a while.

After a strong finish in Q4, we saw a return to weaker demand conditions in the first quarter, similar to what we experienced in 2023. Given most software companies are not profitable, or not generating meaningful FCF, it’s the only metric to compare the entire industry against. Even a DCF is riddled with long term assumptions.

.” As growth starts to slow, it gets harder and harder to justify using revenue multiples as a primary valuation metric. And when this happens, growth companies transition to more of a value based valuation metric (FCF or PE). The “power of the bundle / platform” is very real.

The hyperscalers (AWS, Azure, GCP) are seeing some uptick, but this is largely from selling compute (ie cloud GPUs). In summary, I don’t expect real AI tailwinds to show up in non-hyperscaler businesses in a meaningful way through the rest of 2023. However, it’s not showing up in the data yet.

Iceberg is open source, and is the leading table format, having been adopted by Snowflake, AWS, GCP, Databricks, Confluent and many others, with contributions and usage coming from some of the largest organizations like Netflix, Apple, LinkedIn, Adobe, Salesforce, Stripe, Pinterest, AirBNB, Expedia and many others.

We organize all of the trending information in your field so you don't have to. Join 80,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content