This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Most startups play defense when discussing pricing with customers. They use pricing as an offensive tool to reinforce their product’s value and underscore the company’s core marketing message. For many founding teams, pricing is one of the most difficult and complex decisions for the business.

Subscribe now Amazon ReInvent This week Amazon had their annual AWS ReInvent conference. ” AWS fully embracing the breadth over depth approach. Looking at the mid to long term, we feel very optimistic about the outlook for strong AWS growth. Follow along to stay up to date! This year, there was tons of experimentation.

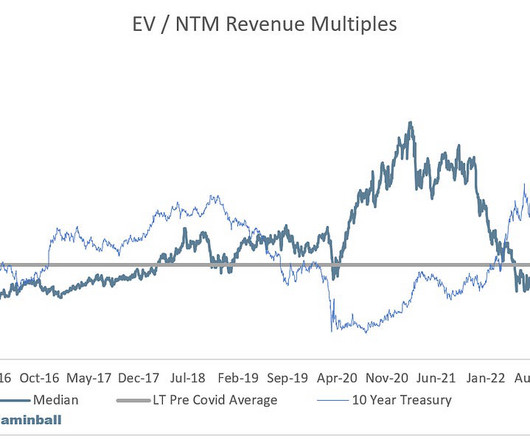

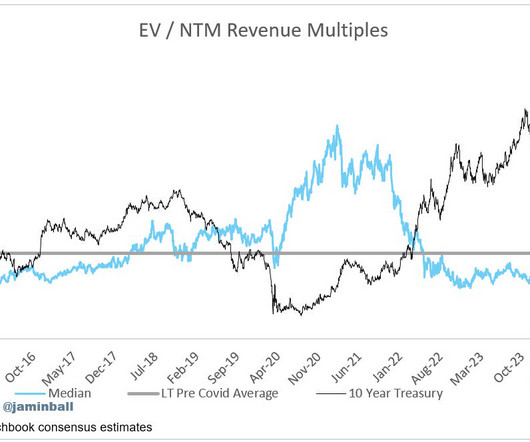

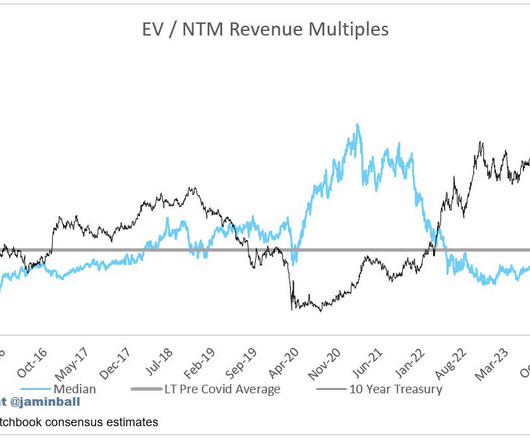

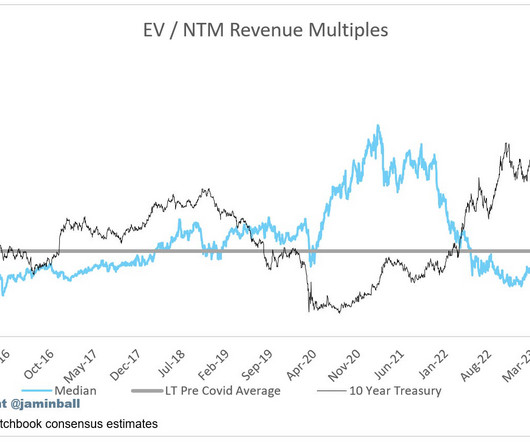

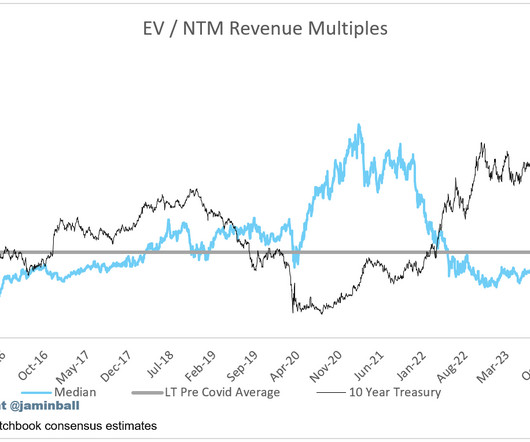

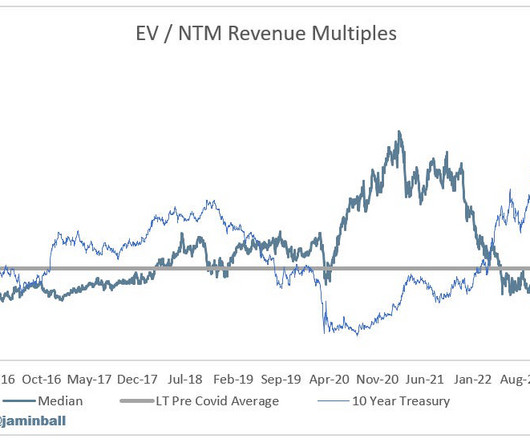

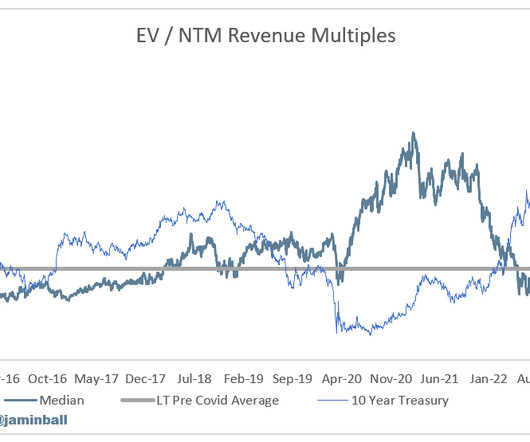

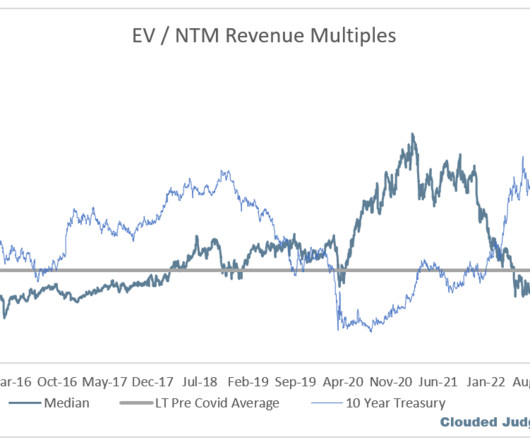

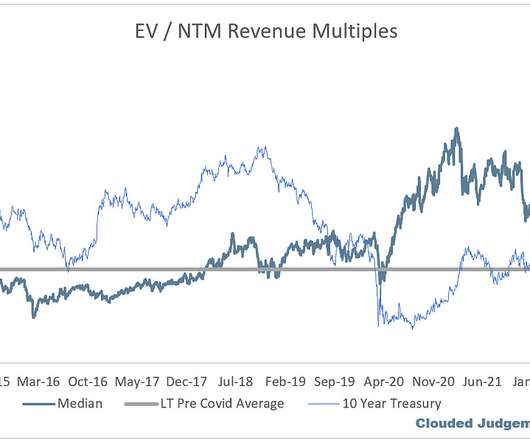

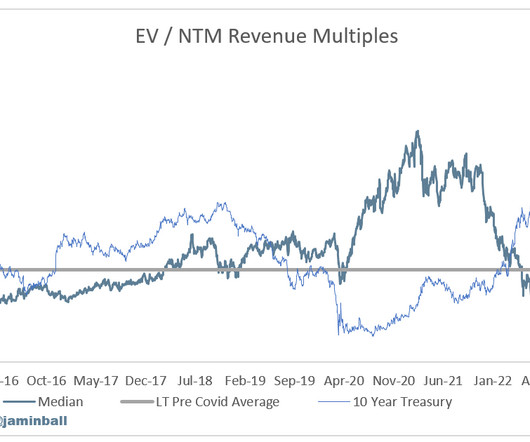

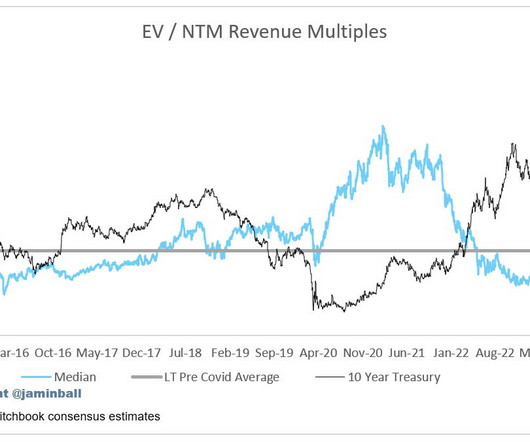

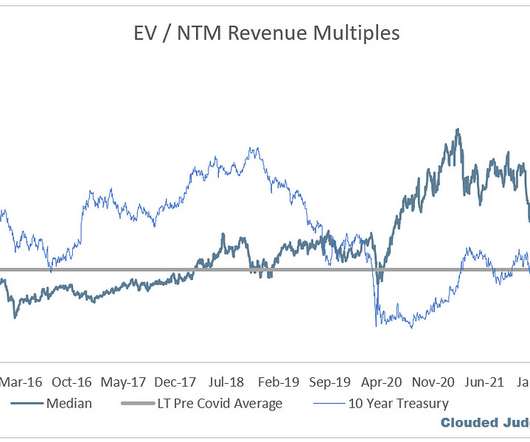

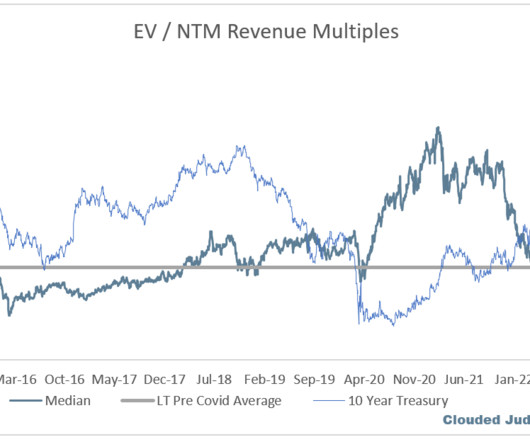

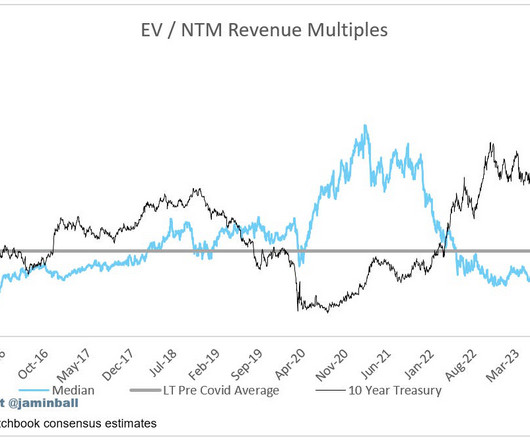

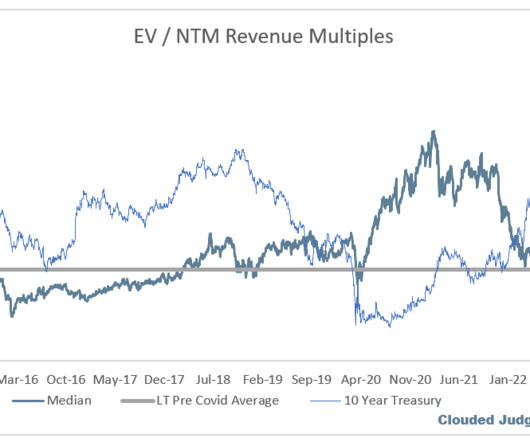

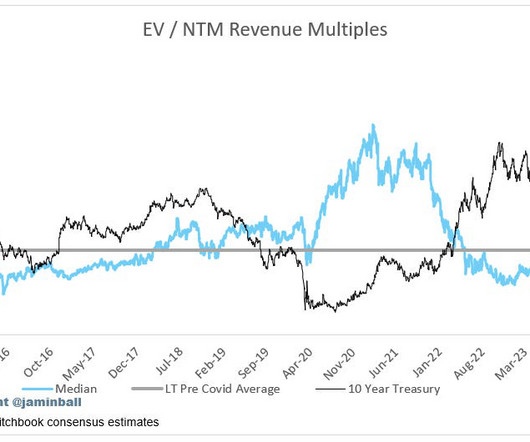

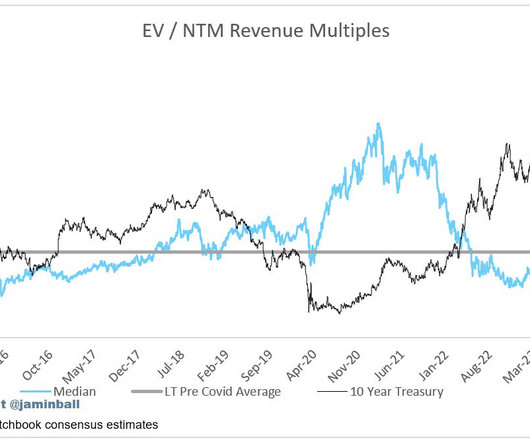

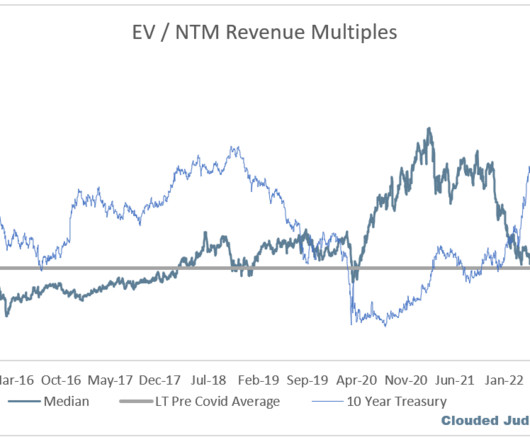

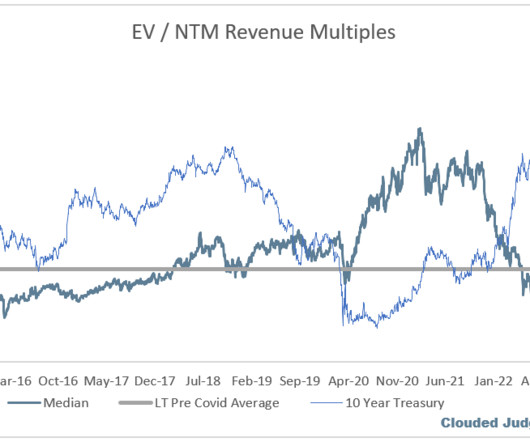

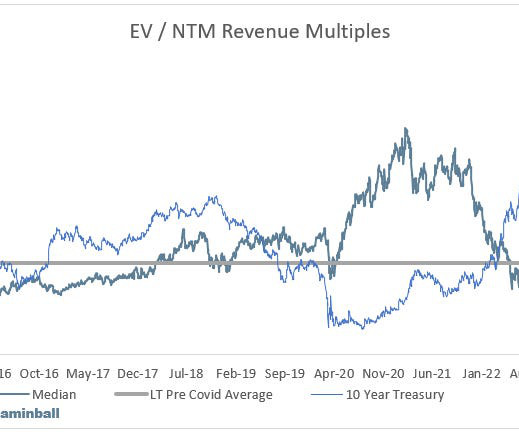

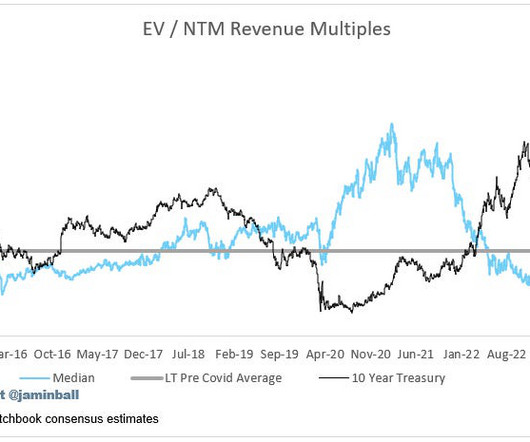

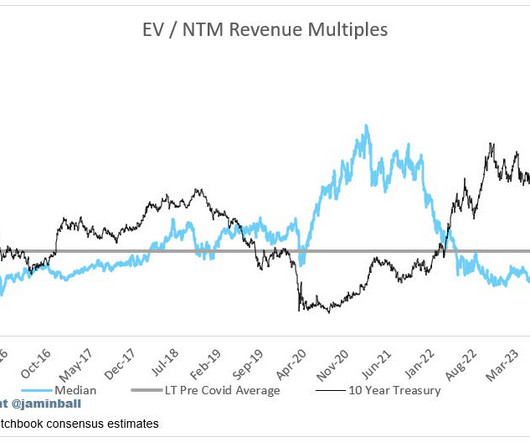

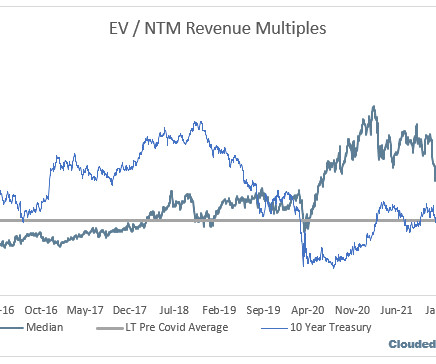

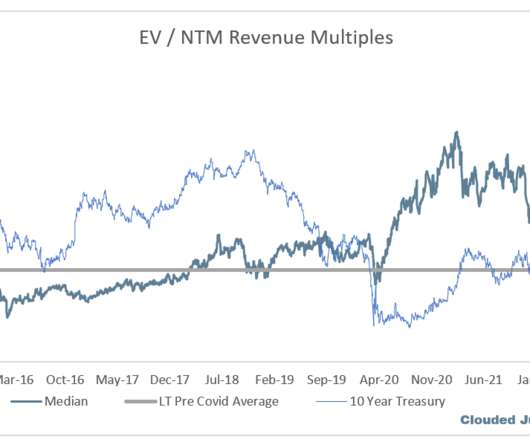

Fast forward to the launch of AWS and the public cloud. Quarterly Reports Summary Top 10 EV / NTM Revenue Multiples Top 10 Weekly Share Price Movement Update on Multiples SaaS businesses are generally valued on a multiple of their revenue - in most cases the projected revenue for the next 12 months. So why try and compete now?

ARR now really means revenue with 100%+ Net Revenue Retention. We could have picked many B2D services, like Twilio or others, too, which have primarily or substantial transaction pricing too. First, Snowflake rolls its large customers into fixed comittments (as does AWS and many others), and bills them in advance.

net retention and CAC payback). It’s worth pointing out that Azure is a bit above the long term trendline, while AWS is still below (but accelerating up). Net Revenue Retention High net revenue retention is the fourth aspect of a successful quarter, and one of my favorite metrics to evaluate in private SaaS companies.

Recently I was catching up with a good friend who used to be CEO of an enterprise-y SaaS social networking company — and the usage and engagement numbers of his business were just awful. OK, just renew at last year’s price. Well, if we do, let’s get a big price cut if usage isn’t high. Should we renew?

We all know this from AWS and Twilio on down, but Fastly is a visceral reminder. Yes, Fastly is a developer-focused platform with $100k+ price points. 130%+ revenue retention. Fastly is no exception, with 130%+ revenue retention for the past 3 years. It’s also a great one to learn from, at $200m+ ARR ($45.5m

Pothole #2 – Increasing Pricing Rate Without a Sustainable Moat. Raising prices might seem like a quick win to grow your revenue, but it’s critical to bear in mind the effect increased prices will have on your sales cycle, close rates, and disruption risk. Sell it to your market for half the price.

For software companies, this phenomenon can be a tailwind, as it drives accelerated deal closures and increased sales velocity, sometimes with less price sensitivity from buyers looking to quickly deplete their budgets. As a result, software vendors often see an uptick in revenue and bookings during these periods. Cloudflare is up 17%.

They each have some of the largest cloud businesses in the world in AWS, Azure and Google Cloud respectively. Cloud Giants Report Q4 ‘24 We now have the quarterly reports from Amazon, Microsoft and Google. Overall, there was weakness across the board. Not the best start to cloud software earnings season!

In the application layer for startups, many face challenges that boil down to retention. If you’re a startup building in this space, retention is a challenge, and you’ll need to be more strategic. Notion launched the first of many upcoming AI features, and they’ve priced it so that it may be at $100M ARR in the near term.

For example, Google and AWS are already ZoomInfo customers, but only certain sub-segments within those businesses – not the entire org. So, in 2024, there should be a more normalized customer base from a retention perspective as you transition past Q1 and those customers are transitioning with you.

And account management, which is basically around for retention and also upsell of different products. We look at annual churn, given the nature of those businesses that have annual or multi annual contracts with much bigger price items and tickets. This is where we’re putting that price, et cetera. Is actually very good.

You need 50M active free users to build a paid business, no matter the price. In B2B, you also have fixed costs, but you can diversify monetization based on tokens or seats, or in the case of AWS, however you like. It really pays to lean into retention, especially if you sell to SMBs. 25% isn’t unusual.

net retention and CAC payback). This has all resulted in the median stock price declining 5% YTD. It looks at the YoY dollar change in quarterly revenue from the hyperscalers (just looking at Azure / AWS because the data goes back further) going back a few years. Is Software Rebounding? Who are the real AI winners.

We now have results from the three hypersclaers (AWS / Azure / GCP). The most notable change in tone was Andy Jassy talking about AWS. Subscribe now Cloud Giants Report Q1 + Early Look at Software Results Q1 earnings seasons has officially kicked off! ” Full quote below: “We're seeing a few trends right now.

Subscribe now Foundation Models Are to AI what S3 was to the Public Cloud Many people look at 2006 as the birth of the public cloud - the year Amazon launched AWS. On top of that- we HAVE seen significant pricing pressure. In the last 18 months GPT4 has dropped ~90% in price! Follow along to stay up to date!

This is why we’re seeing more and more SaaS companies—Datadog, Twilio, AWS, Snowflake, and Stripe, to name a few—find success with product led growth paired with usage-based pricing. Usage-based pricing will be the key to successful monetization in the future.”. Usage-based pricing is in all layers of the tech stack.

Amazon on AWS : “…customers are continuing to shift their focus towards driving innovation and bringing new workloads to the cloud. Azure (excluding Azure AI) continued to decelerate, and while AWS did come in ahead of expectations, it wasn’t a blow out. Follow along to stay up to date!

In our webinar, 2022 SaaS retention benchmarks , SaaS Capital Manager Director Rob Belcher shares the results from their 11th annual B2B SaaS benchmarking survey. You can download the full report for net retention and gross retention benchmarks as well as retention metrics in relation to ACV, growth, size, and more.

Looking for SaaS pricing examples to get inspiration for your own strategy? In this piece, we’ll explore different pricing models and go over some brands that implemented these in real life. Hopefully, by the end of the article, you’ll have ideas on how to design a pricing strategy that contributes to product growth.

You’re leaving cash on the table for your competitors to sweep up if you don’t have a strategy for retention marketing. So, in this blog we’ll show you how to keep your customers happy with a targeted retention strategy. What is Retention Marketing? How to Measure Retention. Day 1 Retention. Week 1 Retention.

Subscribe now Cloud Giants Report Q3 ‘23 Not a great signal for software this week from the Cloud Giants (AWS, Azure and Google Cloud)…After Q2 (3 months ago), the tone from the Cloud Giants around optimizations was largely: optimizations have started to ease, and net new workloads have picked up. That is not new.”

” We saw some green shoots in AWS and a few other consumption names, and overall sentiment seemed more positive. Partly due to larger layoffs, as well as stronger bookings And finally - net retention. Not surprising, net retention continued to fall.

Hyperscalers Report Quarterly Earnings This week we saw AWS (Amazon), GCP (Google) and Azure (Microsoft) report earnings. Overall, it wasn’t pretty… AWS grew 28% when expectations were 30-31%. Every week I’ll provide updates on the latest trends in cloud software companies. Follow along to stay up to date!

Hyperscaler Preview Next week Amazon, Microsoft and Google report earnings and we’ll see Q3 data for AWS, Azure and Google Cloud. Said another way, the 10Y today is double what it averaged from 2010 to 2020. These are thought to be the early AI winners, largely due to all of the compute they’re selling to power GenAI applications.

Enterprise software businesses strive for 90-95% gross retention (generally the percent of revenue that sticks with you vs churns altogether), with net expansion in the 120%+ range (the aggregate change in expansion - contraction - churned revenue). Namely, retention!! For “fake” ARR, retention can vary wildly.

Cloud Downgrades This week UBS came out with a couple research reports citing concerns in AWS / Azure growth. This brings me back to AWS / Azure downgrades. This was the worst tone that we’ve heard in years from large AWS/Azure partners, a group that usually expresses different shades of optimism about AWS/Azure growth.”

One of the challenges with that, one of the requisites, in order to start charging money, is you have to come up with a price. At the time we had to make the pricing decision, we didn’t have the six MBAs yet. ” “Yep, we need a price.” Number one, can we sell this thing at any price? We did that.

AWS (Amazon), Azure (Microsoft), and Google Cloud (Google) all reported this week. Then AWS appeared to add fuel to that hope before giving us a huge rug pull. After all, they had a lot of AI tailwinds, and benefited tremendously from consolidation (without a headwind of a larger base of smaller startups, like AWS).

” These are two quotes about AWS on the Amazon earnings call. AWS grew 16% in Q1, but called out growth in April (first month of Q2) was 11%. We’ve all been waiting for cloud optimizations to ease up, and this is our clearest signal that we’re getting there. Revenue multiples are a shorthand valuation framework.

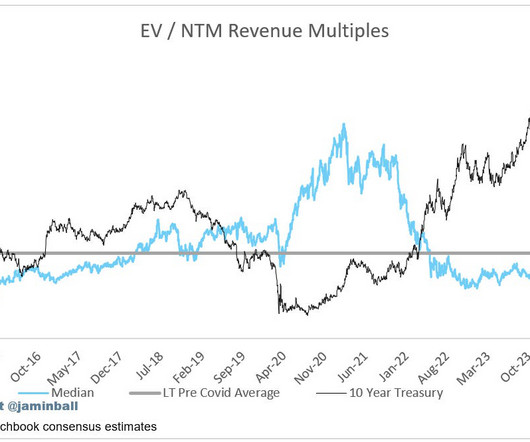

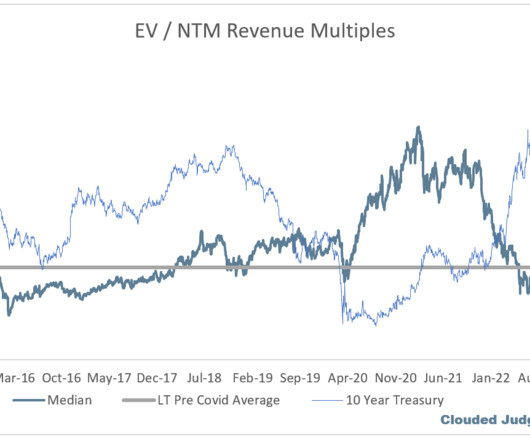

Cloud Giants Report Q2 We also got the Q2 quarters from AWS / Azure / GCP this week! Quarterly Reports Summary Top 10 EV / NTM Revenue Multiples Top 10 Weekly Share Price Movement Update on Multiples SaaS businesses are generally valued on a multiple of their revenue - in most cases the projected revenue for the next 12 months.

Next week we get all 3 hyperscalers reporting (AWS from Amazon, Azure from Microsoft, and GCP from Google). On AWS, in their Q4 earnings call they said AWS was growing “mid teens” in January (down from 20% in Q4). Every week I’ll provide updates on the latest trends in cloud software companies.

This can lead to an airpocket of valuation as companies transition to a different primary valuation metric Outside of the hypserscalers (Azure, AWS, GCP) who have uniquely benefited from AI revenue (mainly selling compute), everyone else has largely struggled. Coming in to Q1 there was broader optimism. Q4’s were generally good!

All 3 (AWS, Azure, GCP) saw positive reacceleration Quarterly Reports Summary Top 10 EV / NTM Revenue Multiples Top 10 Weekly Share Price Movement Update on Multiples SaaS businesses are generally valued on a multiple of their revenue - in most cases the projected revenue for the next 12 months.

Expansion revenue is still declining (we see this in falling net retention rates), but gross retention remains strong. This suggests that we’re at least getting closer to the bottom (but to be clear we’re still well below pre-headwind consumption levels). New customer growth seems to be picking up.

Patrick Campbell’s got thousands of SaaS companies and pricing and issues. Because sales folks want to close the biggest deal and they may not like downgrades or logo retention, how are you thinking about this issue? We can save companies $100,000 on their AWS bill. He’s going to tell you what they see.

AI = Data + Compute I’ll continue beating this drum, but we got two great quotes from Azure and AWS this week. ” Then at AWS Summit they called out “Your data is your differentiator when it comes to Generative AI.” AWS reports next week. ” Data is more important than ever! So what did we learn?

Hyperscalers (AWS, Azure, GCP as companies look for cloud GPUs who aren’t building out their own data centers) Infra (Data layer, orchestration, monitoring, ops, etc) Durable Applications We’ve clearly well underway of the first 3 layers monetizing. Model providers (OpenAI, Anthropic, etc as companies start building out AI).

” From AWS (paraphrased): They said they expect the reaccleration they saw in Q4 to continue into 2024 2024 Estimate Updates One important metric I’m tracking this quarter is the change in 2024 estimates pre / post earnings. Yes, I wouldn't say it's all back to where 2021 was, but there are some green shoots, right?

If we rewind the clock back to the cloud buildout, the competition between the 3 main players has lead to numerous price changes. I asked ChatGPT how many price changes AWS has made to S3 since it’s inception in 2006, and the answer it gave me was 65. Absent the Llama 3.1 release, would this feature have been made free?

Userpilots data is fully encrypted and stored with SOC-compliant vendors like Amazon AWS and Google Cloud. Onboard users, make announcements, and boost retention with mobile-first UI patterns. Thus, you have a single platform that addresses everything you need, from onboarding to retention.

The majority of COGS (revenue less COGS = gross profit) fall in hosting costs (ie AWS), and some customer support. The only way for software companies to avoid this gross margin compression when incorporating AI features is to raise prices. Double the price! Consumption Pricing.

There’s a real chance the fed funds rate isn’t going >5%, and a soft landing or delayed recession is certainly possible (maybe even being priced in). If the market thinks the setup for H2 is great, it won’t wait until H2 to “price it in.” But what’s happened since? Lots of deceleration in growth.

We organize all of the trending information in your field so you don't have to. Join 80,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content