This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

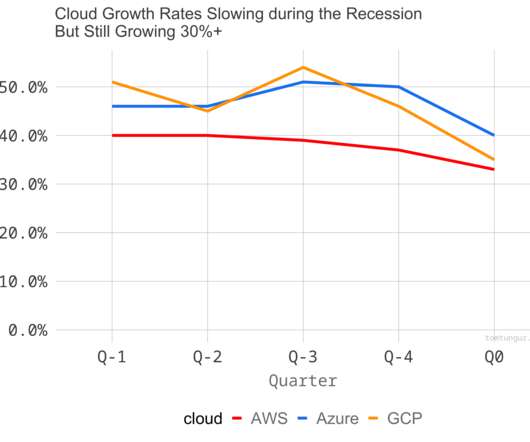

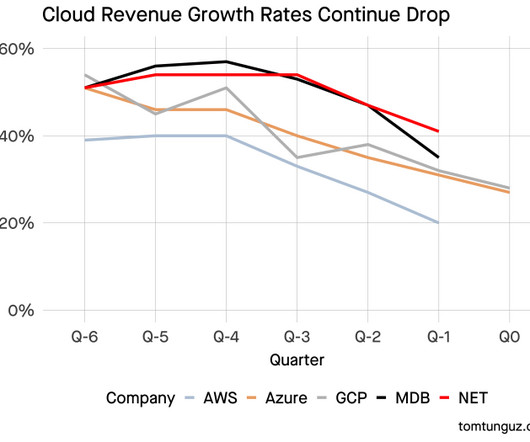

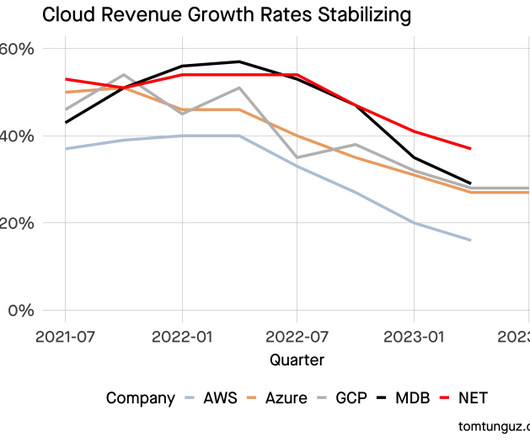

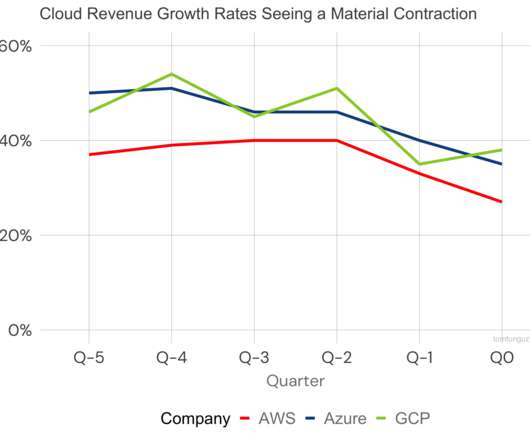

With about 39% market share, AWS reigns supreme as the largest provider. GCP reported 37% growth & Microsoft 40%. Results from these clouds suggest the market isn’t as soft as the 30% estimate - at least not yet. AWS’s growth rate is the slowest of the three largest public infrastructure clouds.

I’m watching public company earnings to identify early weaknesses in the software market. Yesterday, Google & Amazon announced earnings which completes the picture. A year ago, AWS, GCP, & Azure averaged 44% annual growth. Google: [GCP] saw slower growth of consumption as customers optimized GCP costs.

These early conversations helped shape Databricks product, pricing, and go-to-market strategy. Because thats how their customerswho were used to AWS, Azure, and GCP pricingexpected to buy. When you see product-market fit, go all in. Talk to users. We went to the open-source community and asked, What would you pay for?

I’m watching public company earnings to identify early trends in the software market to inform startups’ plans for 2023. Yesterday, Microsoft & Google announced earnings. Google Cloud Platform (GCP) & Microsoft Azure had strong quarters with about 28% annual revenue growth each.

I’m watching public company earnings to identify early weaknesses in the software market. This week Microsoft, Google/ Alphabet, & Amazon report their figures. Today, Microsoft & Google revealed the health of their infrastructure business units. Microsoft Azure. Google Cloud Platform.

It’s worth pointing out that Azure is a bit above the long term trendline, while AWS is still below (but accelerating up). It’s worth pointing out that Azure is a bit above the long term trendline, while AWS is still below (but accelerating up). What I’ve shown below is the market-adjusted stock price reaction.

Perhaps this dynamic drives consolidation in the market, paralleling the web2 infrastructure hypermarts of AWS, GCP, and Azure. Developers pay for low-latency storage with the same protocol token as they would pay for compute. Third, software engineers decentralize only a subset of the app.

As a startup, you’re doing a million things at once: building a product, answering customer tickets, developing a sales playbook, trying out different marketing hacks, and keeping the lights on. The reality is all large companies, and more and more mid-market companies, will require a SOC 2 report from their vendors. Deal: closed-lost.

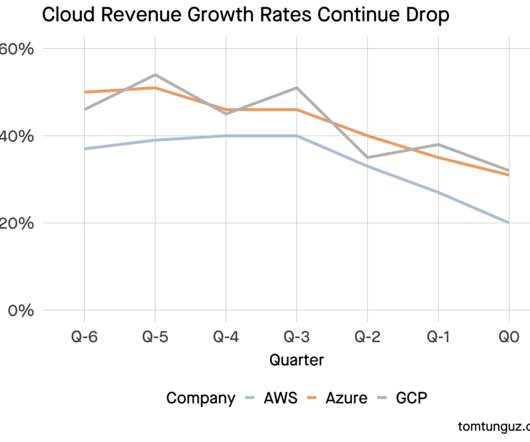

I’m watching public company earnings to identify early trends in the software market to inform startups’ plans for 2023. Yesterday, Microsoft & Google announced earnings. Both Google & Microsoft announced growth rates in GCP & Azure that held steady from one quarter to the next.

I’m watching public company earnings to identify early weaknesses in the software market. This week Microsoft, Google/ Alphabet, & Amazon reported their third quarter figures. Microsoft Azure. Google Cloud Platform. At a 7x multiple of revenue, that is another $84b of market cap creation, in theory.

Drift brings Conversational Marketing, Conversational Sales and Conversational Service into a single platform that integrates chat, email and video and powers personalized experiences with artificial intelligence (AI) at all stages of the customer journey. Usually, it takes a paradigm shift to grow. appeared first on SaaStr.

We help B2B SaaS marketers turn organic search into a source of repeatable revenue through software and coaching. DuploCloud offers an end-to-end DevOps software platform for dev teams that don’t have dedicated DevOps engineers and augments those that do.

" As with many other companies reporting strength in the market, AI & unstructured data workloads are fueling growth. “Yes, we actually saw quite a bit of energy coming from the Azureplatform this quarter. And as a result, our salespeople are really not inclined to do much in GCP.”

Layer : application, platform, or infrastructure? In the cloud, AWS, Azure, & GCP have created about as much market cap as all the top 100 B2B & B2C publics built on cloud (Netflix, ServiceNow, AirBnb, etc). Market : how to compete with incumbents?

After polling CIOs, Gartner found that total SaaS spend will grow from $100B in 2020 to $140B in 2022: A few interesting implications and learnings: The growth in SaaS buying should give you a +20% a year boost on top of your other sales and marketing efforts. That’s a huge tailwind. This is your time, folks. Go make it happen.

The hyperscalers (AWS, Azure, GCP) are always some of the first companies to report earnings during earnings season (coming up in 2 weeks), and there’s always a read through for consumption names (meaning people believe there’s a correlation). Cloudflare is up 17%. Datadog is up 14%. Mongo is up 16%. Snowflake is up 14%.

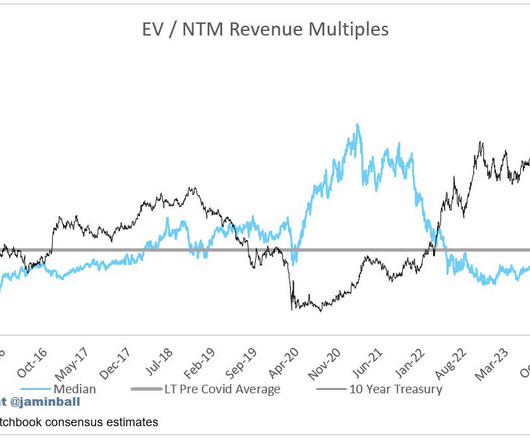

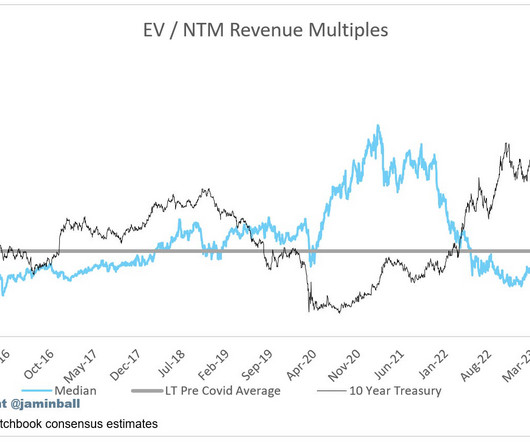

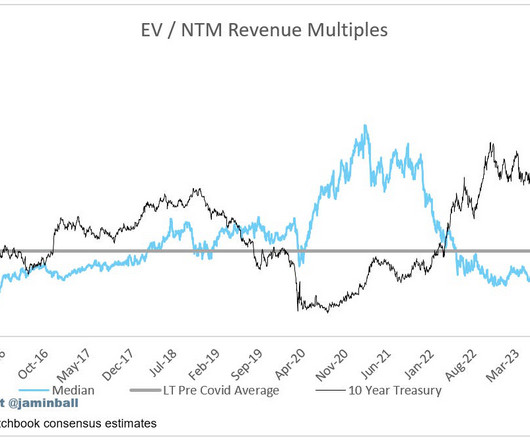

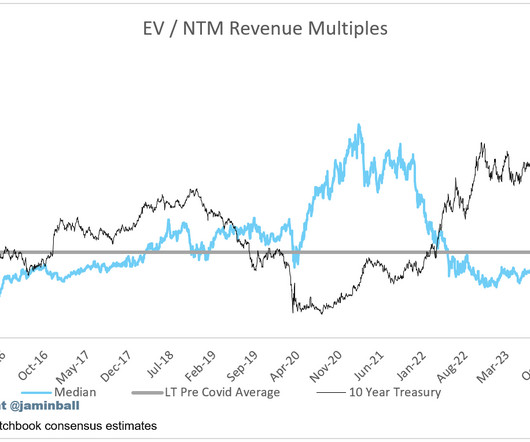

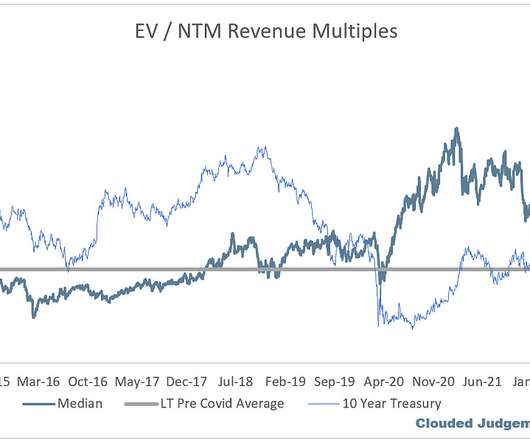

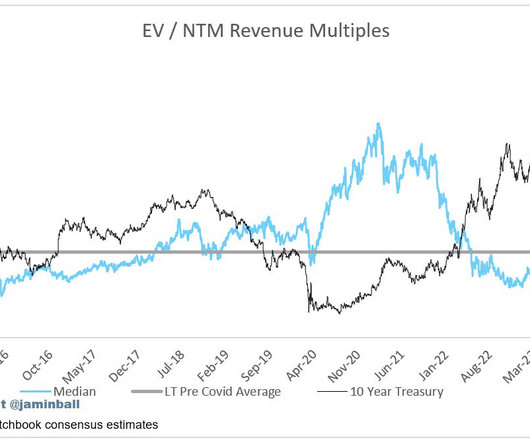

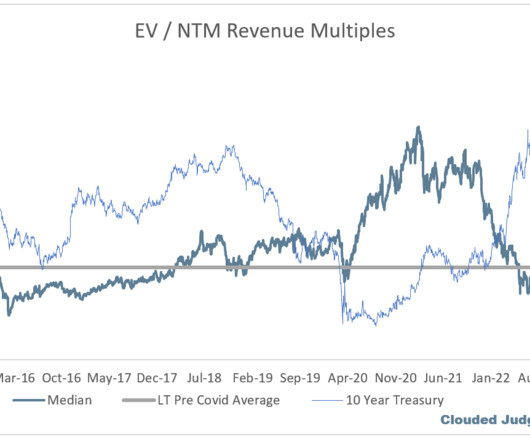

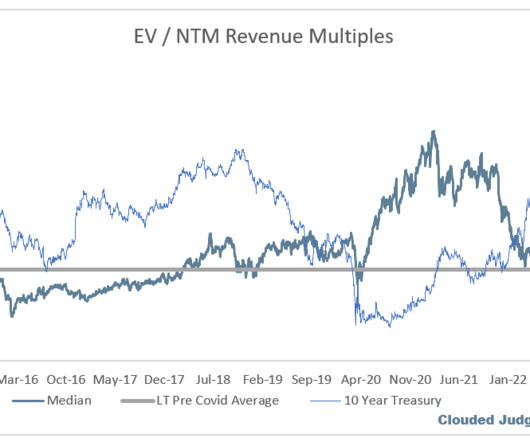

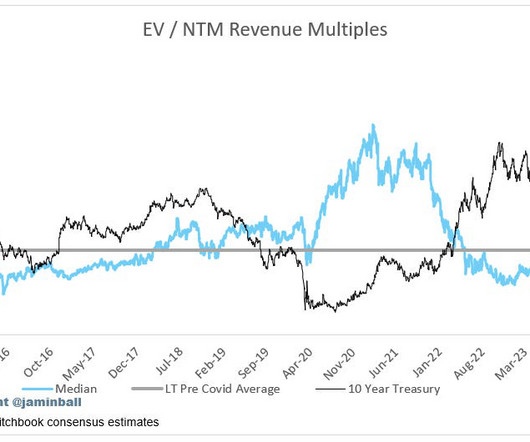

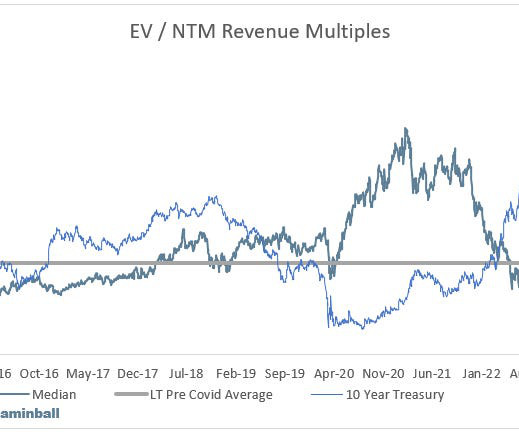

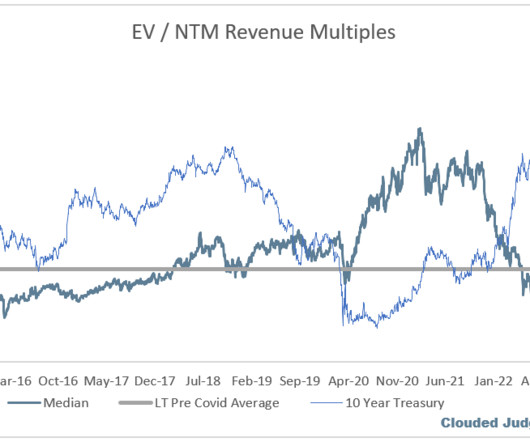

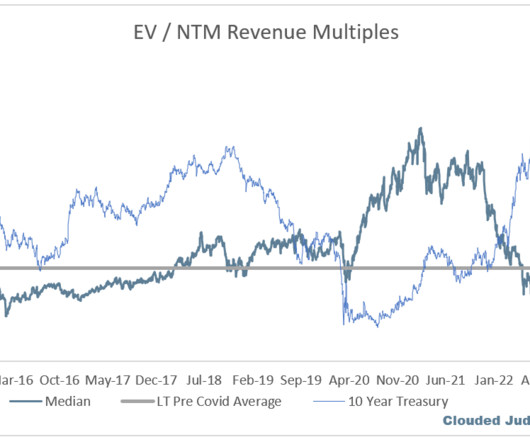

We now have results from the three hypersclaers (AWS / Azure / GCP). Multiples shown below are calculated by taking the Enterprise Value (market cap + debt - cash) / NTM revenue. Subscribe now Cloud Giants Report Q1 + Early Look at Software Results Q1 earnings seasons has officially kicked off! Top 5 Median: 17.5x

Today, the market seems a lot more worried about business fundamentals / growth. Cloud Giants Report Q2 We also got the Q2 quarters from AWS / Azure / GCP this week! Multiples shown below are calculated by taking the Enterprise Value (market cap + debt - cash) / NTM revenue. However, rates are just one variable.

Microsoft launched Azure in 2010, and Google launched GCP to the public in 2011 (they launched a preview of Google App Engine in 2008, but made it publicly available in 2011). And those price compressions will lead to significant market expansion (just like it did in the public cloud). Top 5 Median: 15.4x

Hyperscalers Report Quarterly Earnings This week we saw AWS (Amazon), GCP (Google) and Azure (Microsoft) report earnings. At the same time, Azure came in below expectations. Azure called out an incremental $800m of costs expected throughout the year (they just finished their Fiscal Q1). Top 5 Median: 15.8x

All 3 (AWS, Azure, GCP) saw positive reacceleration Quarterly Reports Summary Top 10 EV / NTM Revenue Multiples Top 10 Weekly Share Price Movement Update on Multiples SaaS businesses are generally valued on a multiple of their revenue - in most cases the projected revenue for the next 12 months. Overall Stats: Overall Median: 5.7x

You can see more detail about their net new ARR added each quarter below Azure Growth came in at 27%, and guided to 25-26% growth for Q3. That means we very well could see 27% be the bottom for them as well (assuming they beat their guidance). Then Q2 came in at 12% (must have seen improvements throughout the quarter).

Next week we get all 3 hyperscalers reporting (AWS from Amazon, Azure from Microsoft, and GCP from Google). Let’s double click on Azure. The big question I have - everyone knows the market is tough right now. Q1 Earnings Season We’re on the eve of Q1 earning season. Overall Stats: Overall Median: 5.6x

This can lead to an airpocket of valuation as companies transition to a different primary valuation metric Outside of the hypserscalers (Azure, AWS, GCP) who have uniquely benefited from AI revenue (mainly selling compute), everyone else has largely struggled. I’m as excited as ever about the long term cloud software markets.

Hyperscalers (AWS, Azure, GCP as companies look for cloud GPUs who aren’t building out their own data centers) Infra (Data layer, orchestration, monitoring, ops, etc) Durable Applications We’ve clearly well underway of the first 3 layers monetizing. Most likely Datadog is seeing trends more unique to their own business.

AI = Data + Compute I’ll continue beating this drum, but we got two great quotes from Azure and AWS this week. Satya at Microsoft said “Every AI app starts with data and having a comprehensive data and analytics platform is more important than ever.” Meaning labor markets continue to be strong!

” It’s really important that new business is still healthy, and a sign of overall market health. I think market can look forward 2-3 quarters, but we’re getting tight on that window. The hyperscalers (AWS, Azure, GCP) are seeing some uptick, but this is largely from selling compute (ie cloud GPUs).

The service is also suitable for startups, digital marketers, and even DevOps. While some website monitoring services watch apps, you really need a service that caters primarily to this market. Additionally, AppDynamics covers more complex platforms and solutions, including WebMethods, TIBCO, JMS, and queuing technologies.

Given the speed and intensity of competition in this market, it’s essential to SaaS success at any scale — and at any point on the lifecycle of your SaaS product offering. Some of these include: Create a cluster of nodes per tenant Use IAM and other platform constructs to prevent tenant boundary-crossing.

Every year Tackle surveys sellers and buyers at software companies across the spectrum—from less than $10M to over $1 billion in ARR, across multiple industries, and in roles like alliances/partnerships, sales, operations, product/development, finance, marketing, IT, and more.

Service providers like Amazon Web Services (AWS), Google Cloud Platform, and Microsoft Azure offer server hosting and load-balancing services. Service providers like Amazon Web Services (AWS), Google Cloud Platform (GCP), and Microsoft Azure offer infrastructure services that support backend development.

In contrast, a data analyst at a company developing marketing automation software might focus on analyzing campaign performance and user engagement data to optimize marketing strategies. Userpilot is an all-in-one product platform with engagement features and powerful analytics capabilities. Looking into tools for data analysts?

We researched the market and discovered many tradeoffs and advantages a new provider could bring to the table. Our options were Amazon Web Services (AWS), Google Cloud (GCP), and Azure. Managed Kubernetes was another major factor to consider, and this was head to head with Google Cloud (GCP).

This helps personalize the user experience and target marketing efforts effectively. They collaborate with product managers, marketing teams, and other stakeholders to translate their analytical findings into actionable business strategies. Bonus points : Experience with cloud platforms (AWS, Azure, GCP).

I did not unleash our sales force and go to a market of 3000 people to sell the thing we bought because we just can’t satisfy the demand. It will be like AWS, GCP, and Azure. At Databricks, we bought Mosaic. There are not enough GPUs. Ben: So you won’t even let all your guys sell it?

Examples of IaaS Cloud Providers Amazon Web Services (AWS) Google Cloud Provider (GCP) IBM Cloud Microsoft Azure PaaS Taking a step ahead from IaaS, let us introduce you to PaaS or Platform-as-a-support. No matter the size of the business, SaaS services can help anyone with advanced and effective solutions.

marketing, product) to define key business questions and translate them into data-driven problems. Bonus points : Experience with cloud platforms (AWS, Azure, GCP). This helps personalize the user experience and target marketing efforts effectively. Experience with data visualization tools (e.g.,

This week on the Sales Hacker podcast, we talk to Alison Wagonfeld, CMO of Google Cloud. Alison brings a wealth of marketing, investor, and exec experience to the show. Google’sMarketing Message and stance on competitors. About Alison Wagonfeld and Google Cloud (01:52). About Alison Wagonfeld and Google Cloud.

We organize all of the trending information in your field so you don't have to. Join 80,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content