This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

There are many ways to slice-and-dice public market data, but the headline one Bessemer called out is the most visceral I’ve seen: Public SaaS and Cloud companies lost $1 Trillion in market cap so far in 2022. At the same time, the leaders in Cloud (AWS, Azure, Google Cloud) are growing a stunning 40%.

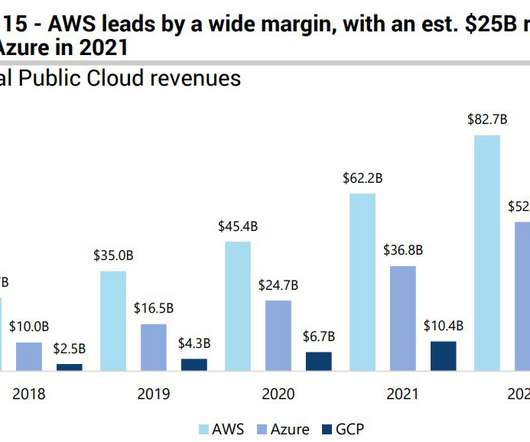

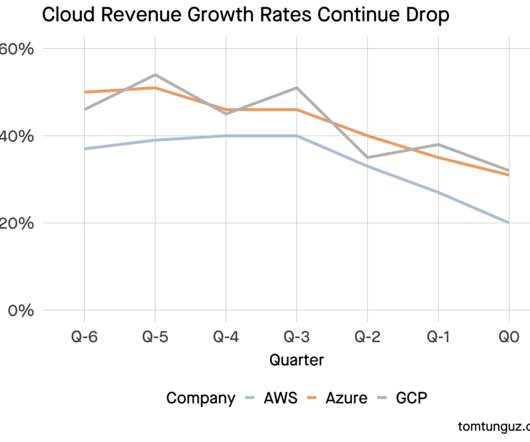

AWS announced earnings earlier today and reported 33% growth. AWS’s growth rate is the slowest of the three largest public infrastructure clouds. With about 39% market share, AWS reigns supreme as the largest provider. With about 39% market share, AWS reigns supreme as the largest provider.

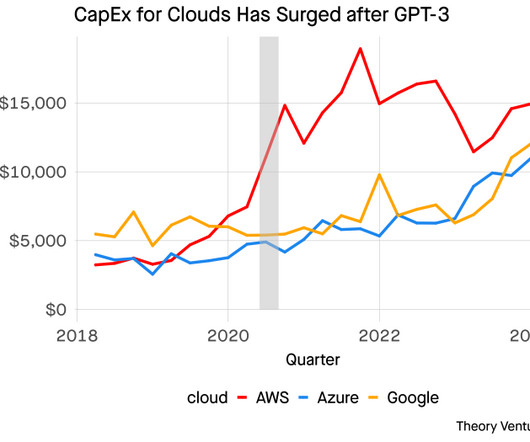

Cloud Capex in Q1 AWS $14 billion Azure $14 billion Google Cloud $12 billion These are not one-time investments, but part of a broader trend that started to occur after the introduction of GPT 3 in mid-2020 Amazon was the first to invest significantly. “Moving to AWS.

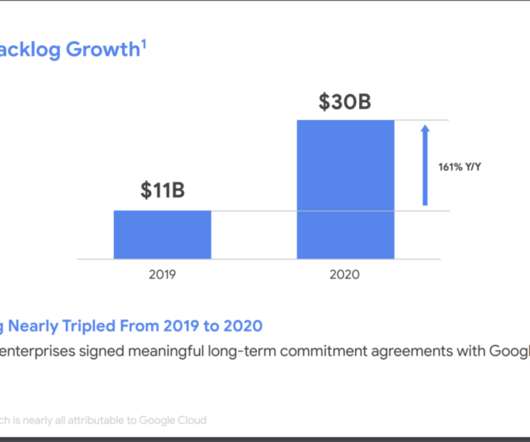

But are AWS, Azure and Google Cloud just too big for us to learn from? The Cloud Market as Google Cloud defines it has grown at a jaw-dropping rate, from $85B in ’15 to $290B in ’20. Google Cloud continues its march upmarket, competing with Azure. So I think there are some good learnings! million customers.

With technology giants like Google, AWS, and Azure leading the charge, the true value of the cloud extends far beyond cost savings. In a rapidly evolving industry, the shift from traditional on-premise systems to cloud-based solutions has become crucial for retail success. Save your seat today!

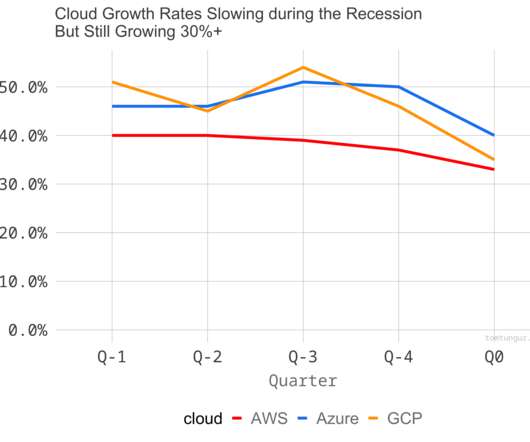

I’m watching public company earnings to identify early weaknesses in the software market. A year ago, AWS, GCP, & Azure averaged 44% annual growth. Amazon: We expect [customer] optimization efforts will continue to be a headwind to AWS growth in at least the next couple of quarters. So

These early conversations helped shape Databricks product, pricing, and go-to-market strategy. Because thats how their customerswho were used to AWS, Azure, and GCP pricingexpected to buy. When you see product-market fit, go all in. Talk to users. We went to the open-source community and asked, What would you pay for?

My summary of Venture Markets in Nov 2022: Series B and later even worse than looks in data: 85%+ of investing here has simply ceased. And while AWS’s growth is down a bit, it’s still at epic levels, Azure isn’t even really down, and Google Cloud is growing faster than ever. But only up to a point.

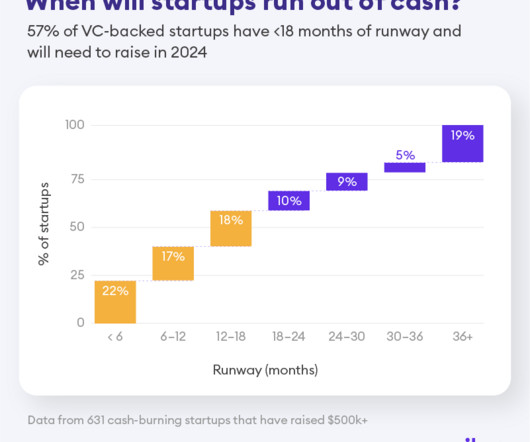

Something that’s both not surprising but also pretty impactful: 57% of venture-backed startups will have to go “back to market” in 2024 to raise more capital. Shopify , Datadog, Crowdstrike , Google Cloud-Azure-AWS, Snowflake , etc. What does Pilot’s latest data say? for the first time in 2024!

It’s worth pointing out that Azure is a bit above the long term trendline, while AWS is still below (but accelerating up). It’s worth pointing out that Azure is a bit above the long term trendline, while AWS is still below (but accelerating up). Either a run up, or a draw down from market factors.

If you’re selling sales and marketing software, like Zoominfo, it can seem a lot tougher than 12-18 months ago. Growth in public cloud services (AWS, Azure, Google Cloud, Snowflake, etc.) If you’re selling cloud infrastructure, for the most part, growth may be down a smidge but is still strong, e.g., MongoDB.

Focusing on smaller developers, in some ways it’s been a bit overshadowed by AWS, Azure, and Google Cloud. But it’s a great case study on how nailing a niche, and staying focused on a core ICP in a huge market, can pay off. So DigitalOcean is the quiet Cloud platform that keeps on growing.

Another 5%-7% go to core infrastructure costs (AWS, Azure, Snowflake, etc). It’s your top marketing and customer retention investment. Typically support consumes about perhaps 5%-7% of your revenue at scale (excluding customer success) in most SaaS models. It could be more or less, but that’s a rough way to think about it.

That’s much more work than the automatic credit card payment with AWS. Perhaps this dynamic drives consolidation in the market, paralleling the web2 infrastructure hypermarts of AWS, GCP, and Azure. It’s too much complexity for a simple static blog.

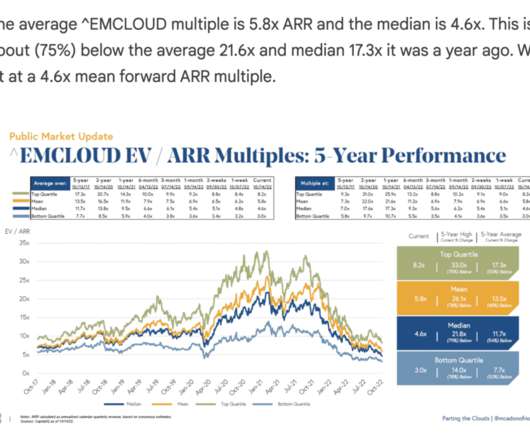

I do think LLMs will really help turbo charge these markets though, and finally make the solutions actually useful. They each have some of the largest cloud businesses in the world in AWS, Azure and Google Cloud respectively. And here’s what gets me really excited - grouping + triage is just step 1. Top 5 Median: 22.2x

I’m watching public company earnings to identify early weaknesses in the software market. Microsoft Azure. Microsoft Azure grew 40% y/y, tying the fastest quarterly growth rate in the past 5 quarters. That suggests the cloud market is quite strong. Google Cloud Platform. Google Cloud Platform. Amazon Web Services.

As a startup, you’re doing a million things at once: building a product, answering customer tickets, developing a sales playbook, trying out different marketing hacks, and keeping the lights on. The reality is all large companies, and more and more mid-market companies, will require a SOC 2 report from their vendors. Deal: closed-lost.

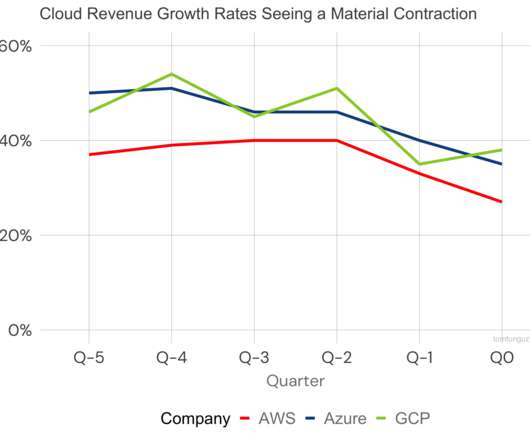

I’m watching public company earnings to identify early weaknesses in the software market. Microsoft Azure. At a 7x multiple of revenue, that is another $84b of market cap creation, in theory. The kink downwards in the red line at Q-2 shows a sudden deceleration in AWS’ growth rate. Google Cloud Platform.

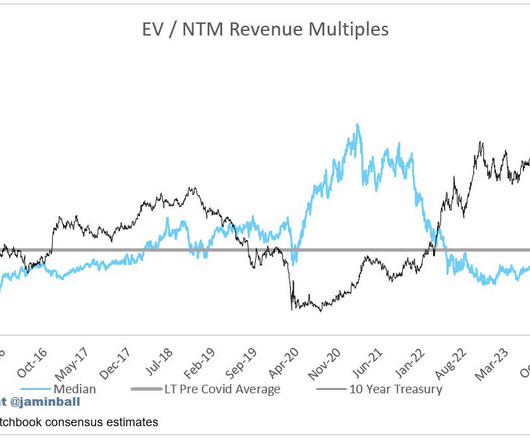

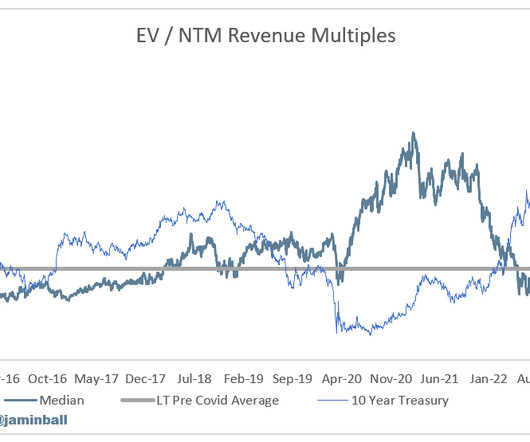

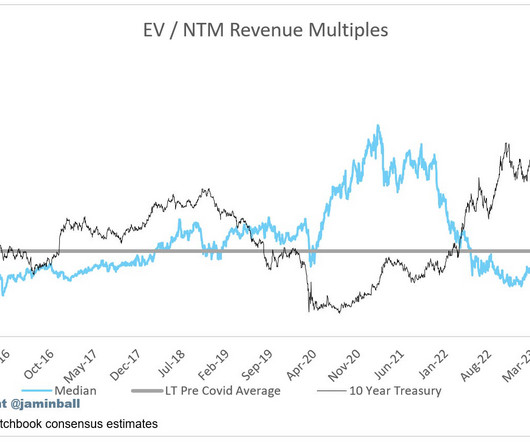

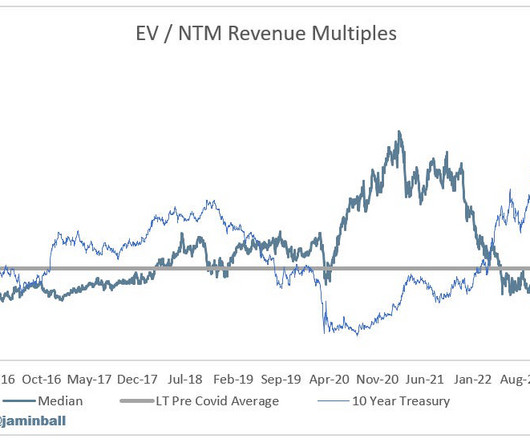

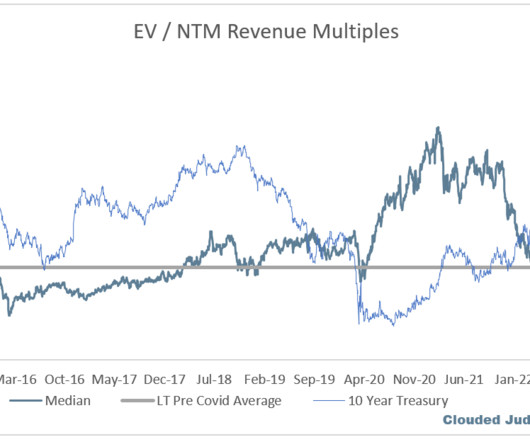

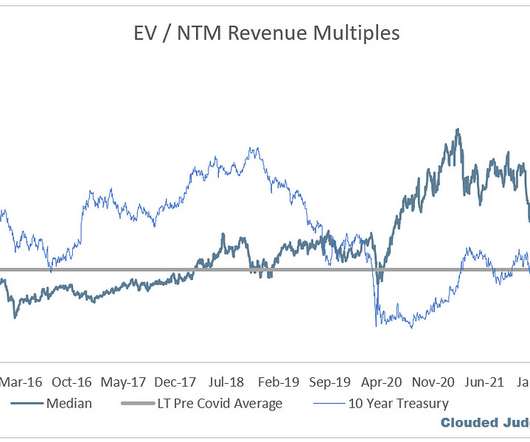

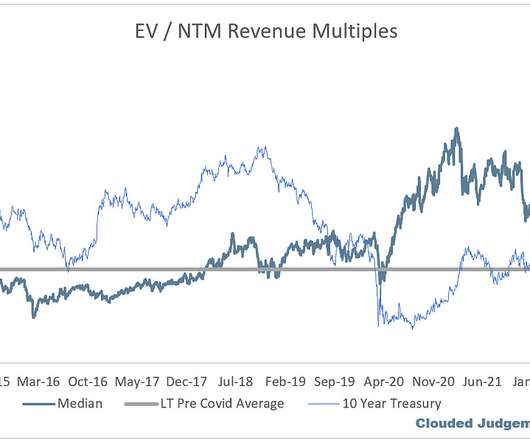

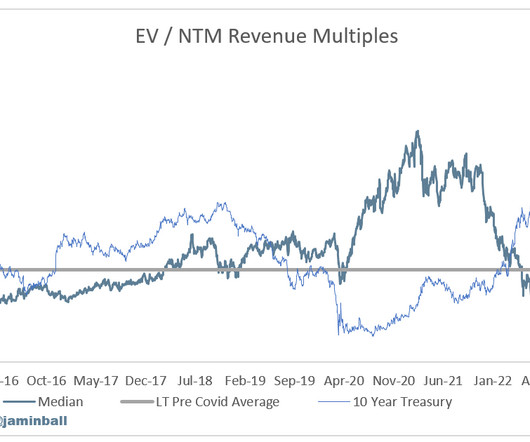

So the public markets are in tumult. This is just starting to roll through the private markets and is going to make a bumpy rest of the year. Revenue multiples are how much VCs, investors, and ultimately, an IPO and public markets will value each dollar of revenue. And indeed there is today! A Covid Hangover in SaaS stocks.’

And it’s one of the three large cloud vendors that we all know: Microsoft, AWS, and Google. Azure’s marketplace has over 4 million monthly visitors. AWS’s marketplace has seen 1.5 Rico Mallozzi: So marketplaces are fundamentally changing, go to market motions for a lot of enterprise technology companies.

Drift brings Conversational Marketing, Conversational Sales and Conversational Service into a single platform that integrates chat, email and video and powers personalized experiences with artificial intelligence (AI) at all stages of the customer journey. Usually, it takes a paradigm shift to grow. appeared first on SaaStr.

We help B2B SaaS marketers turn organic search into a source of repeatable revenue through software and coaching. The platform automates the provisioning of your application to the cloud (AWS, GCP, Azure), integrating cloud ops, DevOps, and security/compliance with 24×7 monitoring and support.

In the cloud, AWS, Azure, & GCP have created about as much market cap as all the top 100 B2B & B2C publics built on cloud (Netflix, ServiceNow, AirBnb, etc). Market : how to compete with incumbents? Layer : application, platform, or infrastructure?

The hyperscalers (AWS, Azure, GCP) are always some of the first companies to report earnings during earnings season (coming up in 2 weeks), and there’s always a read through for consumption names (meaning people believe there’s a correlation). Cloudflare is up 17%. Datadog is up 14%. Mongo is up 16%. Snowflake is up 14%.

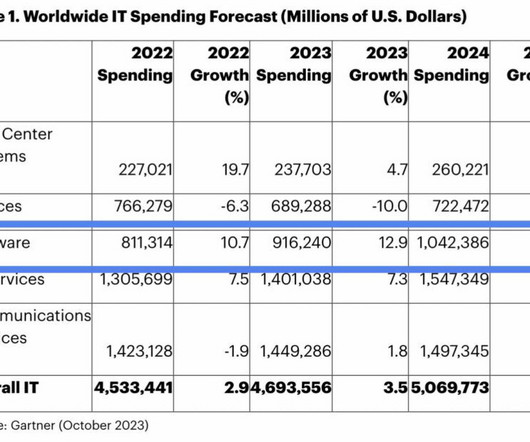

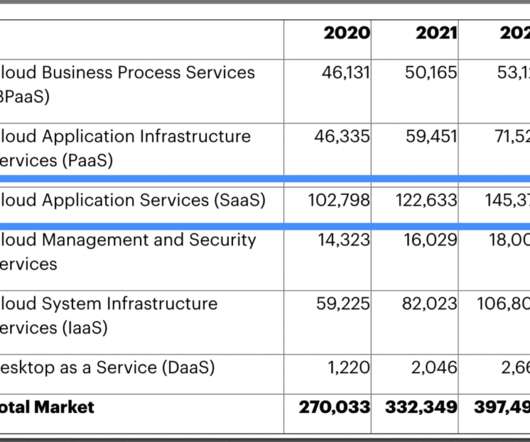

After polling CIOs, Gartner found that total SaaS spend will grow from $100B in 2020 to $140B in 2022: A few interesting implications and learnings: The growth in SaaS buying should give you a +20% a year boost on top of your other sales and marketing efforts. That’s a huge tailwind. This is your time, folks. Go make it happen.

Well, your growth or lack thereof of market share is the #1 sign of potential decay in your product. In a fast-growing market, it’s important to not be quietly left behind just by growing more slowly. You can’t blame it on market changes. Again, they play in the same market. That’s % of marketshare.

Subscribe now Cloud Giants Report Q3 ‘23 Not a great signal for software this week from the Cloud Giants (AWS, Azure and Google Cloud)…After Q2 (3 months ago), the tone from the Cloud Giants around optimizations was largely: optimizations have started to ease, and net new workloads have picked up. Staggering scale already.

Nimble has migrated its market-leading SaaS CRM from Amazon Web Services (AWS) to Microsoft Azure. The migration enables Nimble to tap into Microsoft’s world-class Azure platform and partner ecosystem to scale.

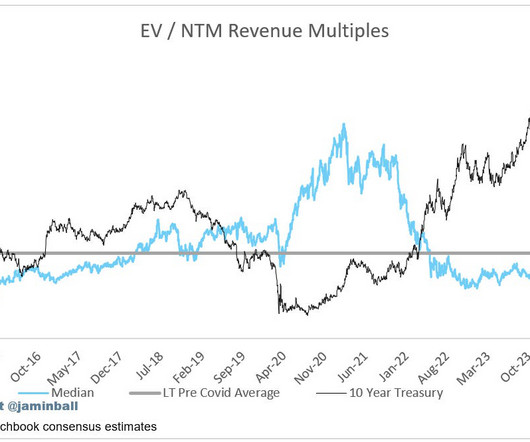

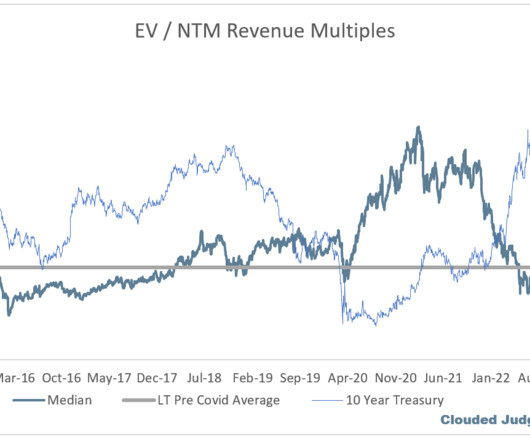

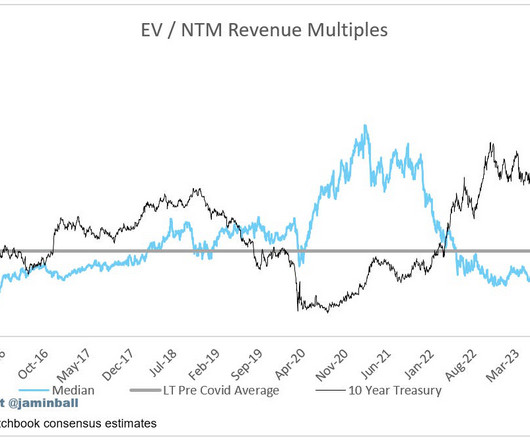

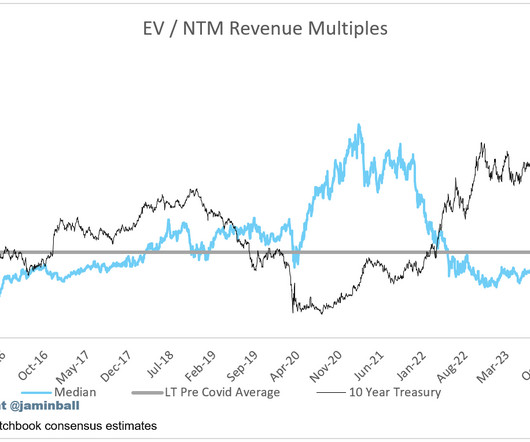

We now have results from the three hypersclaers (AWS / Azure / GCP). The most notable change in tone was Andy Jassy talking about AWS. Multiples shown below are calculated by taking the Enterprise Value (market cap + debt - cash) / NTM revenue. ” Full quote below: “We're seeing a few trends right now.

Amazon on AWS : “…customers are continuing to shift their focus towards driving innovation and bringing new workloads to the cloud. ” Microsoft on Azure : “And I think last quarter, we said one, we are going to continue to have these cycles where people will build new workloads. Follow along to stay up to date!

Google Cloud has announced that Anthos — the company’s software for deploying and managing Kubernetes workloads across multiple on-prem and cloud environments — now supports running workloads on rival cloud platform Amazon Web Services (AWS), with Microsoft Azure support still in preview for now.

" As with many other companies reporting strength in the market, AI & unstructured data workloads are fueling growth. “Yes, we actually saw quite a bit of energy coming from the Azure platform this quarter. Consumption continued to grow in the month of October…Consumption trends have improved.”

If anything, this was the decade they collectively became leaders not just of the technology industry, but of industry itself – Apple overtook ExxonMobil as the world’s most valuable company by market cap in August 2011 (that month again), and then became the first trillion-dollar company by market cap in 2018.

In this session, she shares insights and trends from research conducted this year that can help software buyers and sellers make smarter decisions about software and the market. . and go-to-market partners, to understand what’s happening in the space. . “G2 Go-to-market Partners released a report using G2 data.

The first few months of this year felt like a lot of churning in the market. It looks at the YoY dollar change in quarterly revenue from the hyperscalers (just looking at Azure / AWS because the data goes back further) going back a few years. What I’ve shown below is the market-adjusted stock price reaction.

AWS (Amazon), Azure (Microsoft), and Google Cloud (Google) all reported this week. Azure reported on Tuesday and gave us that glimmer of hope. Then AWS appeared to add fuel to that hope before giving us a huge rug pull. Azure came in at 31% (constant currency). They then guided to 26-27% Azure growth in Q2.

The markets took a while to catch up. That $200b+ of additional Cloud and SaaS spend fueled 50+ Cloud unicorns and massive growth in AWS, Azure, etc. Around 2013 or so, the Cloud started to grow far faster than any of us had thought it would: Amazon Web Services revenue 2018 | Statista. There were dips in 2016 and otherwise.

Cloud Downgrades This week UBS came out with a couple research reports citing concerns in AWS / Azure growth. This brings me back to AWS / Azure downgrades. Multiples shown below are calculated by taking the Enterprise Value (market cap + debt - cash) / NTM revenue. Follow along to stay up to date!

Hyperscalers Report Quarterly Earnings This week we saw AWS (Amazon), GCP (Google) and Azure (Microsoft) report earnings. Overall, it wasn’t pretty… AWS grew 28% when expectations were 30-31%. At the same time, Azure came in below expectations. Follow along to stay up to date! Top 5 Median: 15.8x

Hyperscaler Preview Next week Amazon, Microsoft and Google report earnings and we’ll see Q3 data for AWS, Azure and Google Cloud. Multiples shown below are calculated by taking the Enterprise Value (market cap + debt - cash) / NTM revenue. Said another way, the 10Y today is double what it averaged from 2010 to 2020.

This can make it difficult for software buyers to determine what is real and what is marketing. That’s a big challenge for vendors because your website is your channel to the market, and how can you add value when buyers don’t trust you? You’ll build trust and differentiate yourself in the market. SaaS changed that.

” These are two quotes about AWS on the Amazon earnings call. AWS grew 16% in Q1, but called out growth in April (first month of Q2) was 11%. You can see more detail about their net new ARR added each quarter below Azure Growth came in at 27%, and guided to 25-26% growth for Q3. Overall Stats: Overall Median: 6.4x

Today, the market seems a lot more worried about business fundamentals / growth. Cloud Giants Report Q2 We also got the Q2 quarters from AWS / Azure / GCP this week! Multiples shown below are calculated by taking the Enterprise Value (market cap + debt - cash) / NTM revenue. However, rates are just one variable.

Subscribe now Foundation Models Are to AI what S3 was to the Public Cloud Many people look at 2006 as the birth of the public cloud - the year Amazon launched AWS. Microsoft launched Azure in 2010, and Google launched GCP to the public in 2011 (they launched a preview of Google App Engine in 2008, but made it publicly available in 2011).

We organize all of the trending information in your field so you don't have to. Join 80,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content