This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Through these interactions, I’ve built up mental benchmarks for metrics on which I place extra emphasis. My hope is that this analysis can provide startup entrepreneurs with a framework for how to manage their businesses around SaaS metrics (e.g., This metric is more self-explanatory, so I won’t go into detail.

The hyperscalers (AWS, Azure, GCP) are always some of the first companies to report earnings during earnings season (coming up in 2 weeks), and there’s always a read through for consumption names (meaning people believe there’s a correlation). I created this subset to show companies where FCF is a relevant valuation metric.

We now have results from the three hypersclaers (AWS / Azure / GCP). Given most software companies are not profitable, or not generating meaningful FCF, it’s the only metric to compare the entire industry against. I created this subset to show companies where FCF is a relevant valuation metric.

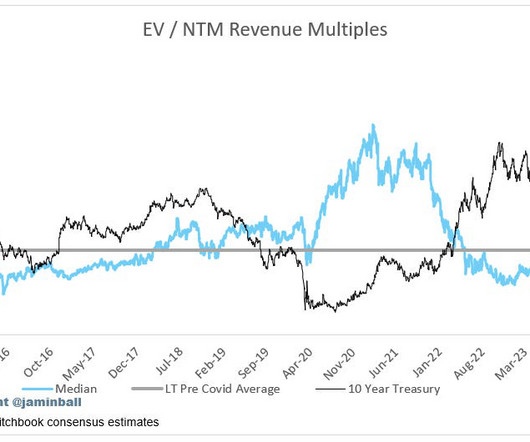

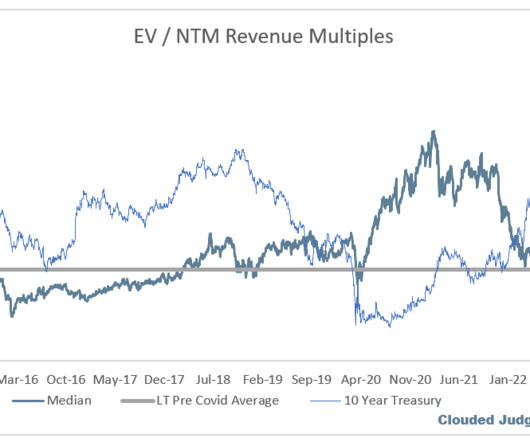

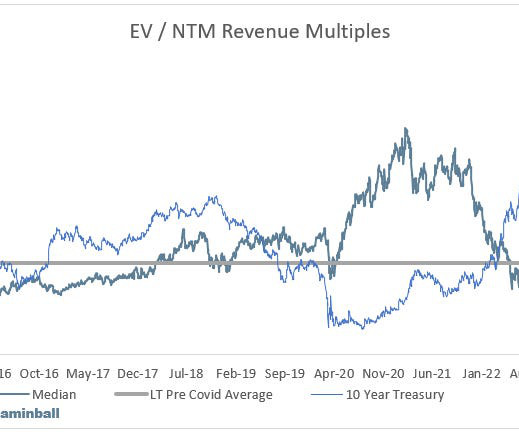

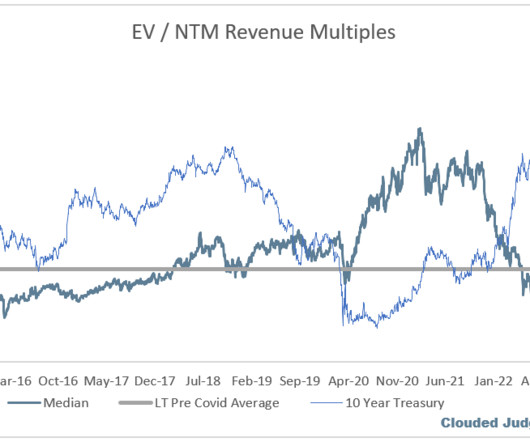

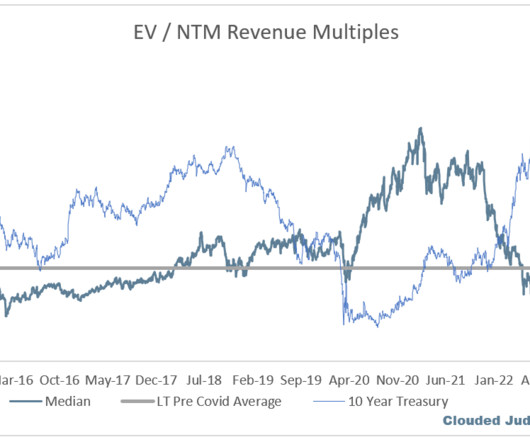

Microsoft launched Azure in 2010, and Google launched GCP to the public in 2011 (they launched a preview of Google App Engine in 2008, but made it publicly available in 2011). I created this subset to show companies where FCF is a relevant valuation metric. Revenue multiples are a shorthand valuation framework.

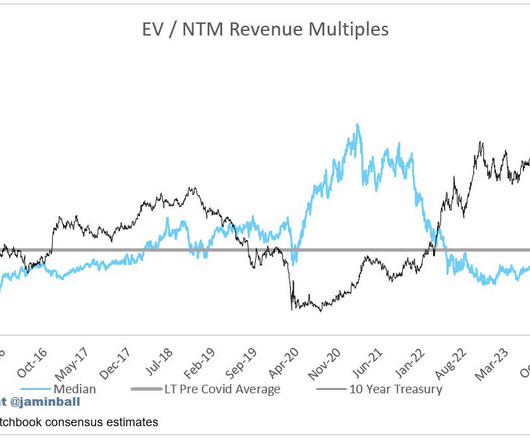

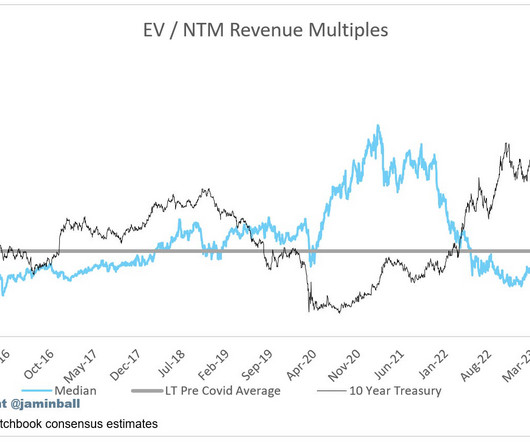

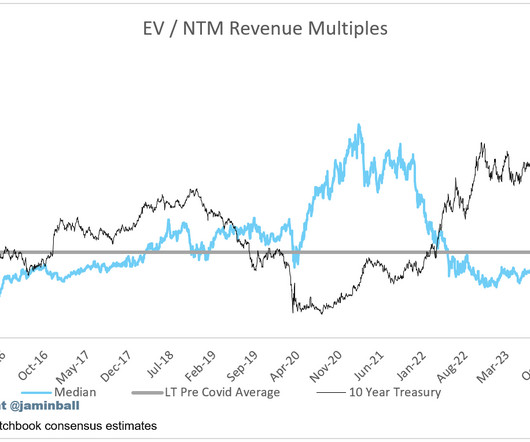

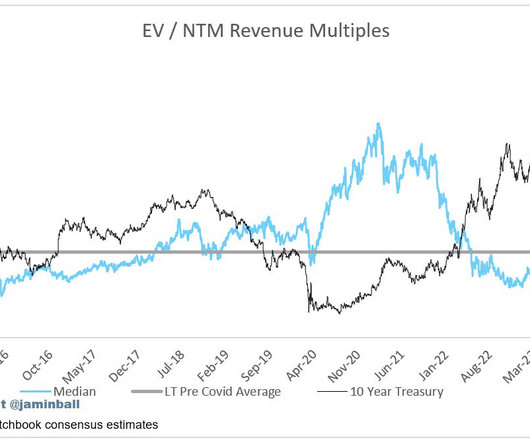

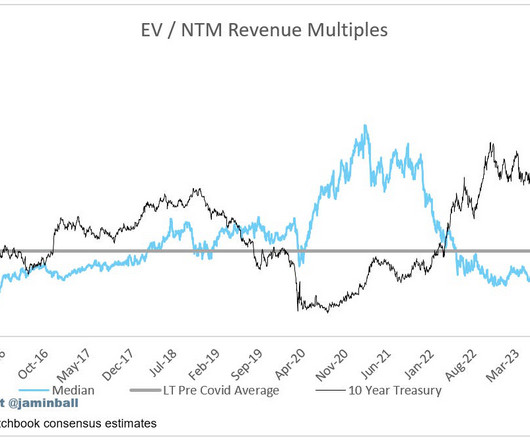

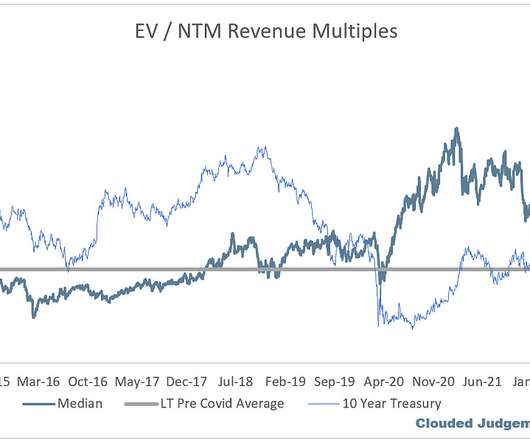

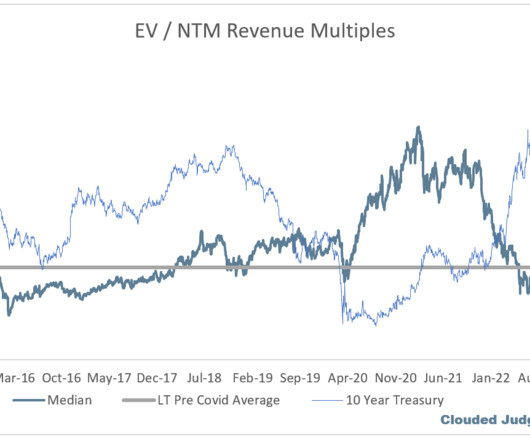

All 3 (AWS, Azure, GCP) saw positive reacceleration Quarterly Reports Summary Top 10 EV / NTM Revenue Multiples Top 10 Weekly Share Price Movement Update on Multiples SaaS businesses are generally valued on a multiple of their revenue - in most cases the projected revenue for the next 12 months.

Cloud Giants Report Q2 We also got the Q2 quarters from AWS / Azure / GCP this week! Given most software companies are not profitable, or not generating meaningful FCF, it’s the only metric to compare the entire industry against. I created this subset to show companies where FCF is a relevant valuation metric.

Hyperscalers Report Quarterly Earnings This week we saw AWS (Amazon), GCP (Google) and Azure (Microsoft) report earnings. At the same time, Azure came in below expectations. Azure called out an incremental $800m of costs expected throughout the year (they just finished their Fiscal Q1).

You can see more detail about their net new ARR added each quarter below Azure Growth came in at 27%, and guided to 25-26% growth for Q3. That means we very well could see 27% be the bottom for them as well (assuming they beat their guidance). Then Q2 came in at 12% (must have seen improvements throughout the quarter).

.” As growth starts to slow, it gets harder and harder to justify using revenue multiples as a primary valuation metric. And when this happens, growth companies transition to more of a value based valuation metric (FCF or PE). I created this subset to show companies where FCF is a relevant valuation metric.

Next week we get all 3 hyperscalers reporting (AWS from Amazon, Azure from Microsoft, and GCP from Google). Let’s double click on Azure. Given most software companies are not profitable, or not generating meaningful FCF, it’s the only metric to compare the entire industry against.

Hyperscalers (AWS, Azure, GCP as companies look for cloud GPUs who aren’t building out their own data centers) Infra (Data layer, orchestration, monitoring, ops, etc) Durable Applications We’ve clearly well underway of the first 3 layers monetizing. Revenue multiples are a shorthand valuation framework.

AI = Data + Compute I’ll continue beating this drum, but we got two great quotes from Azure and AWS this week. Satya at Microsoft said “Every AI app starts with data and having a comprehensive data and analytics platform is more important than ever.” ” Data is more important than ever! AWS reports next week.

If next quarter we get similar commentary that Azure gave us this quarter (“still a couple quarters away” without any specific guidance), then we may see market loose a little patience. The hyperscalers (AWS, Azure, GCP) are seeing some uptick, but this is largely from selling compute (ie cloud GPUs).

Consider also that the Google algorithm ranks websites by load speed, among other metrics. From here, the script collects data from users across various performance metrics and reports back to the RUM interface. Site24x7 supports Ruby, Java, PHP,NET, Node.js, and mobile platforms for apps.

Typical data lake storage solutions include AWS S3, Azure Data Lake Storage (ADLS), Google Cloud Storage (GCS) or Hadoop Distributed File System (HDFS). The warehouse is then optimized for efficient access (typically through SQL) to that data, with a number of other properties layered in (like governance, access, security, etc).

Service providers like Amazon Web Services (AWS), Google Cloud Platform, and Microsoft Azure offer server hosting and load-balancing services. Service providers like Amazon Web Services (AWS), Google Cloud Platform (GCP), and Microsoft Azure offer infrastructure services that support backend development.

Another essential benefit of identity in a tenant context is that it aids in capturing and analyzing events from logs & metrics. Some of these include: Create a cluster of nodes per tenant Use IAM and other platform constructs to prevent tenant boundary-crossing. Amazon Cognito) can be used for access authorization.

We researched the market and discovered many tradeoffs and advantages a new provider could bring to the table. Our options were Amazon Web Services (AWS), Google Cloud (GCP), and Azure. Managed Kubernetes was another major factor to consider, and this was head to head with Google Cloud (GCP). Team expertise.

Bonus points : Experience with cloud platforms (AWS, Azure, GCP). It provides features like metrics dashboards , reports (funnel, path, trend, cohort), user feedback , etc. Experience with data visualization tools (e.g., Tableau, Power BI). Excellent communication and collaboration skills.

GCP 23 35 52.2% Azure 26 33 26.9% Cloud Operating Margin Azure 44% AWS 38% GCP 17% Plus the operating margins of these companies is massive at around 40% for the top two. Cloud Operating Margin Azure 44% AWS 38% GCP 17% Plus the operating margins of these companies is massive at around 40% for the top two.

We organize all of the trending information in your field so you don't have to. Join 80,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content