This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

With Databricks now one of the largest pre-IPO technology companies, with $10 billion of expected non-dilutive financing and a valuation of $62 billion, Ron’s insights are gold for any revenue leader looking to scale. Our founders focused on adoption first, not revenue, Ron explains. The takeaway? The takeaway?

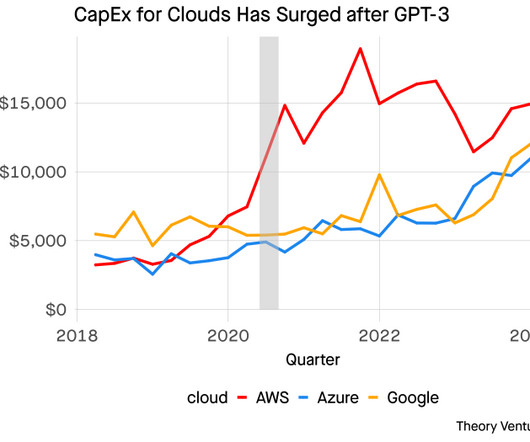

Cloud Capex in Q1 AWS $14 billion Azure $14 billion Google Cloud $12 billion These are not one-time investments, but part of a broader trend that started to occur after the introduction of GPT 3 in mid-2020 Amazon was the first to invest significantly. “Moving to AWS.

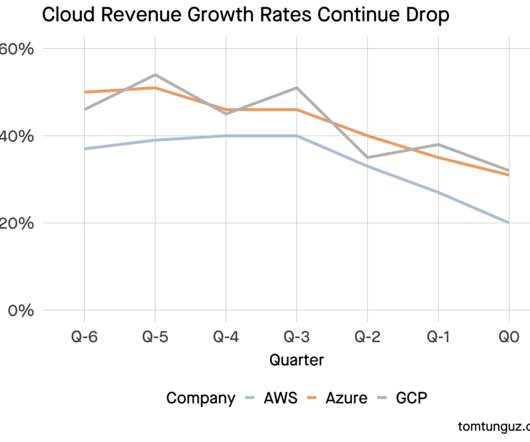

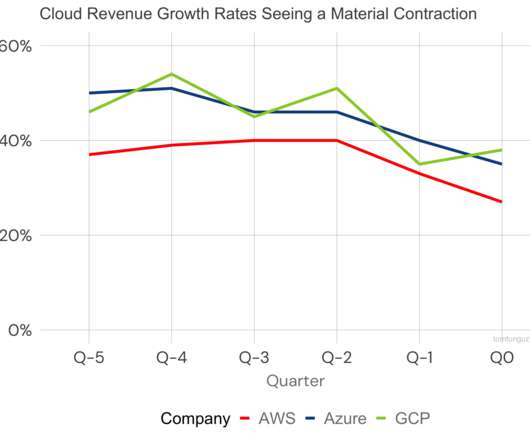

So follow AWS, Azure and Google Cloud. Let’s look a whole level up to the real canaries-in-the-coalmine: AWS, Azure and Google Cloud. And AWS grew 37% at a $74B run-rate , down a bit from 39% the prior quarter but still adding an insane amount of new revenue. For now, they are still on fire.

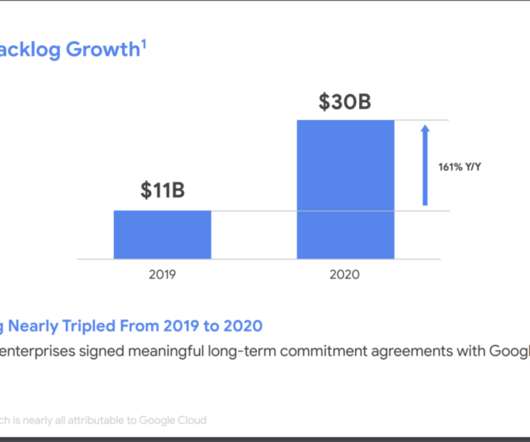

But are AWS, Azure and Google Cloud just too big for us to learn from? Google Cloud sees Cloud revenues tripling in the next 5 years. Google Cloud continues its march upmarket, competing with Azure. You can see that here vividly, with Google Cloud having a $30B backlog of signed revenue on top of its $13B in ARR.

A year ago, AWS, GCP, & Azure averaged 44% annual growth. Amazon: We expect [customer] optimization efforts will continue to be a headwind to AWS growth in at least the next couple of quarters. So So far in the first month of the year, AWS year-over-year revenue growth is in the mid-teens.

The charts below show the change in quarterly revenue YoY (so Q1 ‘24 rev - Q1 ‘23 rev) going back to 2017. It’s worth pointing out that Azure is a bit above the long term trendline, while AWS is still below (but accelerating up). Beating consensus revenue estimates is the first aspect of a successful quarter.

Focusing on smaller developers, in some ways it’s been a bit overshadowed by AWS, Azure, and Google Cloud. DigitialOcean doesn’t want to take AWS, Azure and Google on in the enterprise and doesn’t really try. They are only 15% of the customers, but 83% of the revenue. That’s impressive.

Typically support consumes about perhaps 5%-7% of your revenue at scale (excluding customer success) in most SaaS models. Another 5%-7% go to core infrastructure costs (AWS, Azure, Snowflake, etc). Dear SaaStr: What is The Average Ratio of Support Staff to Customer Count in SaaS?

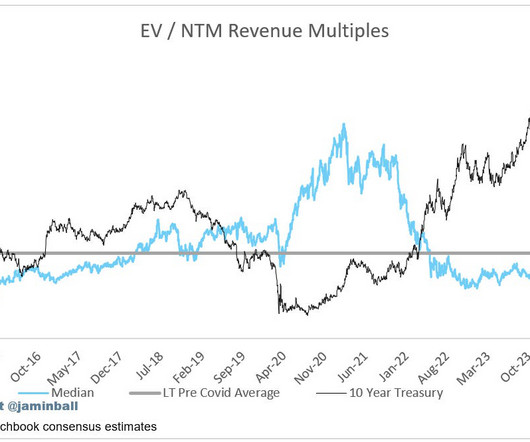

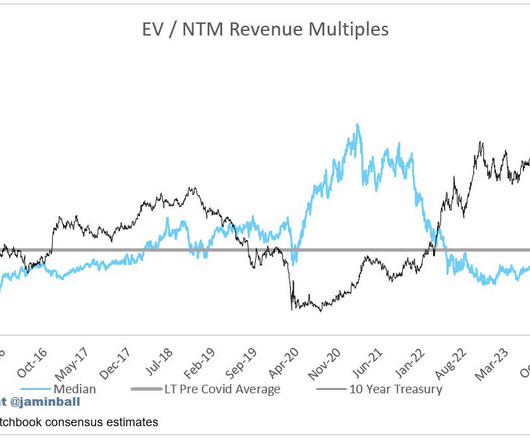

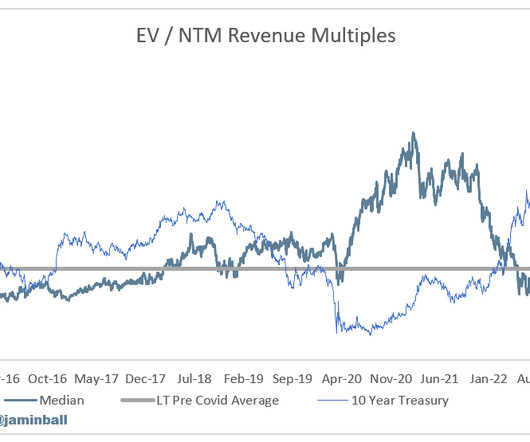

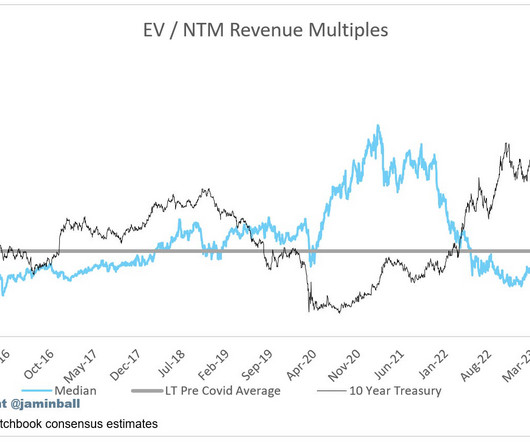

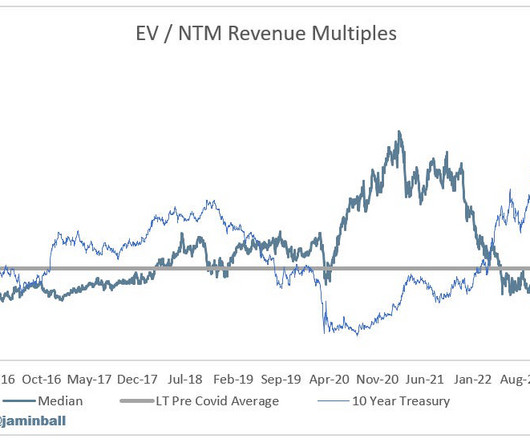

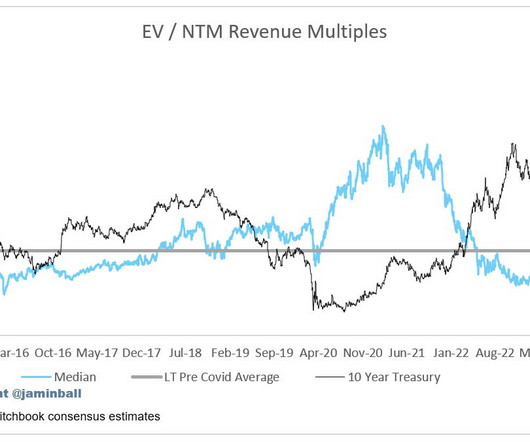

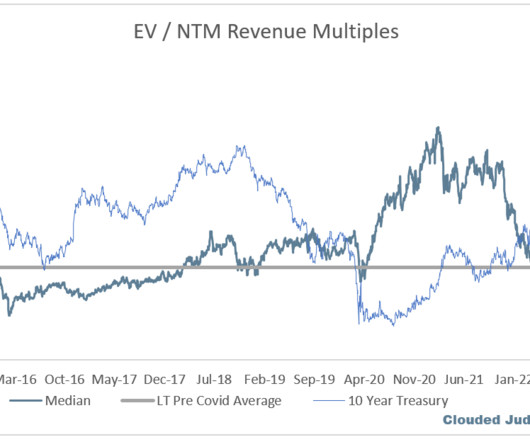

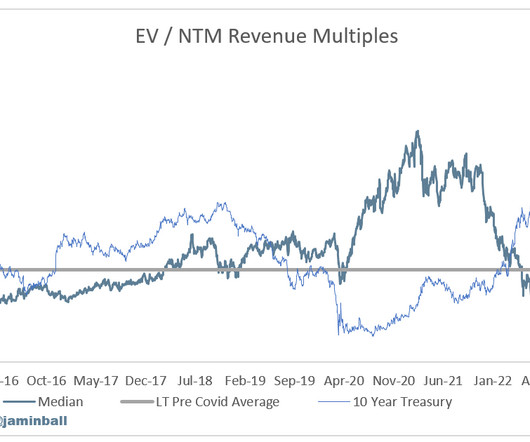

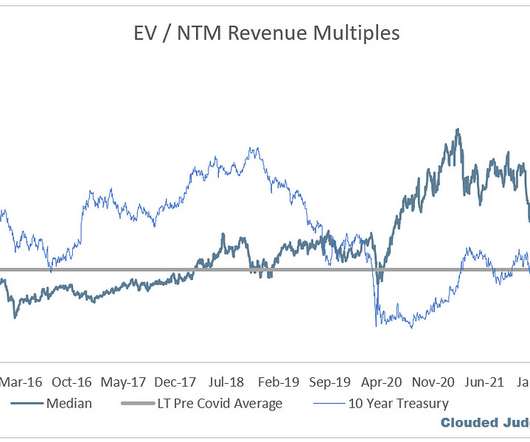

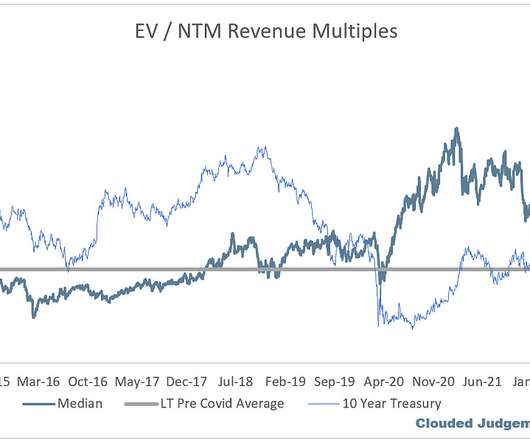

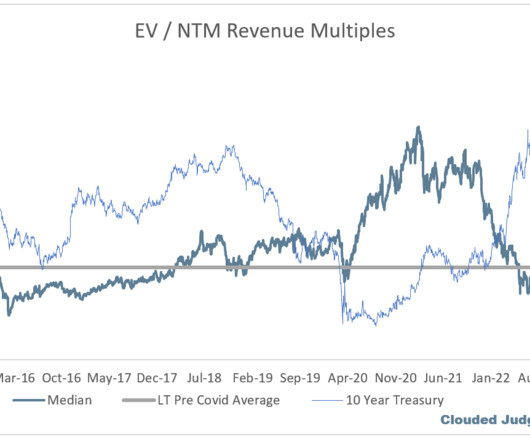

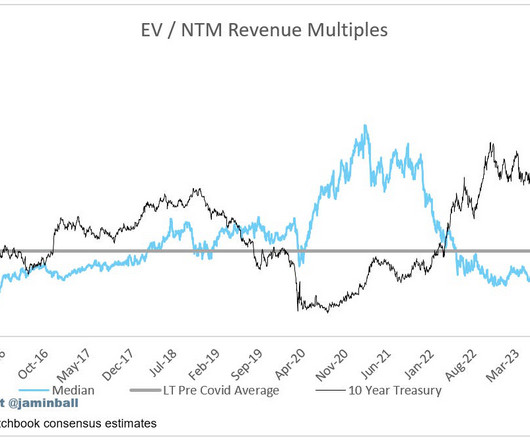

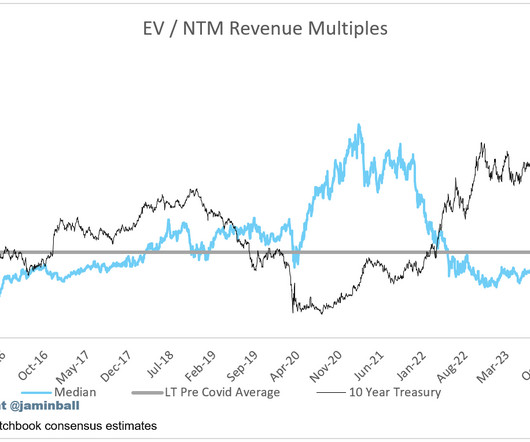

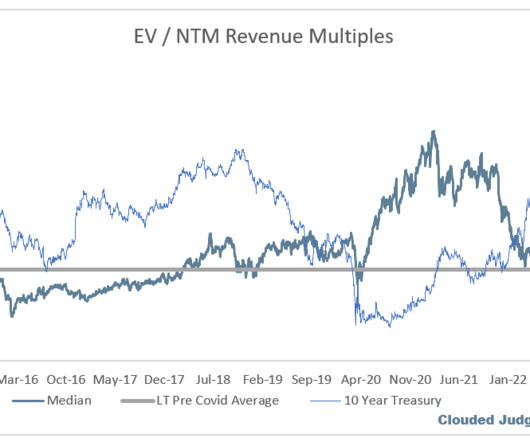

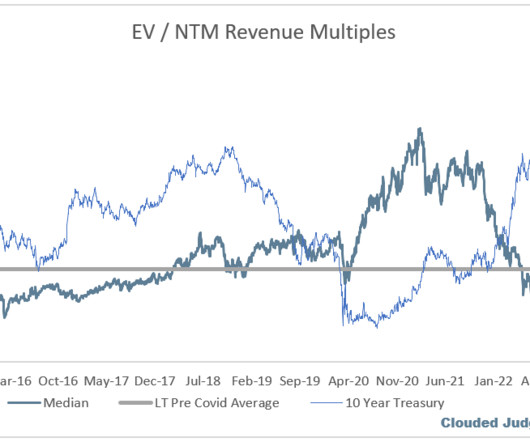

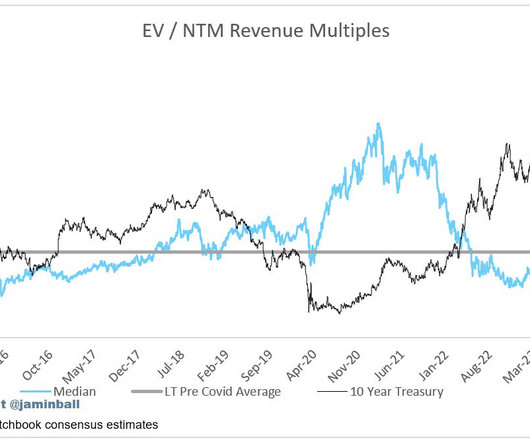

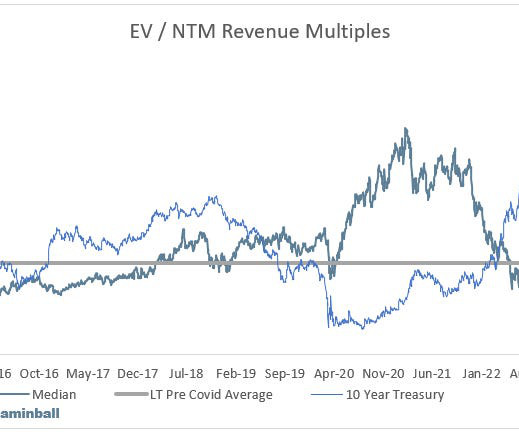

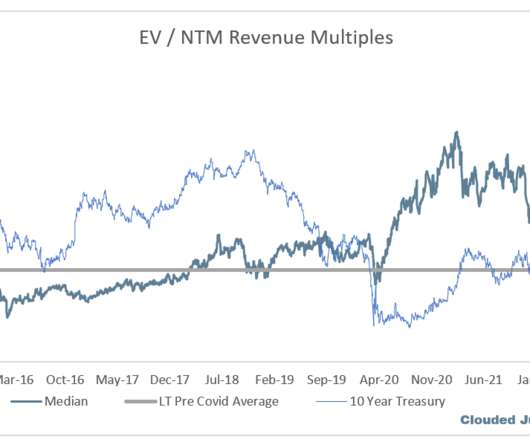

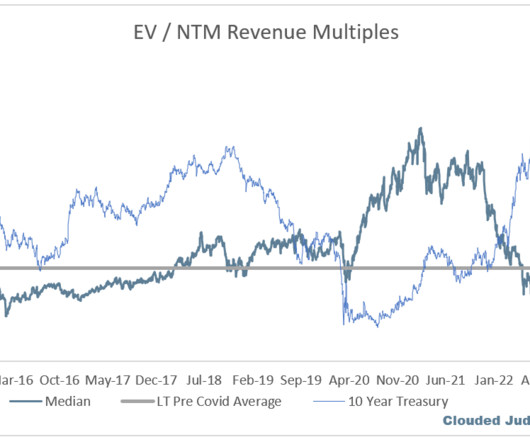

They each have some of the largest cloud businesses in the world in AWS, Azure and Google Cloud respectively. Revenue multiples are a shorthand valuation framework. Multiples shown below are calculated by taking the Enterprise Value (market cap + debt - cash) / NTM revenue. Overall, there was weakness across the board.

Many have used Digital Ocean at the cheaper, simpler version of AWS-Azure-Digital Ocean to get going fast and quickly. But it’s raining cash, and earnings per share is growing 22% — faster than revenue. And if so, maybe that’s Digital Ocean. If you haven’t heard of Digital Ocean, ask your developer.

Microsoft Azure. Microsoft Azure grew 40% y/y, tying the fastest quarterly growth rate in the past 5 quarters. Google’s growth rate fell to 35%, a 29% decline from the trailing 4 quarter average of 49% annual revenue growth. Here are some hypotheses: Google may have greater customer concentration in GCP than Azure.

Ultimately — revenue multiples. Revenue multiples are how much VCs, investors, and ultimately, an IPO and public markets will value each dollar of revenue. Revenue multiples don’t affect customers, or even revenue itself. That revenue multiples should rise from where they were in 2019.

Microsoft Azure. Infrastructure revenue growth averaged 33% this quarter, which is astounding considering we’re talking about businesses that sum to more than $50b of revenue per quarter. At a 7x multiple of revenue, that is another $84b of market cap creation, in theory. Google Cloud Platform. Amazon Web Services.

As a result, software vendors often see an uptick in revenue and bookings during these periods. Top 10 EV / NTM Revenue Multiples Top 10 Weekly Share Price Movement Update on Multiples SaaS businesses are generally valued on a multiple of their revenue - in most cases the projected revenue for the next 12 months.

Which means better customer relationships, more data, and new sources of revenue. Secureframe allows companies to get compliant within weeks, rather than months and monitors 100+ services, including AWS, GCP, and Azure.

Using the Drift Conversation Cloud, businesses can personalize experiences that lead to more quality pipeline, revenue and lifelong customers. More than 5,000 customers use Drift to deliver a more enjoyable and more human buying experience that builds trust and accelerates revenue. Usually, it takes a paradigm shift to grow.

You need an efficient way to keep your customers successful, reduce churn, drive adoption, and increase net revenue retention. Secureframe allows companies to get compliant within weeks, rather than months and monitors 100+ services, including AWS, GCP, and Azure.

We help B2B SaaS marketers turn organic search into a source of repeatable revenue through software and coaching. The platform automates the provisioning of your application to the cloud (AWS, GCP, Azure), integrating cloud ops, DevOps, and security/compliance with 24×7 monitoring and support.

In my 148 public SaaS companies (including most of the categories of this list but not AWS, Azure, GCP) the aggregate revenue is $185B. No matter what, the wave of enterprise spending that fueled 100 SaaS and Cloud unicorns is just getting bigger and strong. This is your time, folks. Go make it happen.

Subscribe now Cloud Giants Report Q3 ‘23 Not a great signal for software this week from the Cloud Giants (AWS, Azure and Google Cloud)…After Q2 (3 months ago), the tone from the Cloud Giants around optimizations was largely: optimizations have started to ease, and net new workloads have picked up. Staggering scale already.

And it’s one of the three large cloud vendors that we all know: Microsoft, AWS, and Google. Azure’s marketplace has over 4 million monthly visitors. AWS’s marketplace has seen 1.5 Like I said, we run 100% of our platform on AWS, so the fit was great. It was pretty easy to drive that from our side.

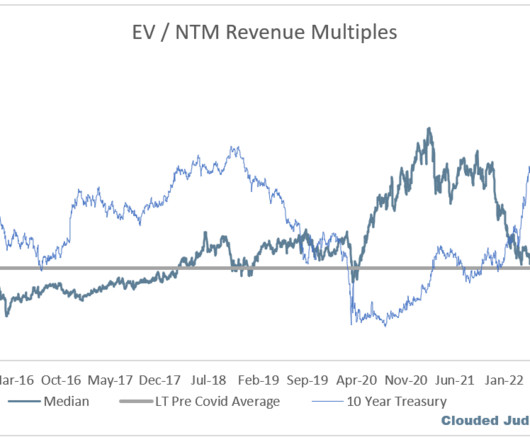

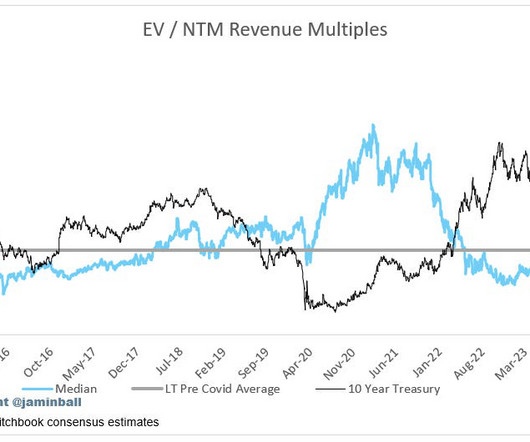

We now have results from the three hypersclaers (AWS / Azure / GCP). The most notable change in tone was Andy Jassy talking about AWS. Revenue multiples are a shorthand valuation framework. Multiples shown below are calculated by taking the Enterprise Value (market cap + debt - cash) / NTM revenue.

Amazon on AWS : “…customers are continuing to shift their focus towards driving innovation and bringing new workloads to the cloud. ” Microsoft on Azure : “And I think last quarter, we said one, we are going to continue to have these cycles where people will build new workloads. Follow along to stay up to date!

“Q3 product revenue grew 34% year-over-year to reach $698 million. “Yes, we actually saw quite a bit of energy coming from the Azure platform this quarter. Non-GAAP adjusted free cash flow was $111 million, representing 7% year-over-year growth. Results reflect strong execution in a broadly stabilizing macro environment.

Subscribe now ARR (Annual Recurring Revenue) vs ERR (Experimental Runrate Revenue) ARR (Annual Recurring Revenue) is one of the most popular SaaS (Non-GAAP) metrics. Many investors laugh (and some rightly so) at the fact that software companies’ valuations are often described as a multiple of revenue.

Around 2013 or so, the Cloud started to grow far faster than any of us had thought it would: Amazon Web Services revenue 2018 | Statista. That $200b+ of additional Cloud and SaaS spend fueled 50+ Cloud unicorns and massive growth in AWS, Azure, etc. The markets took a while to catch up. There were dips in 2016 and otherwise.

AWS (Amazon), Azure (Microsoft), and Google Cloud (Google) all reported this week. Azure reported on Tuesday and gave us that glimmer of hope. Then AWS appeared to add fuel to that hope before giving us a huge rug pull. Azure came in at 31% (constant currency). They then guided to 26-27% Azure growth in Q2.

It looks at the YoY dollar change in quarterly revenue from the hyperscalers (just looking at Azure / AWS because the data goes back further) going back a few years. If we break this down and look at Azure and AWS independently (graphs below), you’ll see how the AWS “swings” were a lot more volatile.

Hyperscaler Preview Next week Amazon, Microsoft and Google report earnings and we’ll see Q3 data for AWS, Azure and Google Cloud. Office 365 Copilot, for example, doesn’t go live until November and we most likely won’t see meaningful revenue from it until next year. Overall Stats: Overall Median: 5.7x

Cloud Downgrades This week UBS came out with a couple research reports citing concerns in AWS / Azure growth. This brings me back to AWS / Azure downgrades. Revenue multiples are a shorthand valuation framework. Every week I’ll provide updates on the latest trends in cloud software companies.

Hyperscalers Report Quarterly Earnings This week we saw AWS (Amazon), GCP (Google) and Azure (Microsoft) report earnings. Overall, it wasn’t pretty… AWS grew 28% when expectations were 30-31%. At the same time, Azure came in below expectations. Follow along to stay up to date! Top 5 Median: 15.8x

” These are two quotes about AWS on the Amazon earnings call. AWS grew 16% in Q1, but called out growth in April (first month of Q2) was 11%. You can see more detail about their net new ARR added each quarter below Azure Growth came in at 27%, and guided to 25-26% growth for Q3. Overall Stats: Overall Median: 6.4x

Cloud Giants Report Q2 We also got the Q2 quarters from AWS / Azure / GCP this week! Quarterly Reports Summary Top 10 EV / NTM Revenue Multiples Top 10 Weekly Share Price Movement Update on Multiples SaaS businesses are generally valued on a multiple of their revenue - in most cases the projected revenue for the next 12 months.

Subscribe now Foundation Models Are to AI what S3 was to the Public Cloud Many people look at 2006 as the birth of the public cloud - the year Amazon launched AWS. Microsoft launched Azure in 2010, and Google launched GCP to the public in 2011 (they launched a preview of Google App Engine in 2008, but made it publicly available in 2011).

Next week we get all 3 hyperscalers reporting (AWS from Amazon, Azure from Microsoft, and GCP from Google). Let’s double click on Azure. On AWS, in their Q4 earnings call they said AWS was growing “mid teens” in January (down from 20% in Q4). Revenue multiples are a shorthand valuation framework.

AI = Data + Compute I’ll continue beating this drum, but we got two great quotes from Azure and AWS this week. ” Then at AWS Summit they called out “Your data is your differentiator when it comes to Generative AI.” AWS reports next week. Revenue multiples are a shorthand valuation framework.

And no one raised full year guide >2% The median “beat” (Q1 revenue over Q1 consensus estimates) was 1.5%, which is the lowest it’s been in the last 4 years Overall, it’s been a TOUGH quarter for software companies. Revenue multiples are a shorthand valuation framework. Overall Stats: Overall Median: 5.7x

Expansion revenue is still declining (we see this in falling net retention rates), but gross retention remains strong. Usage on Snowflake is driven by queries run on Snowflake Azure: Neutral Tone With Strength in AI Overall I’d characterize Azure’s quarter as a net positive. Overall Stats: Overall Median: 5.7x

” As growth starts to slow, it gets harder and harder to justify using revenue multiples as a primary valuation metric. Any kind of inference really can rack up bills quickly (see growth in hyperscaler revenue…), and AI talent isn’t cheap. Revenue multiples are a shorthand valuation framework.

Hyperscalers (AWS, Azure, GCP as companies look for cloud GPUs who aren’t building out their own data centers) Infra (Data layer, orchestration, monitoring, ops, etc) Durable Applications We’ve clearly well underway of the first 3 layers monetizing. Revenue multiples are a shorthand valuation framework.

In the short term, enjoy the ride as the chase continues 😊 Kind of related to all of this - we now have seen the Q4’s from AWS, Azure and Google Cloud. Revenue multiples are a shorthand valuation framework. Multiples shown below are calculated by taking the Enterprise Value (market cap + debt - cash) / NTM revenue.

While the overall median revenue multiple of the software universe is ~6x (which is ~25% below the long term average of ~8x), high growth software is currently trading at a premium to it’s long term average (9.4x The hyperscalers (AWS, Azure, GCP) are seeing some uptick, but this is largely from selling compute (ie cloud GPUs).

This is why we’re seeing more and more SaaS companies—Datadog, Twilio, AWS, Snowflake, and Stripe, to name a few—find success with product led growth paired with usage-based pricing. Though it was pioneered in the infrastructure layer (think: AWS and Azure), it’s becoming increasingly popular for API-based products and application software.

Many people are doing great, even private companies like Netskope, which are growing over 30% at $500M in revenue. Canva is growing at 40% and has a revenue of $2.3B. Klaviyo is growing 42% at $750M, coming up on a billion in revenue, and number one in the Shopify ecosystem. Samsara is growing 39% at $1.1B. What’s going on here?

We organize all of the trending information in your field so you don't have to. Join 80,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content