This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

3 Unexpected Learnings from Datadog’s Marketing Playbook Press relations and analyst activities often contribute almost nothing to the bottom line – Datadog found that many “standard” marketing activities didn’t actually drive customer acquisition or revenue, despite their visibility.

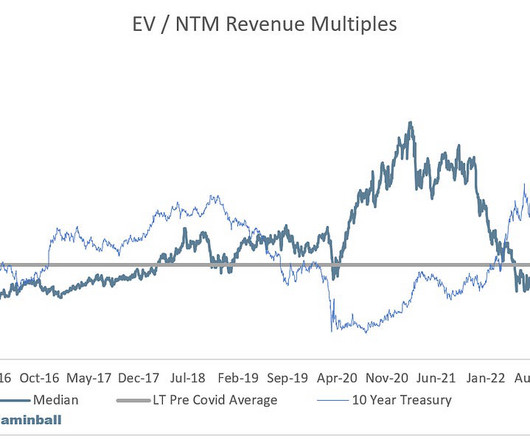

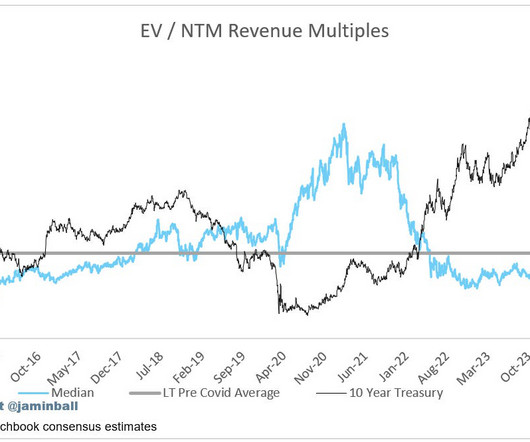

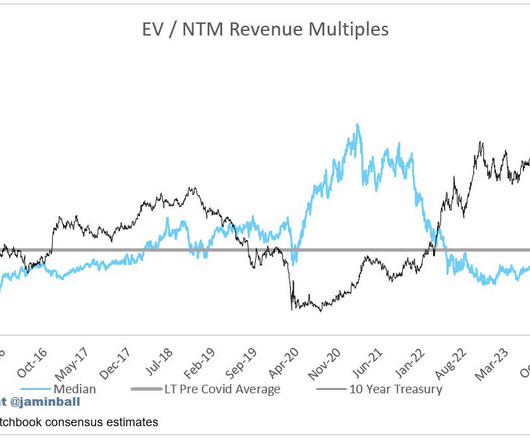

Subscribe now Amazon ReInvent This week Amazon had their annual AWS ReInvent conference. ” AWS fully embracing the breadth over depth approach. Looking at the mid to long term, we feel very optimistic about the outlook for strong AWS growth. Revenue multiples are a shorthand valuation framework. Top 5 Median: 16.6x

With Databricks now one of the largest pre-IPO technology companies, with $10 billion of expected non-dilutive financing and a valuation of $62 billion, Ron’s insights are gold for any revenue leader looking to scale. Our founders focused on adoption first, not revenue, Ron explains. The takeaway? The takeaway?

They prioritize revenue growth, market share and profit maximization differently. Maximization (Revenue Growth) - maximize revenue growth in the short term. Many mid-market software companies price with the goal of revenue maximization, negotiating for the highest possible price in each sale. AWS, Twilio, Heroku, etc.

Why Customer Success and Product Should be Best Friends: Lessons Learned with AWS’ Head of Customer Success Harini Gokul. The Builders AND Sellers Playbook: Proven Operational Models that Help Revenue & Product-led Teams Scale to $100M ARR with CircleCI’s CEO Jim Rose. And how about our product teams?

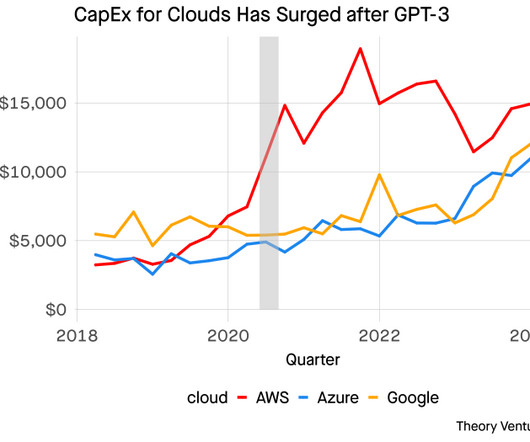

Cloud Capex in Q1 AWS $14 billion Azure $14 billion Google Cloud $12 billion These are not one-time investments, but part of a broader trend that started to occur after the introduction of GPT 3 in mid-2020 Amazon was the first to invest significantly. “Moving to AWS. Each of these businesses are large enough to justify it.

In 2006, after Amazon Web Services (AWS) helped pioneer what we now call the cloud, product development changed forever. Today, one-third of daily internet users visit websites built on top of AWS. AWS is now an $11.5B run rate business and has made up for an incredible 67% of Amazon’s operating revenue last quarter.

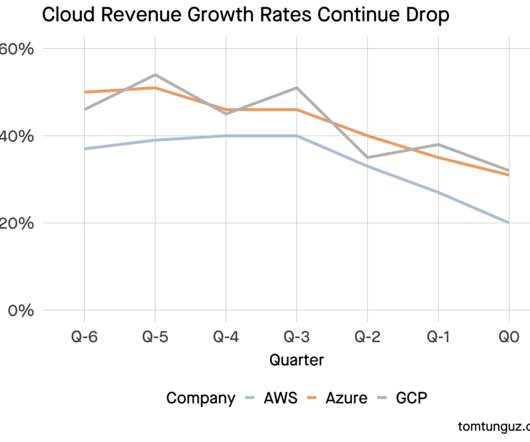

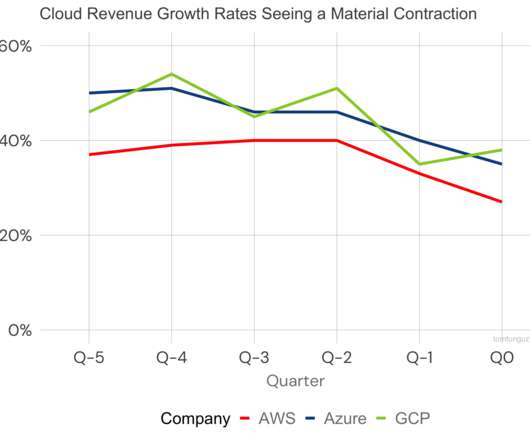

A year ago, AWS, GCP, & Azure averaged 44% annual growth. Amazon: We expect [customer] optimization efforts will continue to be a headwind to AWS growth in at least the next couple of quarters. So So far in the first month of the year, AWS year-over-year revenue growth is in the mid-teens.

So many startups these days are claiming they have “ARR” from revenue that … doesn’t recur. Doesn’t ARR stand for Annual Recurring Revenue? ARR now really means revenue with 100%+ Net Revenue Retention. 50% revenue from software (recurring), 50% from payments (not-recurring). .

Wherever the biggest dataset resided, customers ran their compute workloads that generated all of the profit and revenue growth for the last generation of data companies. AWS & others have stopped charging to move data. AWS cut prices more than 100 times in its first five years. Today, the battle is for AI gravity.

3. “Atlassian and AWS Say: Maybe Worry a Little Bit. Atlassian and AWS, two of the greats, may hold a clue: Atlassian and AWS Say: “Maybe Worry a Little Bit” 4. “A Framework For Your First SaaS Sales Comp Plan” A SaaStr Classic, still going strong in 2020. . Even If It Isn’t Revenue.”

To make this concrete - if a company got to say ~$25-50m in revenue (I’m making this number up, it’s just illustrative), someone else who is considering competing might be persuaded against it. By the time they got their competitor up and off the ground, that first mover may already be at $100m+ in revenue and at escape velocity.

So follow AWS, Azure and Google Cloud. Let’s look a whole level up to the real canaries-in-the-coalmine: AWS, Azure and Google Cloud. And AWS grew 37% at a $74B run-rate , down a bit from 39% the prior quarter but still adding an insane amount of new revenue. If they stumble, we’re in for a rough patch.

The charts below show the change in quarterly revenue YoY (so Q1 ‘24 rev - Q1 ‘23 rev) going back to 2017. It’s worth pointing out that Azure is a bit above the long term trendline, while AWS is still below (but accelerating up). Beating consensus revenue estimates is the first aspect of a successful quarter.

This drop in prices has grown AWS into a $90b revenue business in 17 years. Compare that to AWS’ managed database, Aurora, which charges $0.0000002 per request. (I’m Database Cost per Transaction in $ Cost Multiple Relative to AWSAWS Aurora 0.0000002 1 Ethereum Peak 37 185m Ethereum Today 2.67

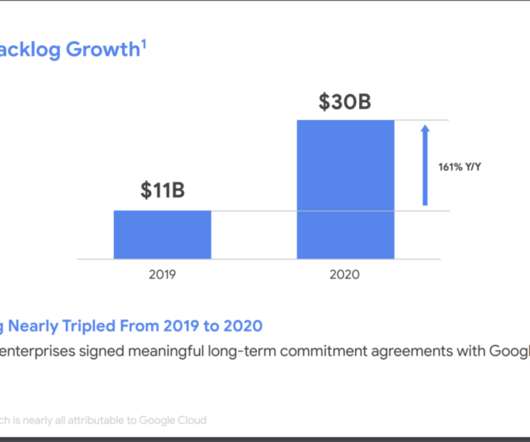

But are AWS, Azure and Google Cloud just too big for us to learn from? Google Cloud sees Cloud revenues tripling in the next 5 years. You can see that here vividly, with Google Cloud having a $30B backlog of signed revenue on top of its $13B in ARR. The power of recurring revenue and multi-year, long-term customers.

But a few thoughts on “the hardest part” for the first few stages: From $1-$100k in ARR, the hardest part is often how little revenue you get from each customer. So much work, so little revenue. Enough to pay some salaries and AWS bills, but it’s not that much. It’s just so much revenue to add in absolute terms.

AWS can’t support 20 partners equally. When partnering with big folks like Drata does with AWS, you have to bring business to them. Drata was one of three companies mentioned on stage by AWS’ Head of Partnerships because they did the most transactions on the marketplace than any other company. Otherwise, it falls apart.

Recently I was catching up with a good friend who used to be CEO of an enterprise-y SaaS social networking company — and the usage and engagement numbers of his business were just awful. It’s not like Zynga, where you see the latest XXXVille usage trail off in a few months after launch, and the revenue comes to a grinding halt.

Focusing on smaller developers, in some ways it’s been a bit overshadowed by AWS, Azure, and Google Cloud. DigitialOcean doesn’t want to take AWS, Azure and Google on in the enterprise and doesn’t really try. They are only 15% of the customers, but 83% of the revenue. Only 38% of revenue in North America.

Many have used Digital Ocean at the cheaper, simpler version of AWS-Azure-Digital Ocean to get going fast and quickly. But it’s raining cash, and earnings per share is growing 22% — faster than revenue. And if so, maybe that’s Digital Ocean. If you haven’t heard of Digital Ocean, ask your developer.

They each have some of the largest cloud businesses in the world in AWS, Azure and Google Cloud respectively. Revenue multiples are a shorthand valuation framework. Multiples shown below are calculated by taking the Enterprise Value (market cap + debt - cash) / NTM revenue. Overall, there was weakness across the board.

At the time, they were less than a billion or two in revenue, and now, they just crossed over a $30B revenue run rate. Google Cloud Platform, on the other hand, is in a very different set that also competes with Microsoft, but AWS is considered their biggest competitor in the market.

Canva: – Almost $2B ARR – Growing 40%+ – Profitable And … 4,000 employees That's about $500k in revenue per employee That's where software really makes money — Jason ✨Be Kind✨ Lemkin ?? 4,000 Employees, So About $500,000 in Revenue Per Employee That’s very efficient.

Your customers may not know that it’s your product under the hood, so while you may gain a bunch of revenue, your brand equity won’t appreciate. Marketplaces: AWS marketplace, Heroku marketplace, Salesforce marketplace. OEM relationships can be a good way to get to market quickly. But, there’s a tradeoff.

Typically support consumes about perhaps 5%-7% of your revenue at scale (excluding customer success) in most SaaS models. Another 5%-7% go to core infrastructure costs (AWS, Azure, Snowflake, etc). Dear SaaStr: What is The Average Ratio of Support Staff to Customer Count in SaaS?

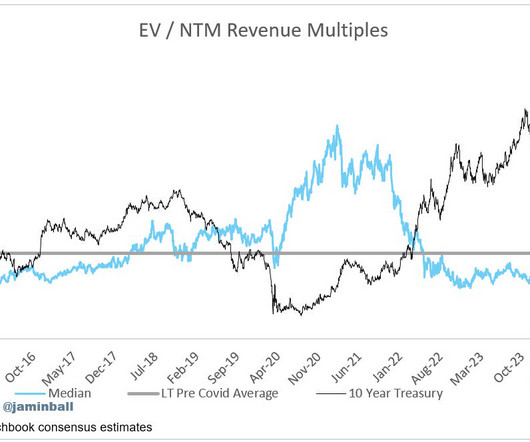

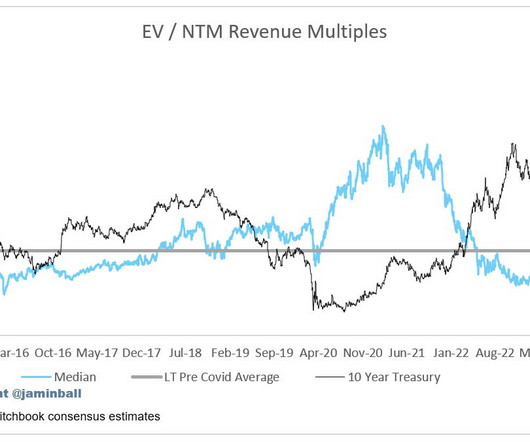

As a result, software vendors often see an uptick in revenue and bookings during these periods. Top 10 EV / NTM Revenue Multiples Top 10 Weekly Share Price Movement Update on Multiples SaaS businesses are generally valued on a multiple of their revenue - in most cases the projected revenue for the next 12 months.

Ultimately — revenue multiples. Revenue multiples are how much VCs, investors, and ultimately, an IPO and public markets will value each dollar of revenue. Revenue multiples don’t affect customers, or even revenue itself. That revenue multiples should rise from where they were in 2019.

And inflation is awful. Exceeding expectations again, and importantly, also raising guidance in revenues for the full year. #3. . — Jason 2022 SaaStr Annual Sep 13-15 Lemkin (@jasonlk) August 3, 2022. So are we in a downturn in SaaS? Certainly, segments are. eCommerce, video, and more are having post-crazy growth hangovers.

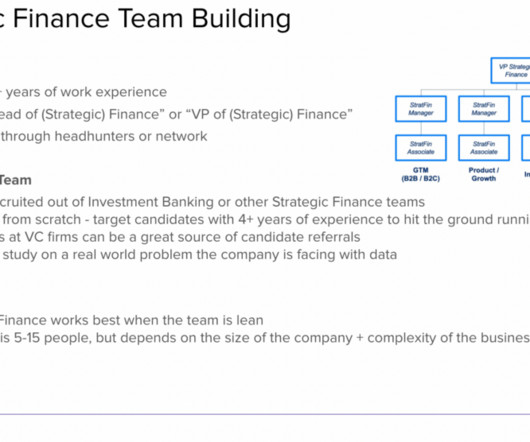

In a fascinating workshop session, Miao shares his thoughts on how finance teams can contribute to company strategy and grow revenue. Strategic Finance optimizes a company’s underlying business model to create long-term value by increasing revenue and decreasing costs. SaaStr Workshop Wednesdays are LIVE every Wednesday.

Even though you may not have that much revenue or that many leads, he will help you get more leads and maximize the experience of the leads you do have. But, sometimes a founder is >so< terrible at sales, so awful at it, that literally, it’s hopeless. Ideally, hire your Head of Demand Gen around now. But it’s super risky.

53% of Revenue is Outside U.S. With 1,500 employees, SEMRush is at about $190,000 in revenue per employee (1,500 employees). Spending a Hefty 50% of Revenue on Sales and Marketing. They spend a pretty high 50% of all revenue on sales and marketing — and that’s up from last year. And a few other interesting learnings: #6.

GAAP revenue in Q1 ’19) because it’s in a space filled with strong competitors. We all know this from AWS and Twilio on down, but Fastly is a visceral reminder. It’s an almost 100% enterprise play — they have 227 customers spending over $100k a year, comprising 84% of their revenues. The lesson?

They will manage their own servers to reduce the $3m annual AWS bill by 60%. Downtime implies a loss of revenue, which isn’t factored into the math above. Last week, David Heinemeier Hansson explained why his company, Basecamp, is leaving the cloud. Inspecting & controlling cloud costs may be the more appealing path.

Subscribe now ARR (Annual Recurring Revenue) vs ERR (Experimental Runrate Revenue) ARR (Annual Recurring Revenue) is one of the most popular SaaS (Non-GAAP) metrics. Many investors laugh (and some rightly so) at the fact that software companies’ valuations are often described as a multiple of revenue.

80% of the revenue is in the Enterprise. If you go back 10-15 years, when people ask about build vs. buy for the long-term, people would consider building their own data center if they were spending $100k/month on AWS. Today, companies spend over $10M/month on AWS — companies like Lyft, Pinterest, and Stripe. It’s not an option.

64% of Large Customers Sourced From Partners They are AWS’s largest cybersecurity partner. This chart of their revenue growth will make your jaw drop: Not much to not like here. ? Most Enterprises Buy More Than 60 Endpoint Security Products So there is room for many winners here. #8. Only Founded in 2011.

Using the Drift Conversation Cloud, businesses can personalize experiences that lead to more quality pipeline, revenue and lifelong customers. More than 5,000 customers use Drift to deliver a more enjoyable and more human buying experience that builds trust and accelerates revenue. Usually, it takes a paradigm shift to grow.

But a few thoughts on “the hardest part” for the first few stages: From $1-$100k in ARR, the hardest part is often how little revenue you get from each customer. So much work, so little revenue. Enough to pay some salaries and AWS bills, but it’s not that much. It’s just so much revenue to add in absolute terms.

Which means better customer relationships, more data, and new sources of revenue. Secureframe allows companies to get compliant within weeks, rather than months and monitors 100+ services, including AWS, GCP, and Azure. StratusGreen is a leading provider of cloud computing solutions and services for emerging and mid-sized businesses.

Here are a few: All the way until $600m+ ARR, the majority of Xero’s new bookings and revenue still came from Australia and New Zealand! Gross margins have grown to best-of-breed at 83%, after a migration to AWS and more automation in customer support. What lessons can we learn from this huge Kiwi SMB success, for other founders?

Infrastructure revenue growth averaged 33% this quarter, which is astounding considering we’re talking about businesses that sum to more than $50b of revenue per quarter. At a 7x multiple of revenue, that is another $84b of market cap creation, in theory. Let’s put these figures into context.

However, with the introduction of Events-Based Billing by Chargify, this event-based billing model is now available to small and medium-sized businesses, giving them the ability to offer the same pricing models and bill customers just as precisely as Amazon Web Services (AWS) or the popular voice and messaging platform Twilio.

Enterprise SaaS has a much higher average revenue per paying account, while consumer is around a $0.35 Churn is much higher on consumer subscriptions, but you have higher expansion revenue. If you’re in consumer, how can you go upmarket and get a small cohort of users paying more, churning less, and expanding revenue?

We organize all of the trending information in your field so you don't have to. Join 80,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content