This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Subscribe now Azure Report - Cloud Infra Looks Good! For software, all eyes were on Azure - which grew 31% YoY (ahead of expectations closer to 29%). Azure doesn’t disclose exact Azure quarterly revenue (they disclose growth rate in absolute terms and in constant currency), but there are good estimations.

One invoice. I would pay each product provider in their own token: one for storage, compute, caching/CDN, email subscription management, etc. Perhaps this dynamic drives consolidation in the market, paralleling the web2 infrastructure hypermarts of AWS, GCP, and Azure. I paid for them each in US dollars every month.

It’s worth pointing out that Azure is a bit above the long term trendline, while AWS is still below (but accelerating up). It’s worth pointing out that Azure is a bit above the long term trendline, while AWS is still below (but accelerating up). Some software companies also have seasonality in the “payback.”

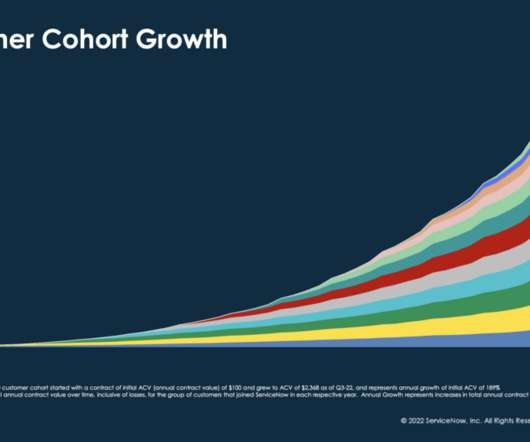

Ok, this chart is a bit confusing, but if you look at ServiceNow’s currency-adjusted revenue, you can see super-consistent 29%-30% growth in subscription revenue each of the past 5 quarters. #2. Microsoft also reported strong growth overall and for Azure and Cloud especially. Steady, steady, steady strong growth. But ServiceNow?

ChartMogul is an analytics platform to help you run your subscription business. Our mission is to build powerful and secure cloud software for subscription businesses of all sizes, with a strong emphasis on good design and ease of use.

ChartMogul is an analytics platform to help you run your subscription business. Our mission is to build powerful and secure cloud software for subscription businesses of all sizes, with a strong emphasis on good design and ease of use.

The most triumphant transfer of control from an original generation leader to a new CEO was surely that of Microsoft, which pivoted from chasing after Apple’s success in the consumer space under Steve Ballmer (don’t mention Nokia ) to successfully focusing on the cloud under Satya Nadella (please do mention Azure).

2: LinkedIn is Migrating to Microsoft Azure. 3: Microsoft Invests $1 BIllion in OpenAI to Develop AI Technologies on Azure. 6: “Tinder In-App Purchases No Longer Use Google Play Billing” Mobile subscriptions are becoming a big deal, although it’s early overall. And ask them if it could happen to you.

Subscribe now Cloud Giants Report Q3 ‘23 Not a great signal for software this week from the Cloud Giants (AWS, Azure and Google Cloud)…After Q2 (3 months ago), the tone from the Cloud Giants around optimizations was largely: optimizations have started to ease, and net new workloads have picked up. Staggering scale already.

We now have results from the three hypersclaers (AWS / Azure / GCP). Most public companies don’t report net new ARR, so I’m taking an implied ARR metric (quarterly subscription revenue x 4). Companies that do not disclose subscription rev have been left out of the analysis and are listed as NA.

” Microsoft on Azure : “And I think last quarter, we said one, we are going to continue to have these cycles where people will build new workloads. Azure (excluding Azure AI) continued to decelerate, and while AWS did come in ahead of expectations, it wasn’t a blow out.

It looks at the YoY dollar change in quarterly revenue from the hyperscalers (just looking at Azure / AWS because the data goes back further) going back a few years. If we break this down and look at Azure and AWS independently (graphs below), you’ll see how the AWS “swings” were a lot more volatile.

Azure’s marketplace has over 4 million monthly visitors. million subscriptions transacted and Google’s marketplace has seen 3X growth in SaaS sales. And a lot of this depends on your go to market, but we are selling jointly with the AWS and the Azure, et cetera sellers too. AWS’s marketplace has seen 1.5

Hyperscaler Preview Next week Amazon, Microsoft and Google report earnings and we’ll see Q3 data for AWS, Azure and Google Cloud. Most public companies don’t report net new ARR, so I’m taking an implied ARR metric (quarterly subscription revenue x 4).

Cloud Downgrades This week UBS came out with a couple research reports citing concerns in AWS / Azure growth. This brings me back to AWS / Azure downgrades. This was the worst tone that we’ve heard in years from large AWS/Azure partners, a group that usually expresses different shades of optimism about AWS/Azure growth.”

AWS (Amazon), Azure (Microsoft), and Google Cloud (Google) all reported this week. Azure reported on Tuesday and gave us that glimmer of hope. Azure : Coming into the quarter, a growth rate that would have satisfied the market would have been ~29%. Azure came in at 31% (constant currency). Follow along to stay up to date!

Hyperscalers Report Quarterly Earnings This week we saw AWS (Amazon), GCP (Google) and Azure (Microsoft) report earnings. At the same time, Azure came in below expectations. Azure called out an incremental $800m of costs expected throughout the year (they just finished their Fiscal Q1).

MetricFire offers five subscription tiers according to the needs of different organization types. Stripe is the leading payment processing service for SaaS and subscription businesses. MetricFire is one of 900+ subscription-based companies using Baremetrics to understand key metrics and accelerate growth.

Azure (Microsoft) Quarter The week the first of the cloud giants reported - Azure. Early Look at 2023 Guides Given the Azure weakness reported on Tuesday, all software tumbled Wednesday morning with most names down 5-10%. Companies that do not disclose subscription rev have been left out of the analysis and are listed as NA.

Cloud Giants Report Q2 We also got the Q2 quarters from AWS / Azure / GCP this week! Most public companies don’t report net new ARR, so I’m taking an implied ARR metric (quarterly subscription revenue x 4). Companies that do not disclose subscription rev have been left out of the analysis and are listed as NA.

You can see more detail about their net new ARR added each quarter below Azure Growth came in at 27%, and guided to 25-26% growth for Q3. Most public companies don’t report net new ARR, so I’m taking an implied ARR metric (quarterly subscription revenue x 4).

Microsoft launched Azure in 2010, and Google launched GCP to the public in 2011 (they launched a preview of Google App Engine in 2008, but made it publicly available in 2011). Most public companies don’t report net new ARR, so I’m taking an implied ARR metric (quarterly subscription revenue x 4).

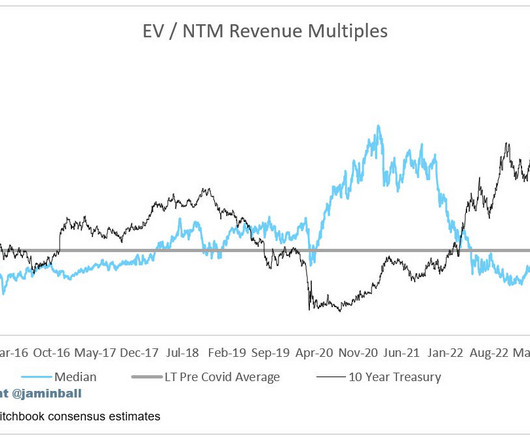

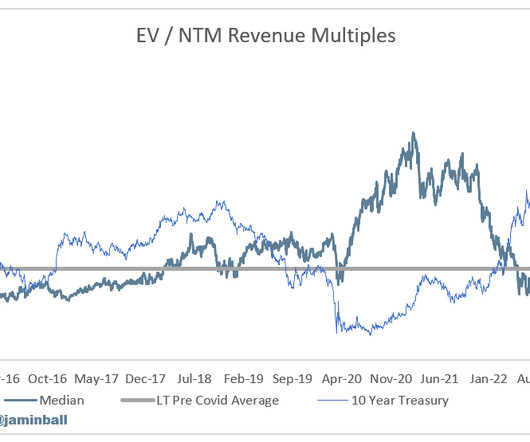

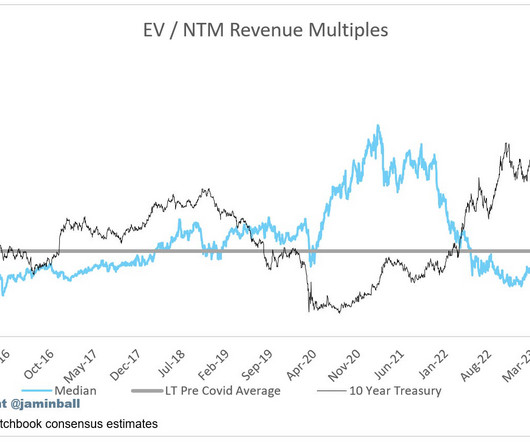

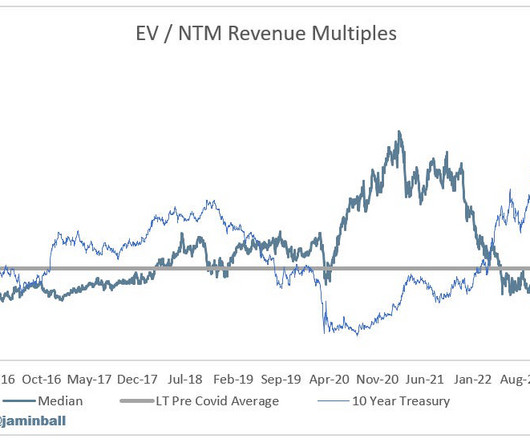

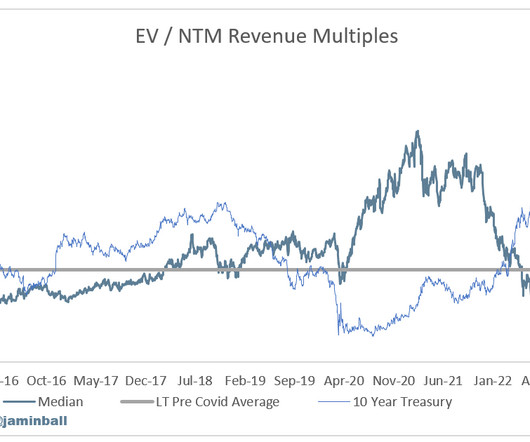

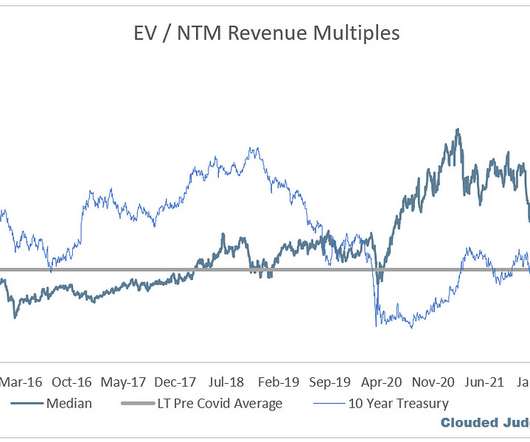

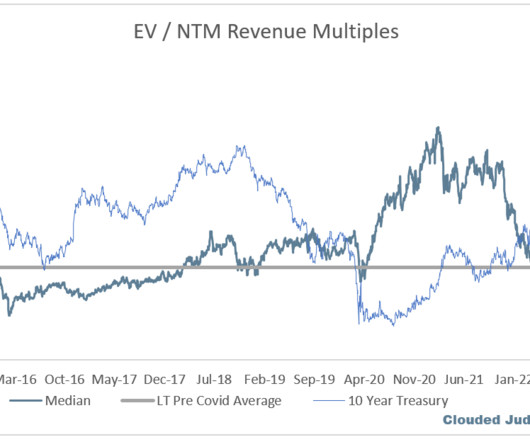

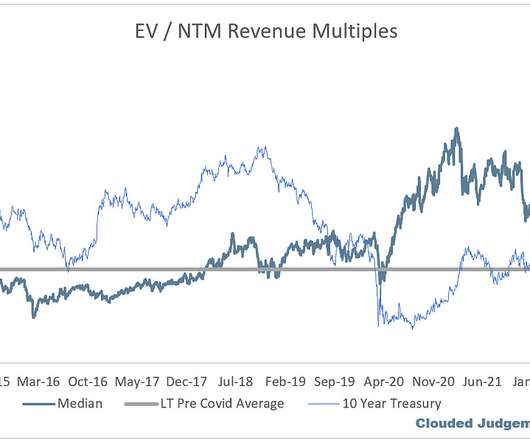

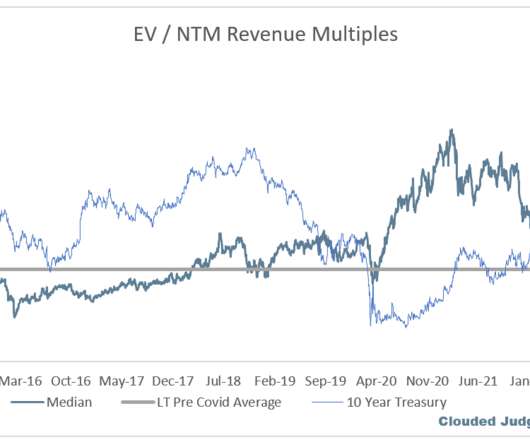

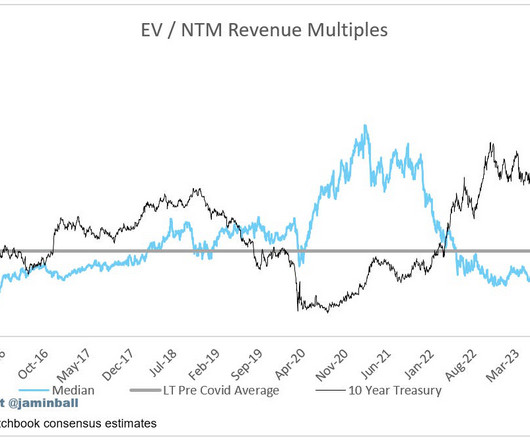

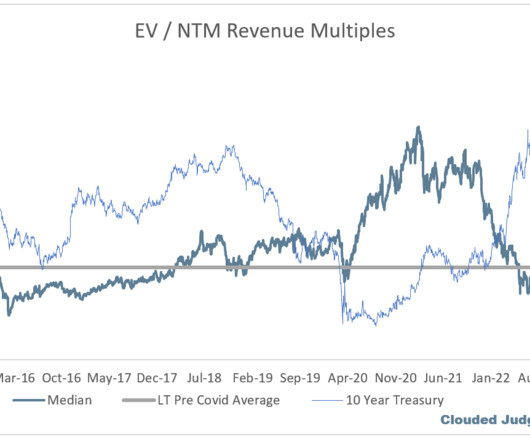

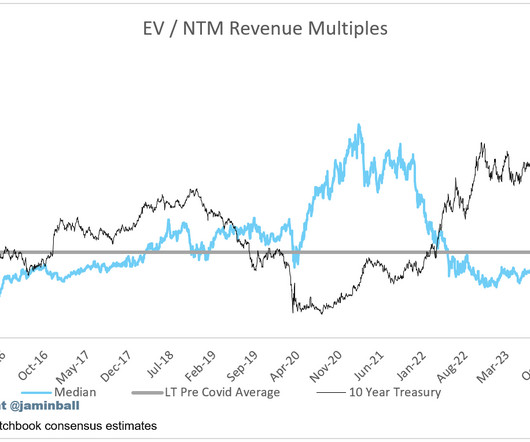

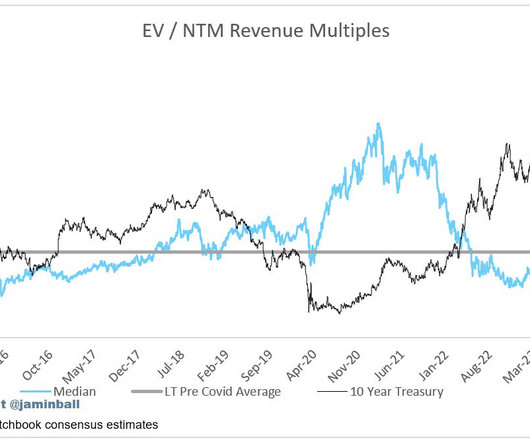

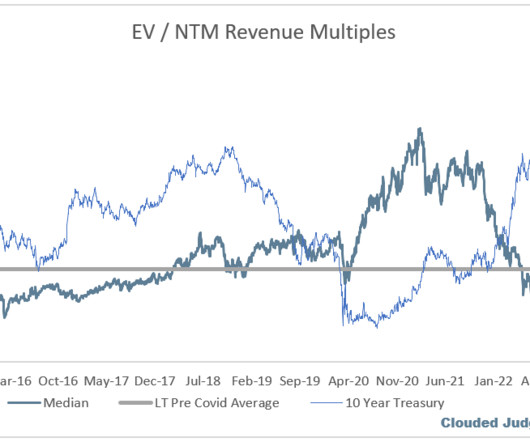

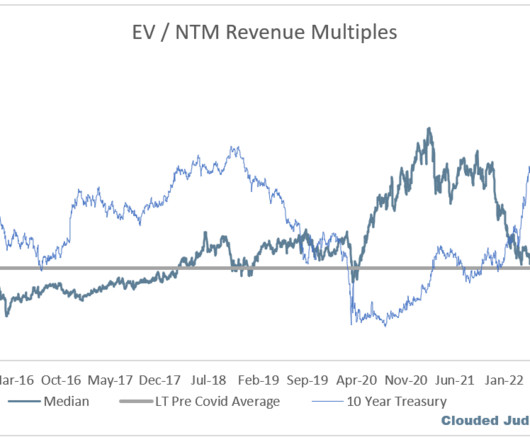

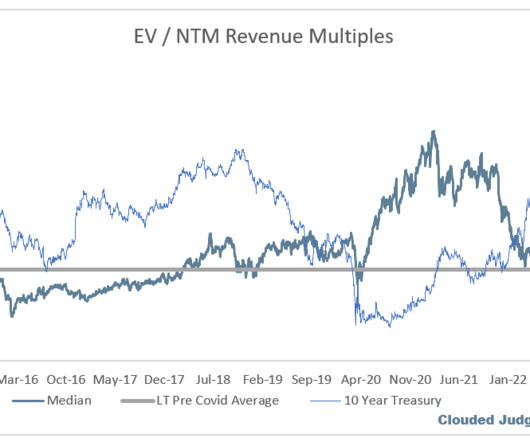

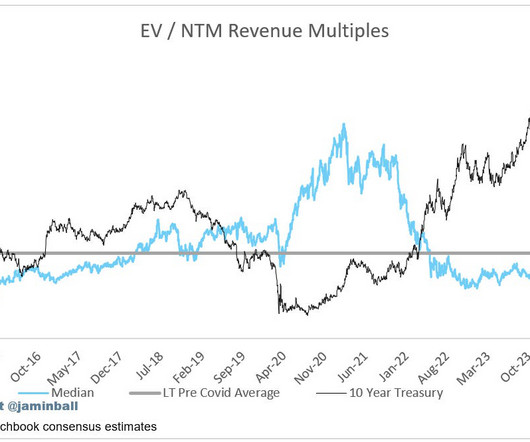

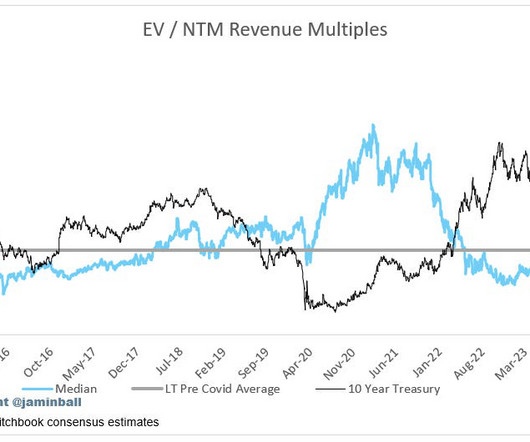

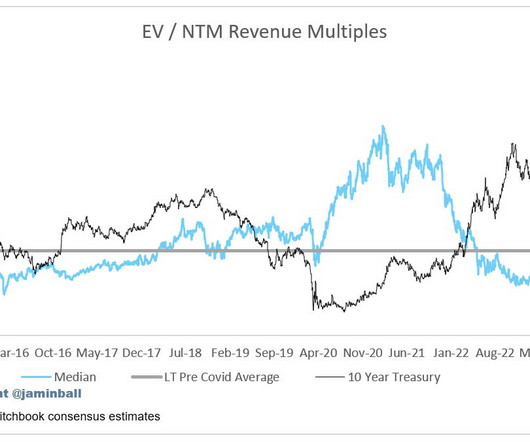

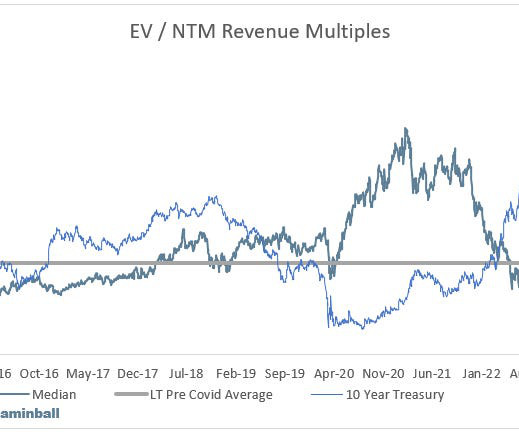

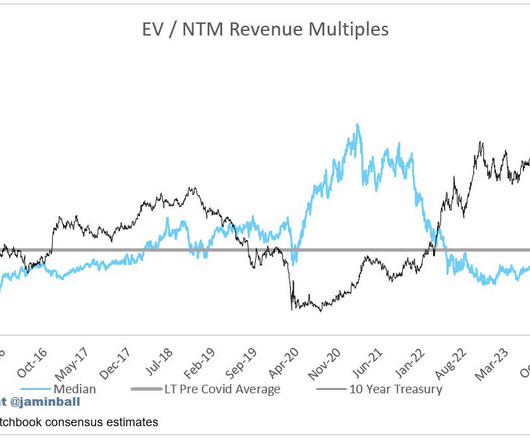

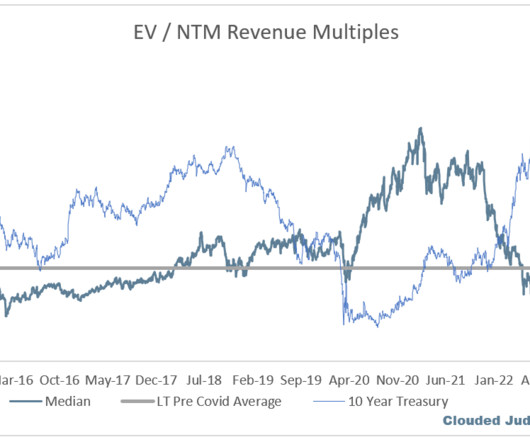

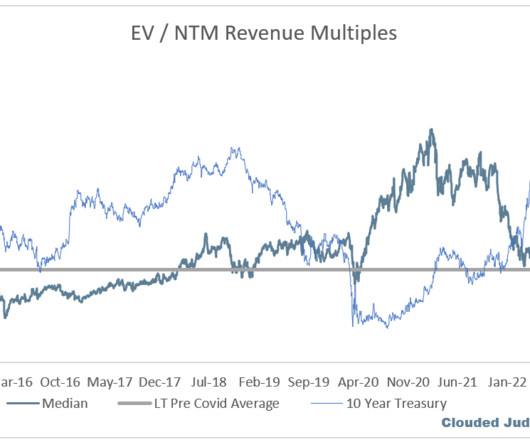

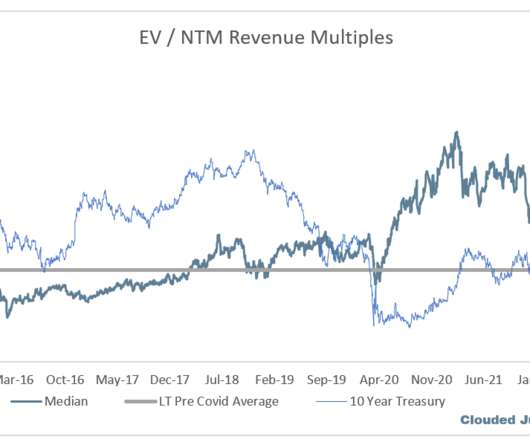

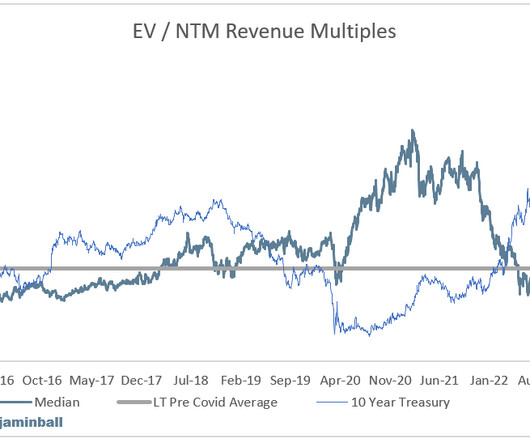

All 3 (AWS, Azure, GCP) saw positive reacceleration Quarterly Reports Summary Top 10 EV / NTM Revenue Multiples Top 10 Weekly Share Price Movement Update on Multiples SaaS businesses are generally valued on a multiple of their revenue - in most cases the projected revenue for the next 12 months.

AI = Data + Compute I’ll continue beating this drum, but we got two great quotes from Azure and AWS this week. This week we had two of the hypserscalers report (Microsoft / Azure and Google / GCP), and everyone was eager to see their results. Lots to unpack, I’ll hit on a couple of my favorite topics from this week below.

Usage on Snowflake is driven by queries run on Snowflake Azure: Neutral Tone With Strength in AI Overall I’d characterize Azure’s quarter as a net positive. They guided to 26-27% growth in Azure in Q2 (with 1% coming from AI). Their consumption is driven by usage of applications built on top of Mongo.

Next week we get all 3 hyperscalers reporting (AWS from Amazon, Azure from Microsoft, and GCP from Google). Let’s double click on Azure. Most public companies don’t report net new ARR, so I’m taking an implied ARR metric (quarterly subscription revenue x 4). The Q4 ‘22 growth rate was 38% YoY.

They each have some of the largest cloud businesses in the world in AWS, Azure and Google Cloud respectively. Most public companies don’t report net new ARR, so I’m taking an implied ARR metric (quarterly subscription revenue x 4). Overall, there was weakness across the board.

This can lead to an airpocket of valuation as companies transition to a different primary valuation metric Outside of the hypserscalers (Azure, AWS, GCP) who have uniquely benefited from AI revenue (mainly selling compute), everyone else has largely struggled. Coming in to Q1 there was broader optimism. Q4’s were generally good!

.” Let’s look at consumption revenue - this is also not technically recurring! It’s probably better described as re-occurring vs recurring. This is why the consumption players (Snowflake, Mongo, Confluent, Azure, AWS, etc) so more variability in the macro slowdown.

Hyperscalers (AWS, Azure, GCP as companies look for cloud GPUs who aren’t building out their own data centers) Infra (Data layer, orchestration, monitoring, ops, etc) Durable Applications We’ve clearly well underway of the first 3 layers monetizing. Model providers (OpenAI, Anthropic, etc as companies start building out AI).

Quickbooks and Xero are accounting SaaS products that help you send invoices, track expenses, and process payroll. Software as a Service (SaaS): SaaS providers have ready-to-use software applications over the internet on a subscription basis. Online invoicing : Manage and track invoices to maintain cash flow with ease.

The hyperscalers (AWS, Azure, GCP) are always some of the first companies to report earnings during earnings season (coming up in 2 weeks), and there’s always a read through for consumption names (meaning people believe there’s a correlation). Cloudflare is up 17%. Datadog is up 14%. Mongo is up 16%. Snowflake is up 14%.

If next quarter we get similar commentary that Azure gave us this quarter (“still a couple quarters away” without any specific guidance), then we may see market loose a little patience. The hyperscalers (AWS, Azure, GCP) are seeing some uptick, but this is largely from selling compute (ie cloud GPUs).

Azure / Confluent / Datadog reported a few weeks back (they all had March quarter ends), and their commentary suggested the worst was behind us. Most public companies don’t report net new ARR, so I’m taking an implied ARR metric (quarterly subscription revenue x 4).

Managing user accounts and access improves employee productivity, boosts security, and fosters collaboration. It also enables companies to track and manage SaaS subscriptions. For example, they may automate user provisioning, de-provisioning, or subscription management, making for a cheaper, more efficient system.

Power BI can integrate with Azure Machine Learning—plus, its ML and AI features are driven by Azure functions built into the Azure Cloud. Sprinkle offers three subscription plans: Essentials, Professional, and Enterprise. Its image analytics feature can also be useful to make better business decisions.

Then, we moved to a more customer-friendly model with SaaS and subscription-based pricing. What’s evolved over the years and is driven by hyper-scalers like Google Azure, AWS, Twilio, and Stripe is the consumption-based model. There are still some complexities around SaaS-based approaches.

Some PaaS examples include Windows Azure, Google App Engine, and Force.com. Since SaaS is typically subscription-based (aka, no licensing fees) there are lower costs upfront. However, the subscription model is flexible. Before purchasing a software subscription, research the capabilities you need and ensure they are present.

In the short term, enjoy the ride as the chase continues 😊 Kind of related to all of this - we now have seen the Q4’s from AWS, Azure and Google Cloud. Most public companies don’t report net new ARR, so I’m taking an implied ARR metric (quarterly subscription revenue x 4). Lots of deceleration in growth.

On the Microsoft earnings call they said (related to Azure): “But at some point, workloads just can't be optimized much further. To calculate implied ARR I take the subscription revenue in a quarter and multiply it by 4. My interpretation is we’re in the bottoming phase.

It Takes Time To Bounce Back Jason was the first investor in RevenueCat , a company that automates mobile subscriptions on your phone. 30% of all mobile apps with a paid subscription use RevenueCat to manage it. You can see the growth on the platform side with Azure, Google, and AWS and how much it’s accelerating in AI.

Maybe with the exception of hyperscalers (particularly Azure). Most public companies don’t report net new ARR, so I’m taking an implied ARR metric (quarterly subscription revenue x 4). Companies that do not disclose subscription rev have been left out of the analysis and are listed as NA. And the median guide is 0.4%

Server products and cloud services both saw revenue growth of 17%, with Azure revenue up 27%, while Office commercial products and cloud services revenue also grew by 13% this quarter. Three months after launching its new Basic subscription tier , the company reported that its Microsoft 365 consumer subscription numbers have now topped 65.4

But growing with a usage-model is not as straightforward as traditional subscription SaaS. Though it was pioneered in the infrastructure layer (think: AWS and Azure), it’s becoming increasingly popular for API-based products and application software. Consumption-based revenue isn’t as predictable as subscription-based revenue.

We organize all of the trending information in your field so you don't have to. Join 80,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content