This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

I’ve also seen this in the leaders in eComm I’ve invested in, like Gorgias. Second, AWS, Azure and Google Cloud all grew nicely, and are still growing like a weed — but the growth rate slowed. Cloud Giants Update: AWS (Amazon): $82B run rate growing 28% YoY (last Q grew 33%). Perhaps as it should be.

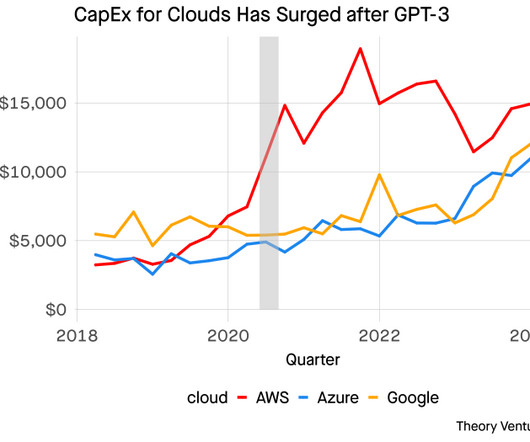

Aside from the overall growth of these clouds increasing, the massive investment in CapEx data centers, power plants, and GPUs is stunning. Google and Microsoft would wait another two years to replicate a similar level of investment. Google and Microsoft would wait another two years to replicate a similar level of investment.

So follow AWS, Azure and Google Cloud. And it is stressful, especially if you invested at those peaks or as founders raised money at relatively high valuations and multiples. Let’s look a whole level up to the real canaries-in-the-coalmine: AWS, Azure and Google Cloud. For now, they are still on fire.

Because thats how their customerswho were used to AWS, Azure, and GCP pricingexpected to buy. Final Advice for Revenue Leaders After nearly a decade of scaling Databricks, Ron has one core piece of advice for revenue leaders: hire the best people and invest in them. Talent beats everything. Culture beats everything.

My summary of Venture Markets in Nov 2022: Series B and later even worse than looks in data: 85%+ of investing here has simply ceased. And while AWS’s growth is down a bit, it’s still at epic levels, Azure isn’t even really down, and Google Cloud is growing faster than ever.

It’s worth pointing out that Azure is a bit above the long term trendline, while AWS is still below (but accelerating up). It’s worth pointing out that Azure is a bit above the long term trendline, while AWS is still below (but accelerating up). Altimeter is an investment adviser registered with the U.S.

Another 5%-7% go to core infrastructure costs (AWS, Azure, Snowflake, etc). It’s your top marketing and customer retention investment. Typically support consumes about perhaps 5%-7% of your revenue at scale (excluding customer success) in most SaaS models. It could be more or less, but that’s a rough way to think about it.

They each have some of the largest cloud businesses in the world in AWS, Azure and Google Cloud respectively. This is for information purposes and should not be construed as an investment recommendation. Altimeter is an investment adviser registered with the U.S. Overall, there was weakness across the board.

This behavior can create a surge in purchasing activity, as organizations look to make strategic investments without losing their allocated funds. This is for information purposes and should not be construed as an investment recommendation. Altimeter is an investment adviser registered with the U.S. Cloudflare is up 17%.

Secureframe allows companies to get compliant within weeks, rather than months and monitors 100+ services, including AWS, GCP, and Azure. Verdane is a specialist growth equity investment firm that partners with tech-enabled and sustainable businesses based out of Europe to help them reach the next stage of international growth.

And it’s one of the three large cloud vendors that we all know: Microsoft, AWS, and Google. Azure’s marketplace has over 4 million monthly visitors. AWS’s marketplace has seen 1.5 Like I said, we run 100% of our platform on AWS, so the fit was great. It was pretty easy to drive that from our side.

In the cloud, AWS, Azure, & GCP have created about as much market cap as all the top 100 B2B & B2C publics built on cloud (Netflix, ServiceNow, AirBnb, etc). It’s likely startups start at plug-ins & then move down with scale that affords more usage & more capital to invest.

Subscribe now Cloud Giants Report Q3 ‘23 Not a great signal for software this week from the Cloud Giants (AWS, Azure and Google Cloud)…After Q2 (3 months ago), the tone from the Cloud Giants around optimizations was largely: optimizations have started to ease, and net new workloads have picked up. Staggering scale already.

We now have results from the three hypersclaers (AWS / Azure / GCP). The most notable change in tone was Andy Jassy talking about AWS. This is for information purposes and should not be construed as an investment recommendation. Altimeter is an investment adviser registered with the U.S.

The traditional clouds (AWS, GCP, and Azure) are getting dated. This is why I’m so excited to announce our investment in Tigris, as well as the release of its globally available S3-compatible distributed object-storage service. However, storage has been a key issue for moving applications wholesale to these new clouds.

Historically, Cloud platforms like AWS and Azure help with the sporadic needs of renting a GPU for a few hours for training vs. long-term use, which would cost thousands of dollars. If someone doesn’t want to switch from AWS because AWS has partnerships with OpenAI, they have tradeoffs. What about ROI?

Amazon on AWS : “…customers are continuing to shift their focus towards driving innovation and bringing new workloads to the cloud. ” Microsoft on Azure : “And I think last quarter, we said one, we are going to continue to have these cycles where people will build new workloads. Follow along to stay up to date!

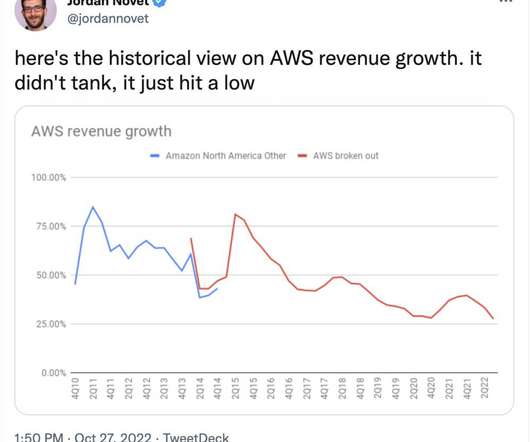

It looks at the YoY dollar change in quarterly revenue from the hyperscalers (just looking at Azure / AWS because the data goes back further) going back a few years. If we break this down and look at Azure and AWS independently (graphs below), you’ll see how the AWS “swings” were a lot more volatile.

The role of AWS, Azure, and Google Cloud Marketplace is becoming increasingly important. “45% Categories like customer success, learning management platforms, and onboarding software are witnessing increased investments. . The value of community expertise: Invest in advocacy and connecting customers with each other. .

The most triumphant transfer of control from an original generation leader to a new CEO was surely that of Microsoft, which pivoted from chasing after Apple’s success in the consumer space under Steve Ballmer (don’t mention Nokia ) to successfully focusing on the cloud under Satya Nadella (please do mention Azure).

Hyperscaler Preview Next week Amazon, Microsoft and Google report earnings and we’ll see Q3 data for AWS, Azure and Google Cloud. This is for information purposes and should not be construed as an investment recommendation. Altimeter is an investment adviser registered with the U.S.

Hyperscalers Report Quarterly Earnings This week we saw AWS (Amazon), GCP (Google) and Azure (Microsoft) report earnings. Overall, it wasn’t pretty… AWS grew 28% when expectations were 30-31%. At the same time, Azure came in below expectations. Follow along to stay up to date!

AWS (Amazon), Azure (Microsoft), and Google Cloud (Google) all reported this week. Azure reported on Tuesday and gave us that glimmer of hope. Then AWS appeared to add fuel to that hope before giving us a huge rug pull. Azure came in at 31% (constant currency). They then guided to 26-27% Azure growth in Q2.

Cloud Downgrades This week UBS came out with a couple research reports citing concerns in AWS / Azure growth. This brings me back to AWS / Azure downgrades. Every week I’ll provide updates on the latest trends in cloud software companies. Follow along to stay up to date! It’s very tricky to predict.

Cloud Giants Report Q2 We also got the Q2 quarters from AWS / Azure / GCP this week! Our expectation, obviously again, is that we are going to significantly increase our investments in AI infrastructure next year, and we'll give further guidance as appropriate.” Altimeter is an investment adviser registered with the U.S.

Subscribe now Foundation Models Are to AI what S3 was to the Public Cloud Many people look at 2006 as the birth of the public cloud - the year Amazon launched AWS. Microsoft launched Azure in 2010, and Google launched GCP to the public in 2011 (they launched a preview of Google App Engine in 2008, but made it publicly available in 2011).

” These are two quotes about AWS on the Amazon earnings call. AWS grew 16% in Q1, but called out growth in April (first month of Q2) was 11%. You can see more detail about their net new ARR added each quarter below Azure Growth came in at 27%, and guided to 25-26% growth for Q3.

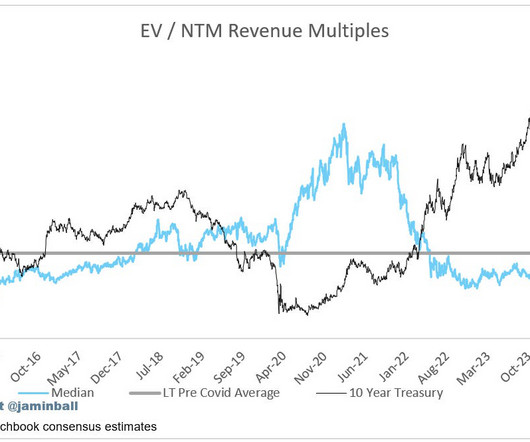

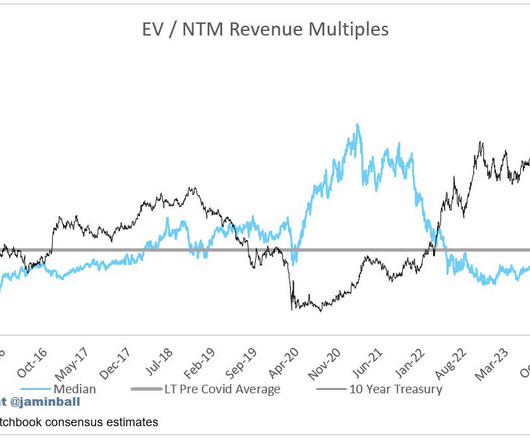

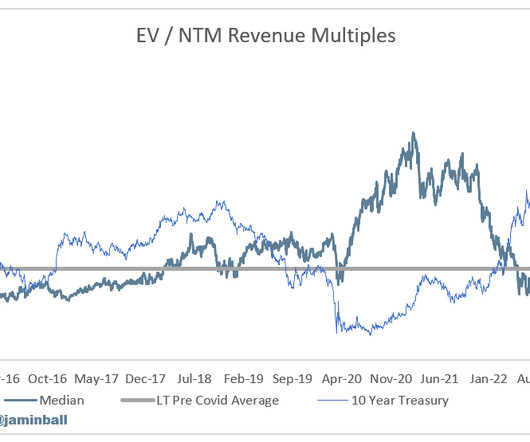

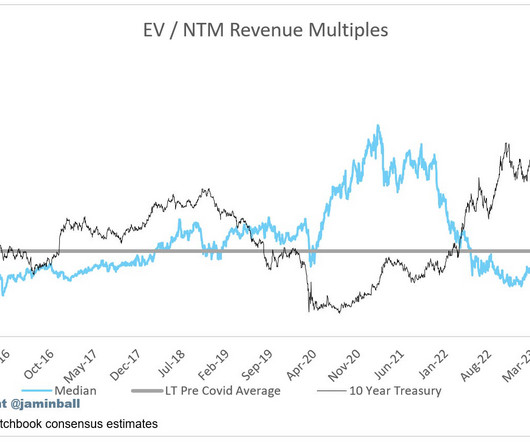

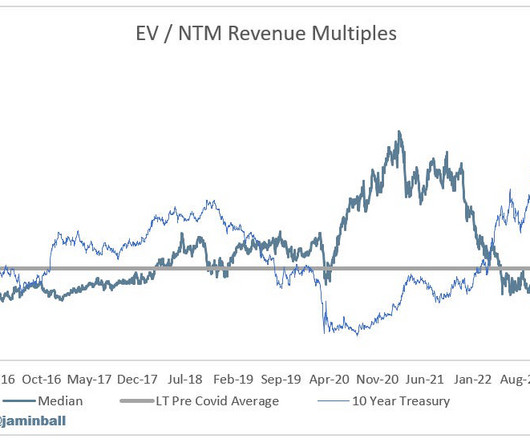

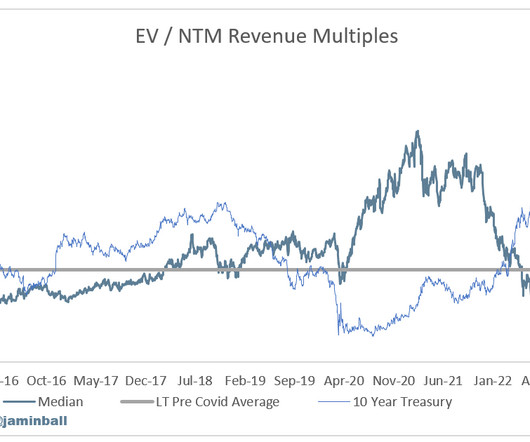

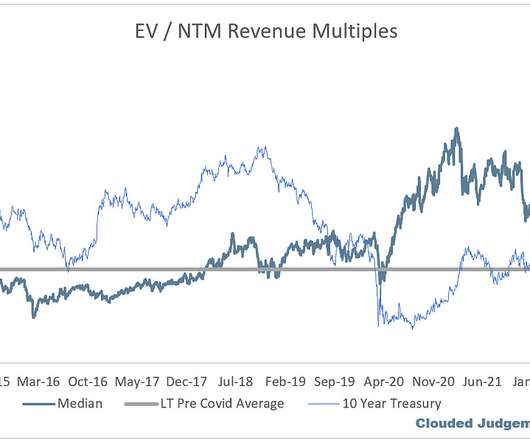

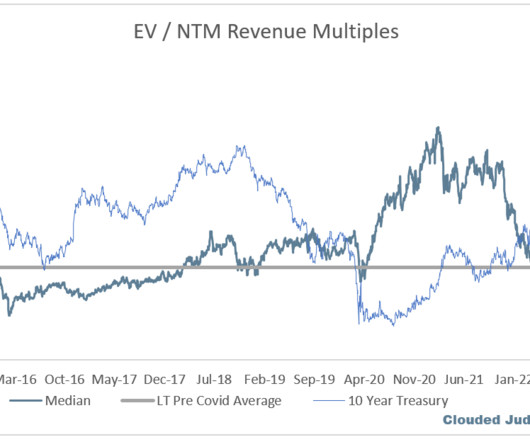

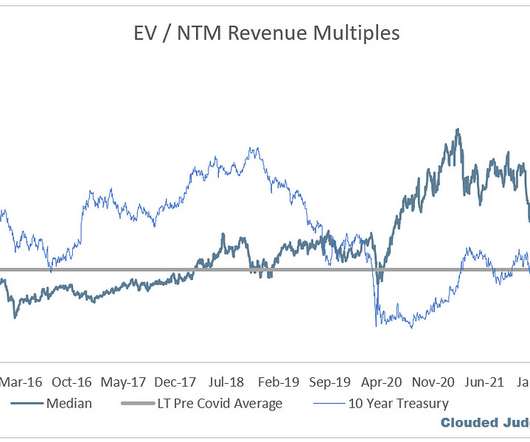

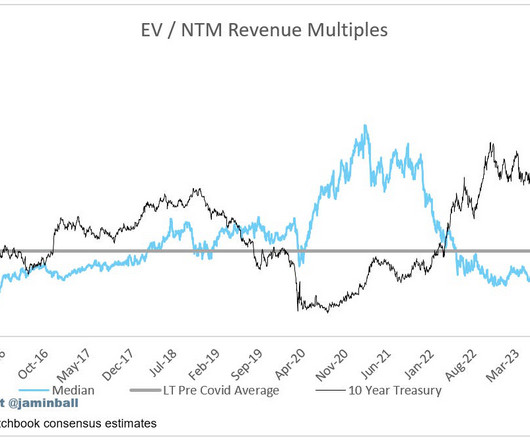

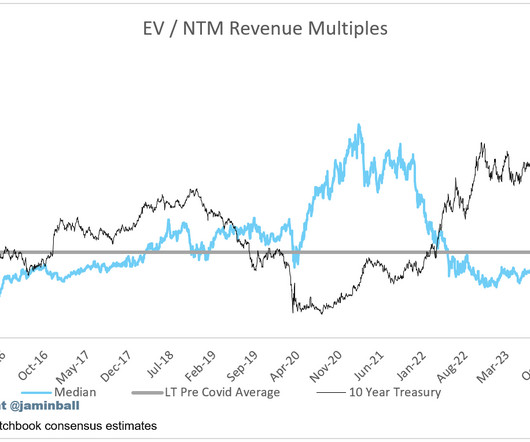

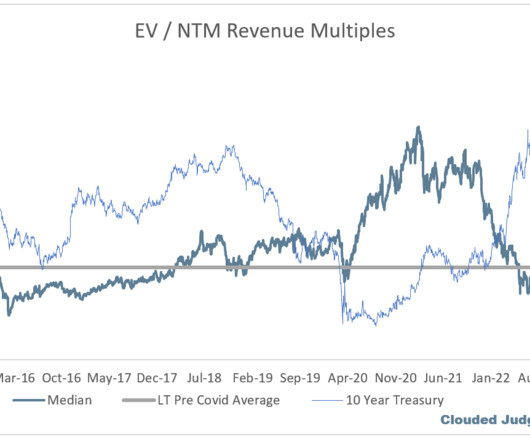

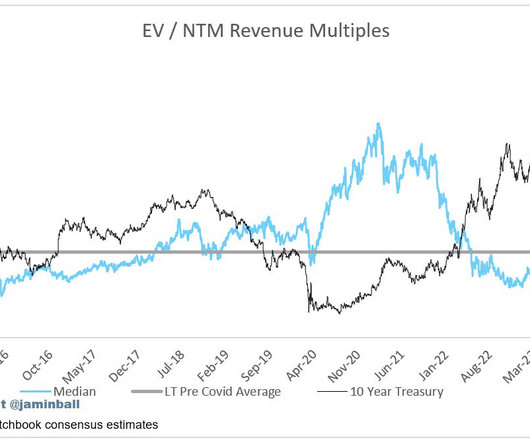

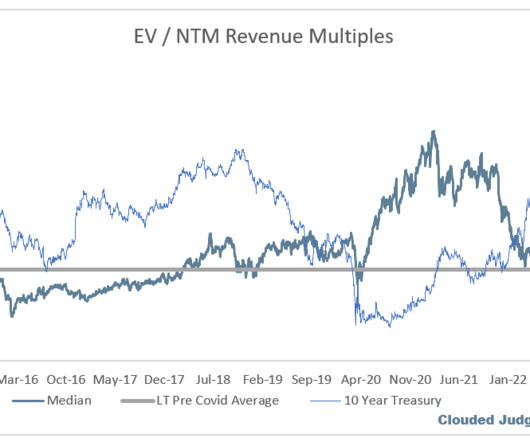

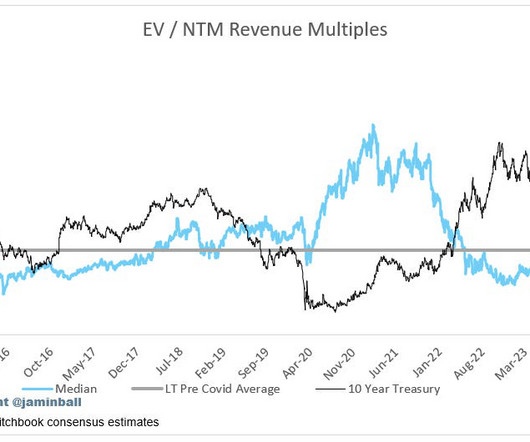

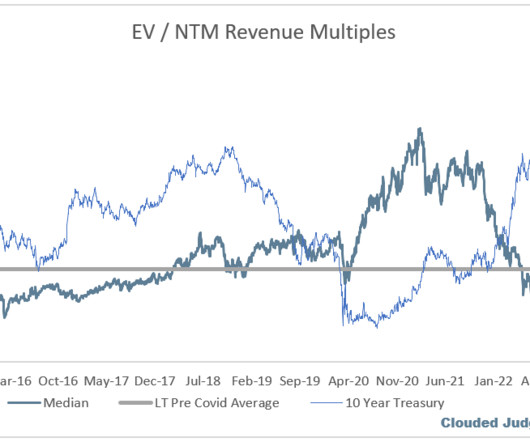

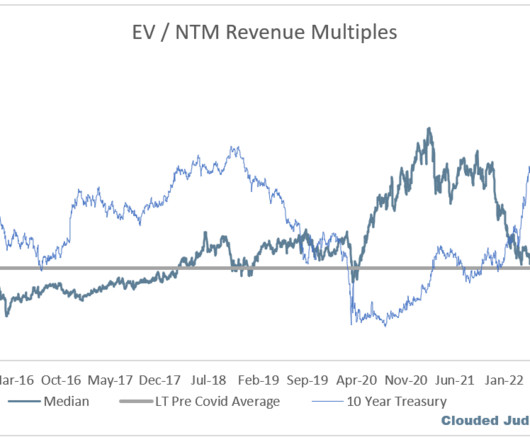

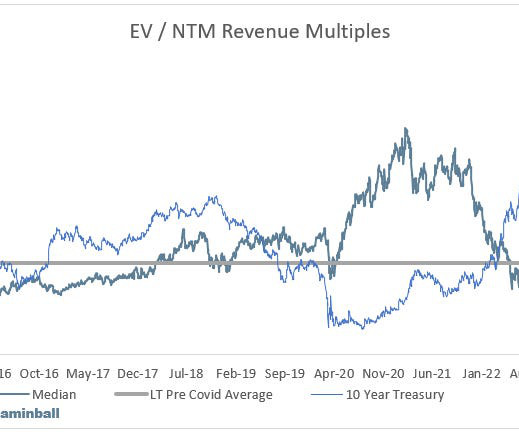

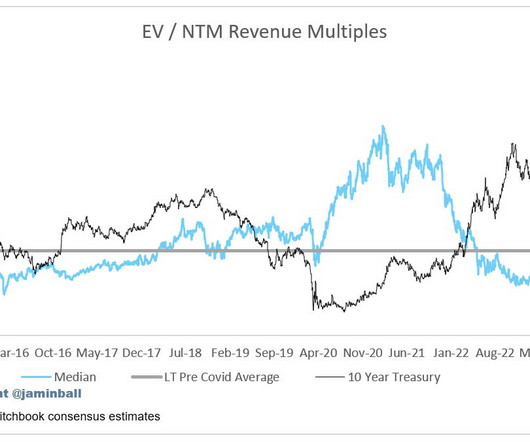

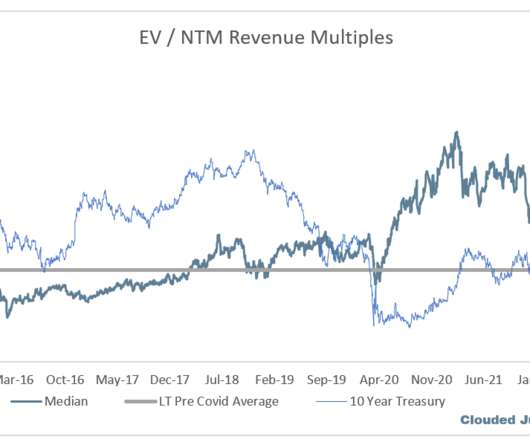

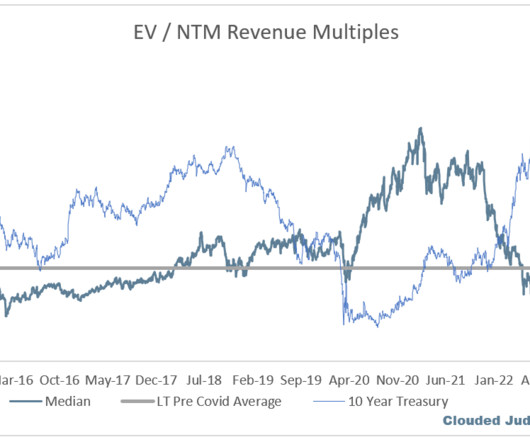

All 3 (AWS, Azure, GCP) saw positive reacceleration Quarterly Reports Summary Top 10 EV / NTM Revenue Multiples Top 10 Weekly Share Price Movement Update on Multiples SaaS businesses are generally valued on a multiple of their revenue - in most cases the projected revenue for the next 12 months. Securities and Exchange Commission.

Next week we get all 3 hyperscalers reporting (AWS from Amazon, Azure from Microsoft, and GCP from Google). Let’s double click on Azure. On AWS, in their Q4 earnings call they said AWS was growing “mid teens” in January (down from 20% in Q4). The Q4 ‘22 growth rate was 38% YoY.

This can lead to an airpocket of valuation as companies transition to a different primary valuation metric Outside of the hypserscalers (Azure, AWS, GCP) who have uniquely benefited from AI revenue (mainly selling compute), everyone else has largely struggled. But these investments aren’t cheap.

AI = Data + Compute I’ll continue beating this drum, but we got two great quotes from Azure and AWS this week. ” Then at AWS Summit they called out “Your data is your differentiator when it comes to Generative AI.” AWS reports next week. ” Data is more important than ever!

Usage on Snowflake is driven by queries run on Snowflake Azure: Neutral Tone With Strength in AI Overall I’d characterize Azure’s quarter as a net positive. They guided to 26-27% growth in Azure in Q2 (with 1% coming from AI). Their consumption is driven by usage of applications built on top of Mongo.

What’s evolved over the years and is driven by hyper-scalers like Google Azure, AWS, Twilio, and Stripe is the consumption-based model. That way, they know what growth to expect and what incremental uplift they’re getting from having sales involved so they can continue to make better investments. This is MongoDB’s approach.

Hyperscalers (AWS, Azure, GCP as companies look for cloud GPUs who aren’t building out their own data centers) Infra (Data layer, orchestration, monitoring, ops, etc) Durable Applications We’ve clearly well underway of the first 3 layers monetizing. Altimeter is an investment adviser registered with the U.S.

This is why the consumption players (Snowflake, Mongo, Confluent, Azure, AWS, etc) so more variability in the macro slowdown. This is for information purposes and should not be construed as an investment recommendation. Altimeter is an investment adviser registered with the U.S. Securities and Exchange Commission.

This is why we’re seeing more and more SaaS companies—Datadog, Twilio, AWS, Snowflake, and Stripe, to name a few—find success with product led growth paired with usage-based pricing. Though it was pioneered in the infrastructure layer (think: AWS and Azure), it’s becoming increasingly popular for API-based products and application software.

In the short term, enjoy the ride as the chase continues 😊 Kind of related to all of this - we now have seen the Q4’s from AWS, Azure and Google Cloud. Lots of deceleration in growth.

If next quarter we get similar commentary that Azure gave us this quarter (“still a couple quarters away” without any specific guidance), then we may see market loose a little patience. The hyperscalers (AWS, Azure, GCP) are seeing some uptick, but this is largely from selling compute (ie cloud GPUs).

You can find the original post here Today we’re very excited to announce our partnership and Series B investment in Tabular , the company behind Apache Iceberg. Typical data lake storage solutions include AWS S3, Azure Data Lake Storage (ADLS), Google Cloud Storage (GCS) or Hadoop Distributed File System (HDFS).

You can see the growth on the platform side with Azure, Google, and AWS and how much it’s accelerating in AI. VCs Want To Invest, But There’s Stress In The System As a community, we over-talk about venture capital, but it’s important if you’re fundraising and to understand the pulse of the system. Every VC wants to invest.

This means it’s vitally crucial for businesses to understand what they’re investing in and how they can make the most of cloud computing. For businesses running e-commerce sites, this means they don’t have to worry about the highly technical aspects of running a web application and they don’t have to invest in expensive infrastructure.

We’ve all seen AWS and what they’ve done with their platform. Azure has been gaining on them rapidly and is growing a double that rate. One of the early co-investments with my prior firm in Bessemer was in Shopify. Invest, do whatever you can when they go because it’s a tell when they start looking good.

Jason Lemkin: The highest stage of venture is crossover, crossover funds, TCV is one of an early one, but even mutual funds that invest in unicorns. A few can, Andreessen and maybe Sequoia, but 99% of the VCs you meet, legally, they can only invest in startups, whether they’re late stage or early stage. It could come back.

This article will look at the most successful SaaS companies, so you can decide if you want to invest in them for your business. Key examples are Amazon Web Services (AWS), Microsoft Azure, and Google Cloud Platform, which provide scalable resources like virtual servers and storage. What are the benefits of the SaaS model?

We organize all of the trending information in your field so you don't have to. Join 80,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content