This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Subscribe now Amazon ReInvent This week Amazon had their annual AWS ReInvent conference. ” AWS fully embracing the breadth over depth approach. Looking at the mid to long term, we feel very optimistic about the outlook for strong AWS growth. Follow along to stay up to date! This year, there was tons of experimentation.

Fast forward to the launch of AWS and the public cloud. Most public companies don’t report net new ARR, so I’m taking an implied ARR metric (quarterly subscription revenue x 4). Companies that do not disclose subscription rev have been left out of the analysis and are listed as NA. So why try and compete now?

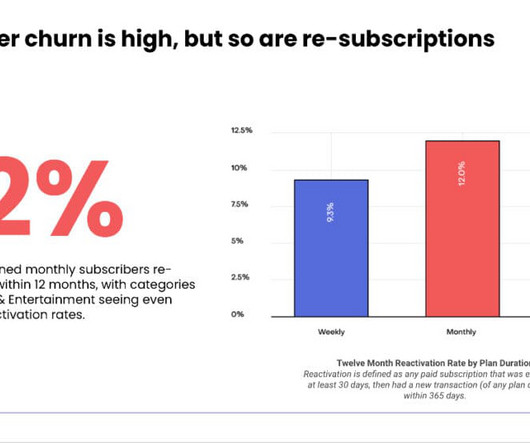

In this week’s Workshop Wednesday, RevenueCat CEO Jacob Eiting and Growth Advocate David Barnard share their annual State of Subscription Apps report with us. So, let’s look at the state of subscription apps and how B2B SaaS can learn from it. Churn is much higher on consumer subscriptions, but you have higher expansion revenue.

net retention and CAC payback). It’s worth pointing out that Azure is a bit above the long term trendline, while AWS is still below (but accelerating up). Net Revenue Retention High net revenue retention is the fourth aspect of a successful quarter, and one of my favorite metrics to evaluate in private SaaS companies.

Doesn’t ARR stand for Annual Recurring Revenue? ARR now really means revenue with 100%+ Net Revenue Retention. 50% revenue from software (recurring), 50% from payments (not-recurring). . You pay a subscription for websites to help you sell stuff. Well of course it does. 220m in ARR, $13B market cap.

8 Out of 10 of Top Deals Were Sourced or Influenced by Partners And more than 40% of their total business is invoiced via channel partners. AWS alone generated $175m of contract value for Okta, growing 130%. GRR / Logo Retention in Mid 90% Range. And a few other interesting learnings: #6. Strong, and what we’d expect.

ChartMogul is an analytics platform to help you run your subscription business. Our mission is to build powerful and secure cloud software for subscription businesses of all sizes, with a strong emphasis on good design and ease of use.

They each have some of the largest cloud businesses in the world in AWS, Azure and Google Cloud respectively. Most public companies don’t report net new ARR, so I’m taking an implied ARR metric (quarterly subscription revenue x 4). Overall, there was weakness across the board.

The hyperscalers (AWS, Azure, GCP) are always some of the first companies to report earnings during earnings season (coming up in 2 weeks), and there’s always a read through for consumption names (meaning people believe there’s a correlation). Cloudflare is up 17%. Datadog is up 14%. Mongo is up 16%. Snowflake is up 14%.

We generate over 90% of our revenue from self-serve channels — users who purchase a subscription through our app or website. As a result, we may be unable to address any retention issues with specific users in a timely manner, which could harm our business.” We “ do not track the retention rate of our individual users”.

net retention and CAC payback). It looks at the YoY dollar change in quarterly revenue from the hyperscalers (just looking at Azure / AWS because the data goes back further) going back a few years. Through these interactions, I’ve built up mental benchmarks for metrics on which I place extra emphasis. Is Software Rebounding?

In the application layer for startups, many face challenges that boil down to retention. If you’re a startup building in this space, retention is a challenge, and you’ll need to be more strategic. Some of that is by launching add-on products that can be priced as subscription fees or transactional per conversation.

We now have results from the three hypersclaers (AWS / Azure / GCP). The most notable change in tone was Andy Jassy talking about AWS. Most public companies don’t report net new ARR, so I’m taking an implied ARR metric (quarterly subscription revenue x 4).

Amazon on AWS : “…customers are continuing to shift their focus towards driving innovation and bringing new workloads to the cloud. Azure (excluding Azure AI) continued to decelerate, and while AWS did come in ahead of expectations, it wasn’t a blow out. Follow along to stay up to date!

Subscribe now Foundation Models Are to AI what S3 was to the Public Cloud Many people look at 2006 as the birth of the public cloud - the year Amazon launched AWS. Most public companies don’t report net new ARR, so I’m taking an implied ARR metric (quarterly subscription revenue x 4). Follow along to stay up to date!

” We saw some green shoots in AWS and a few other consumption names, and overall sentiment seemed more positive. Partly due to larger layoffs, as well as stronger bookings And finally - net retention. Not surprising, net retention continued to fall.

Subscribe now Cloud Giants Report Q3 ‘23 Not a great signal for software this week from the Cloud Giants (AWS, Azure and Google Cloud)…After Q2 (3 months ago), the tone from the Cloud Giants around optimizations was largely: optimizations have started to ease, and net new workloads have picked up. That is not new.”

Hyperscaler Preview Next week Amazon, Microsoft and Google report earnings and we’ll see Q3 data for AWS, Azure and Google Cloud. Most public companies don’t report net new ARR, so I’m taking an implied ARR metric (quarterly subscription revenue x 4).

In our webinar, 2022 SaaS retention benchmarks , SaaS Capital Manager Director Rob Belcher shares the results from their 11th annual B2B SaaS benchmarking survey. You can download the full report for net retention and gross retention benchmarks as well as retention metrics in relation to ACV, growth, size, and more.

Hyperscalers Report Quarterly Earnings This week we saw AWS (Amazon), GCP (Google) and Azure (Microsoft) report earnings. Overall, it wasn’t pretty… AWS grew 28% when expectations were 30-31%. Every week I’ll provide updates on the latest trends in cloud software companies. Follow along to stay up to date!

Cloud Downgrades This week UBS came out with a couple research reports citing concerns in AWS / Azure growth. This brings me back to AWS / Azure downgrades. This was the worst tone that we’ve heard in years from large AWS/Azure partners, a group that usually expresses different shades of optimism about AWS/Azure growth.”

Enterprise software businesses strive for 90-95% gross retention (generally the percent of revenue that sticks with you vs churns altogether), with net expansion in the 120%+ range (the aggregate change in expansion - contraction - churned revenue). Namely, retention!! The biggest culprit is describing non recurring revenue as ARR.

AWS (Amazon), Azure (Microsoft), and Google Cloud (Google) all reported this week. Then AWS appeared to add fuel to that hope before giving us a huge rug pull. After all, they had a lot of AI tailwinds, and benefited tremendously from consolidation (without a headwind of a larger base of smaller startups, like AWS).

” These are two quotes about AWS on the Amazon earnings call. AWS grew 16% in Q1, but called out growth in April (first month of Q2) was 11%. Most public companies don’t report net new ARR, so I’m taking an implied ARR metric (quarterly subscription revenue x 4).

Cloud Giants Report Q2 We also got the Q2 quarters from AWS / Azure / GCP this week! Most public companies don’t report net new ARR, so I’m taking an implied ARR metric (quarterly subscription revenue x 4). Companies that do not disclose subscription rev have been left out of the analysis and are listed as NA.

Did you know that 60% of SaaS companies reported a negative impact on customer retention and upsell deals due to the pandemic? Customer retention, along with new customer acquisition, has been challenging for most companies when the pandemic hit. And, as you know, a better customer experience leads to better customer retention.

This can lead to an airpocket of valuation as companies transition to a different primary valuation metric Outside of the hypserscalers (Azure, AWS, GCP) who have uniquely benefited from AI revenue (mainly selling compute), everyone else has largely struggled. Coming in to Q1 there was broader optimism. Q4’s were generally good!

Next week we get all 3 hyperscalers reporting (AWS from Amazon, Azure from Microsoft, and GCP from Google). On AWS, in their Q4 earnings call they said AWS was growing “mid teens” in January (down from 20% in Q4). Companies that do not disclose subscription rev have been left out of the analysis and are listed as NA.

I’m looking at it and I’m like, “Who’s got the Wall Street Journal subscription? Because sales folks want to close the biggest deal and they may not like downgrades or logo retention, how are you thinking about this issue? For us, it’s been, “Migrate things that you have on invoice over to card.”

Expansion revenue is still declining (we see this in falling net retention rates), but gross retention remains strong. Most public companies don’t report net new ARR, so I’m taking an implied ARR metric (quarterly subscription revenue x 4). New customer growth seems to be picking up.

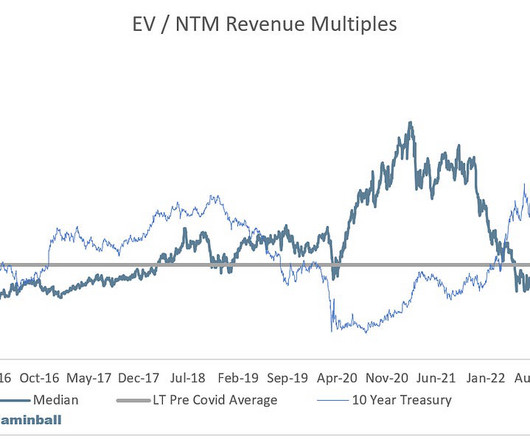

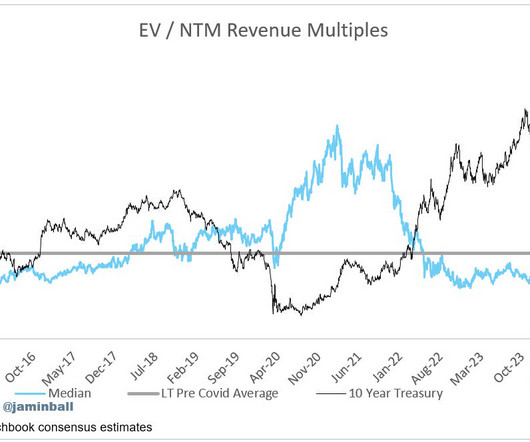

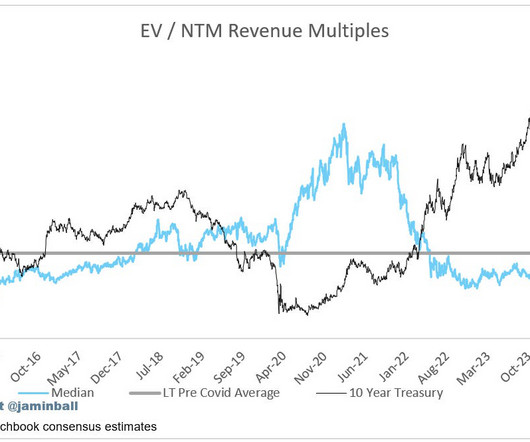

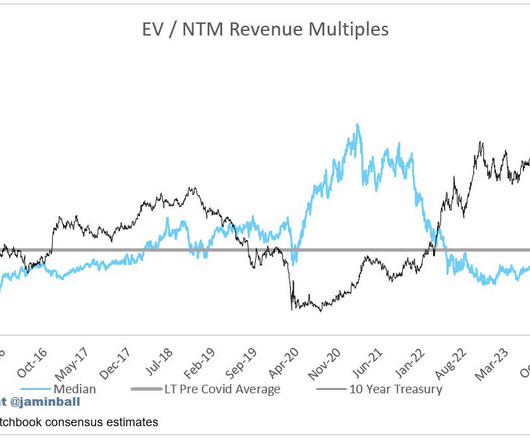

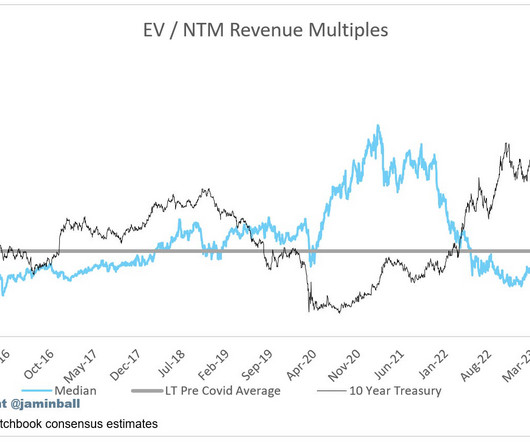

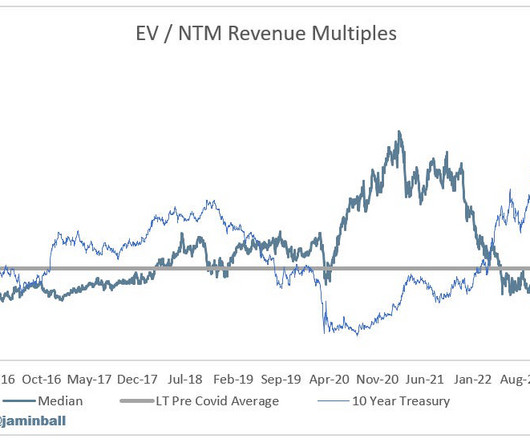

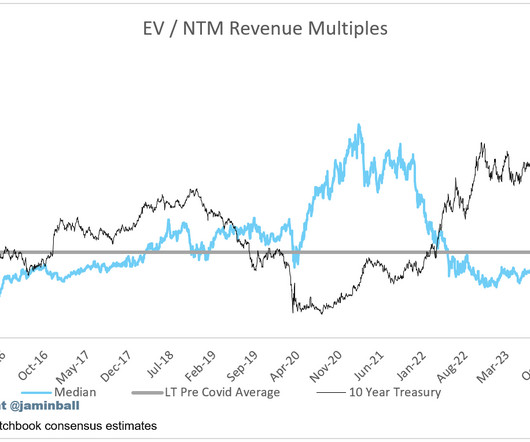

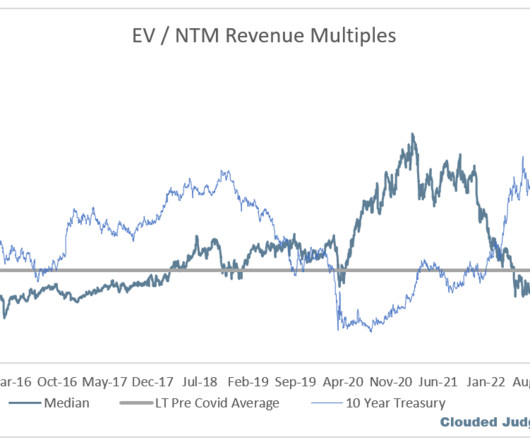

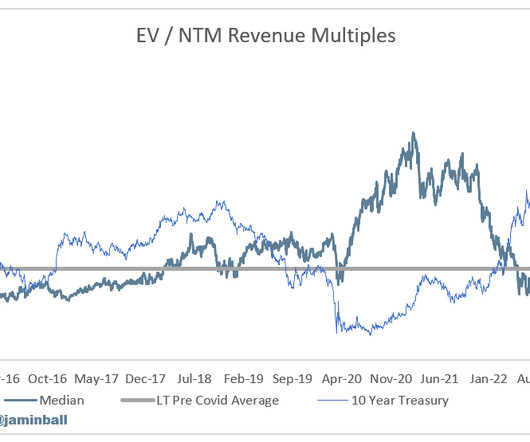

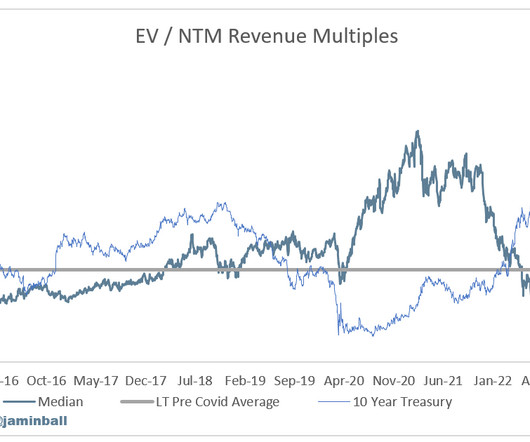

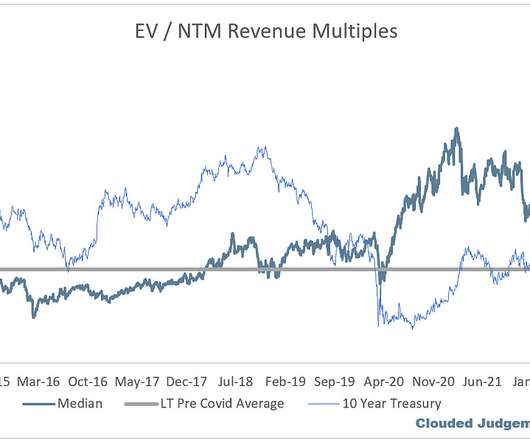

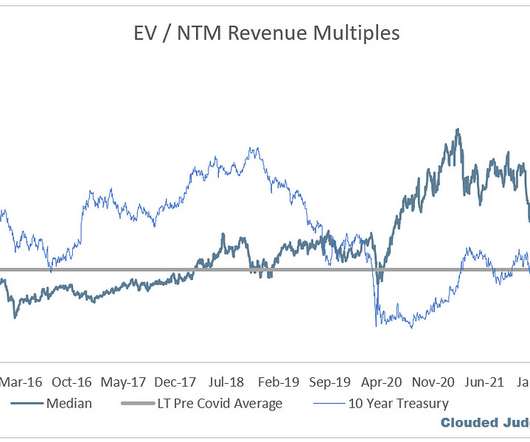

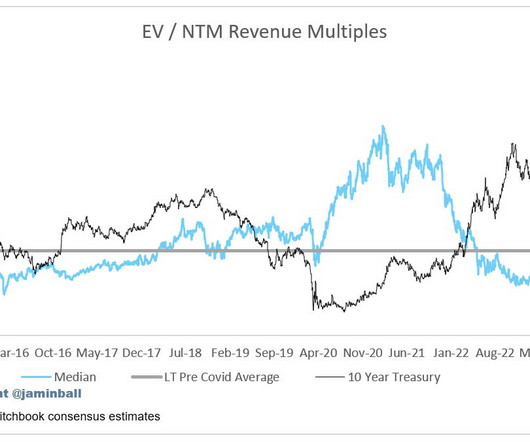

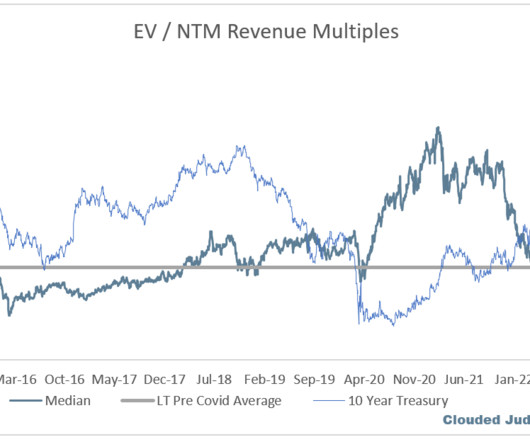

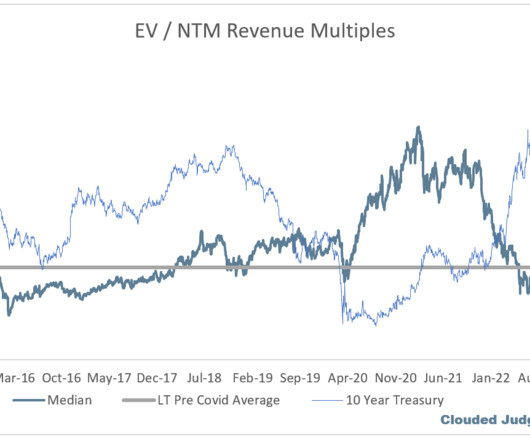

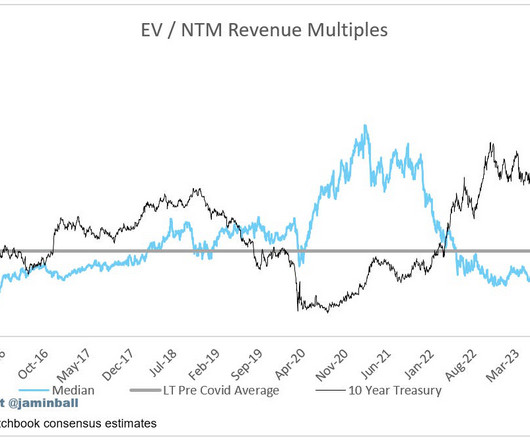

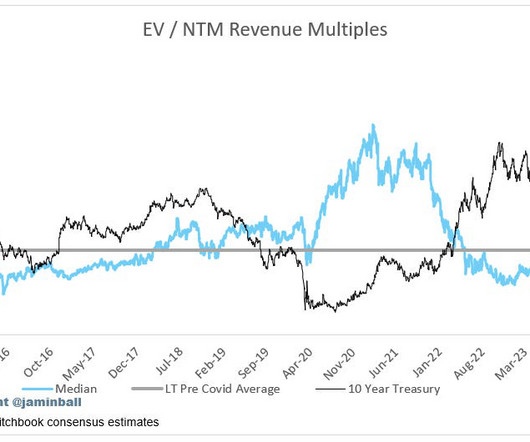

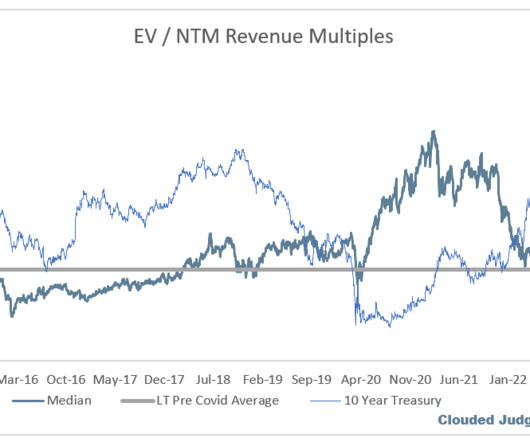

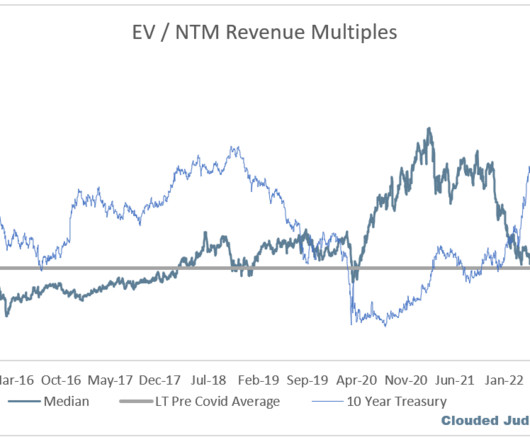

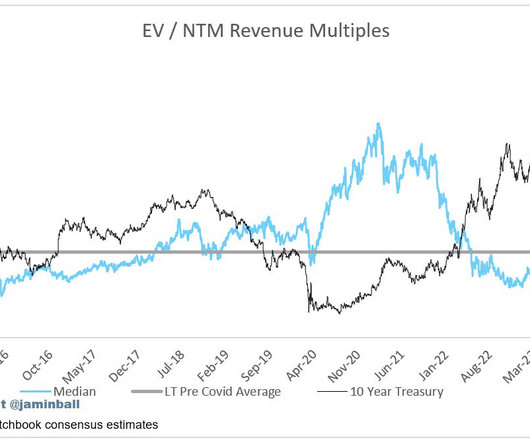

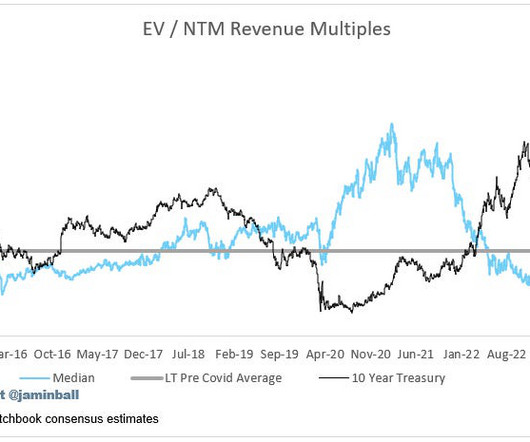

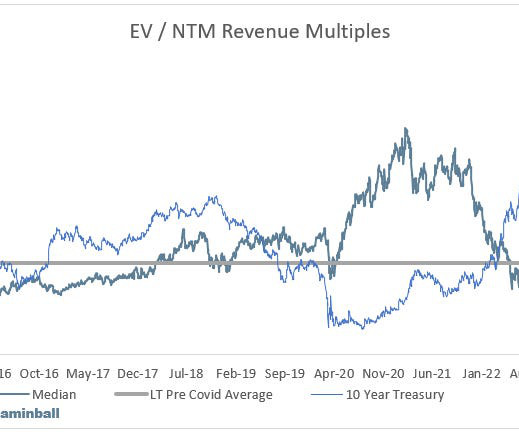

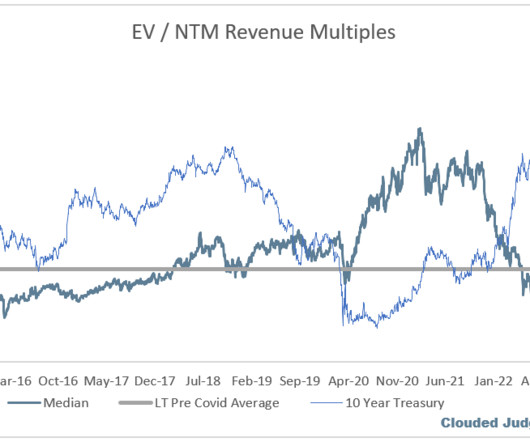

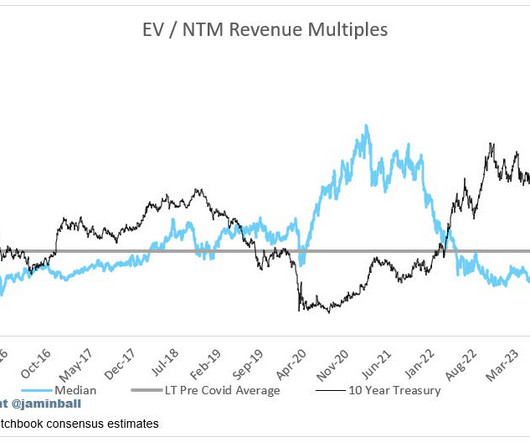

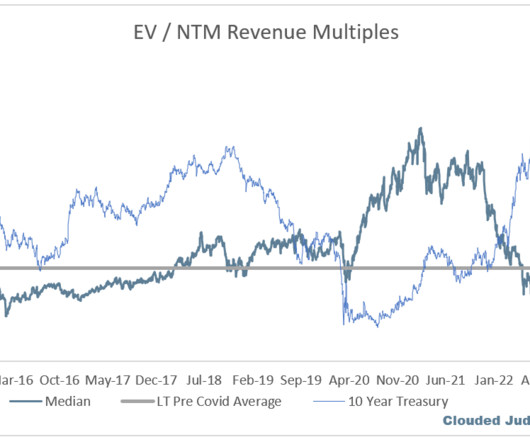

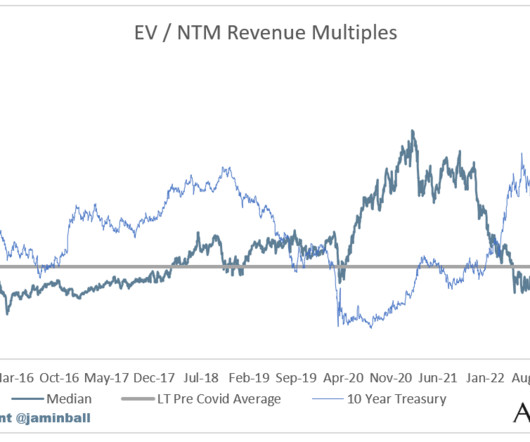

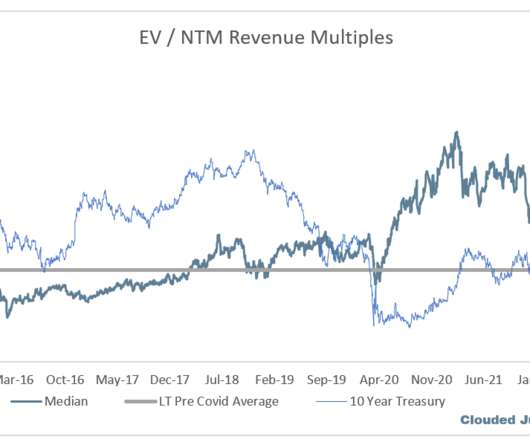

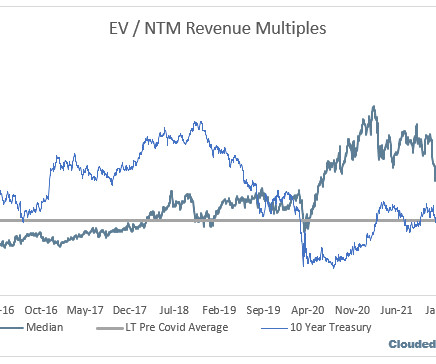

All 3 (AWS, Azure, GCP) saw positive reacceleration Quarterly Reports Summary Top 10 EV / NTM Revenue Multiples Top 10 Weekly Share Price Movement Update on Multiples SaaS businesses are generally valued on a multiple of their revenue - in most cases the projected revenue for the next 12 months.

” From AWS (paraphrased): They said they expect the reaccleration they saw in Q4 to continue into 2024 2024 Estimate Updates One important metric I’m tracking this quarter is the change in 2024 estimates pre / post earnings. Companies that do not disclose subscription rev have been left out of the analysis and are listed as NA.

This is why we’re seeing more and more SaaS companies—Datadog, Twilio, AWS, Snowflake, and Stripe, to name a few—find success with product led growth paired with usage-based pricing. But growing with a usage-model is not as straightforward as traditional subscription SaaS. Then they tell their boss what to buy.

Hyperscalers (AWS, Azure, GCP as companies look for cloud GPUs who aren’t building out their own data centers) Infra (Data layer, orchestration, monitoring, ops, etc) Durable Applications We’ve clearly well underway of the first 3 layers monetizing. Model providers (OpenAI, Anthropic, etc as companies start building out AI).

AI = Data + Compute I’ll continue beating this drum, but we got two great quotes from Azure and AWS this week. ” Then at AWS Summit they called out “Your data is your differentiator when it comes to Generative AI.” AWS reports next week. ” Data is more important than ever! So what did we learn?

I asked ChatGPT how many price changes AWS has made to S3 since it’s inception in 2006, and the answer it gave me was 65. Most public companies don’t report net new ARR, so I’m taking an implied ARR metric (quarterly subscription revenue x 4). Absent the Llama 3.1 release, would this feature have been made free?

The good news is gross retention (ie churn) stayed constant. The hyperscalers (AWS, Azure, GCP) are seeing some uptick, but this is largely from selling compute (ie cloud GPUs). Most public companies don’t report net new ARR, so I’m taking an implied ARR metric (quarterly subscription revenue x 4).

AWS growth seems to be re-accelerating, and qualitative feedback from a number of companies in Q2 (especially those with July quarter ends) suggested new customer bookings conversations were picking up. Most public companies don’t report net new ARR, so I’m taking an implied ARR metric (quarterly subscription revenue x 4).

In the short term, enjoy the ride as the chase continues 😊 Kind of related to all of this - we now have seen the Q4’s from AWS, Azure and Google Cloud. Most public companies don’t report net new ARR, so I’m taking an implied ARR metric (quarterly subscription revenue x 4). Lots of deceleration in growth.

I’m going to skip by my life story, and how I grew up as a small child in India, and how the dusty streets influenced my take on unit economics, and SaaS subscription models. I’m going to talk about retention. We’ll talk about retention. We all know retention is important. Here’s the mistake.

Appcues enhances user onboarding, adoption , and retention with targeted walkthroughs, in-app messaging, and feature adoption tools. Quickbooks and Xero are accounting SaaS products that help you send invoices, track expenses, and process payroll. You don’t handle maintenance or updates. What are the benefits of the SaaS model?

You hear the terms SaaS, subscription, term licenses and perpetual license software tossed around frequently. We sometimes hear companies call themselves “SaaS” companies, because they sell subscriptions, but they do not host software. The product is hosted by the vendor or a 3 rd party (like AWS).

The majority of COGS (revenue less COGS = gross profit) fall in hosting costs (ie AWS), and some customer support. Most public companies don’t report net new ARR, so I’m taking an implied ARR metric (quarterly subscription revenue x 4). This post and the information presented are intended for informational purposes only.

The pricing model, which leads to increases or decreases in revenue based on how much customers engage with a service, has been gaining on the more traditional subscription model as the main way SaaS companies make money. It has tended to be used most in infrastructure platforms, like AWS, Google Cloud, and Azure. Enterprise companies.

We organize all of the trending information in your field so you don't have to. Join 80,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content