This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The “Regulatory Moat” Strategy: Compliance as a Competitive Advantage Circle was the first to receive a New York State BitLicense, which is famously difficult to obtain, in 2015. This early investment in regulatory compliance has become their key differentiator against Tether and newer entrants.

On the network side, every supplier in your network is there, complete with their bank info. SMBs couldn’t do any work to add their bank accounts, and they had to trust BILL to take their money. From day one, they considered having a viable businessmodel, so they didn’t wait to build it.

This “pricing power” indicates genuine demand, not just investment bank optimism. Learning #3: Security/Compliance Isn’t a Sure Thing SailPoint’s negative returns remind us that even “essential” categories like identity management can struggle if execution falters or competition intensifies.

This setup is commonly used in marketplaces, software platforms, or businesses that facilitate payments for a network of sellers, service providers, or smaller businesses. The master merchant simplifies the onboarding process for sub-merchants by handling the complexities of payment integration, security requirements, and compliance.

The harsh reality: Most enterprises are adopting AI due to FOMO (Fear Of Missing Out) rather than for specific business outcomes. A chief data officer at a top-five global bank recently shared they have 150 generative AI projects in the lab but zero in production. Final Thoughts The AI space is well-funded but still maturing.

A typical payment processing procedure involves multiple parties, including the merchant, customer, payment processor, payment gateway, issuing bank, acquiring bank, and card networks. The processor facilitates the transaction by communicating with the payment gateway, issuing bank, and acquiring bank.

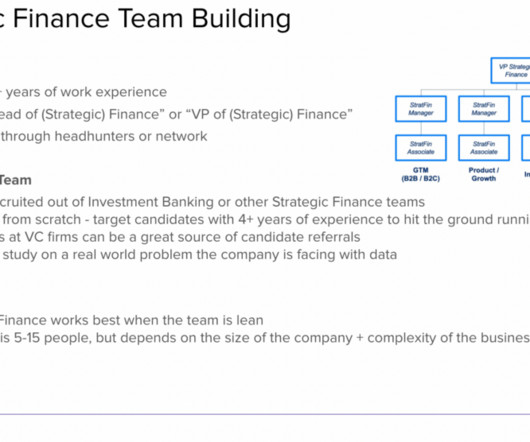

Basics: The Building Blocks of the Finance Team To understand how finance teams impact an organization, it’s helpful to break down various functions and how they support the business. Strategic Finance optimizes a company’s underlying businessmodel to create long-term value by increasing revenue and decreasing costs.

The merchant underwriting process helps reduce fraud (including chargeback volume), ensures compliance with regulations, and protects financial stability in the payment processing space. Key steps include application review, risk assessment, credit checks, and compliance verification. Learn More What is Merchant Account Underwriting?

For those that might not be familiar, FastSpring is a merchant of record platform that combines all the essential tools you need to scale a digital goods business. In simple terms, we handle everything from payments to fraud management, to custom support and tax compliance, so that sellers can focus on growing their business.

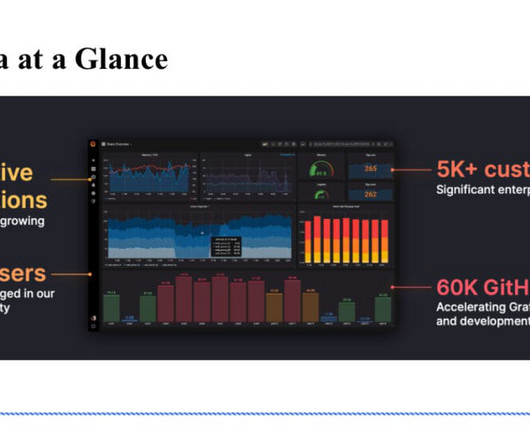

Grafana Labs still has features and capabilities they hold back that appeal to large enterprises, such as things around security and compliance. How do you drive business around that? But when they discover a large global bank using Grafana Labs, that’s where the product strategy comes in.

They learned the importance of sales tax compliance the hard way—when they had to pay millions in back taxes. When the company first began web app development and selling software-as-a-service in 2004, their businessmodel wasn’t even called SaaS. It’s not hard to understand how Basecamp got this wrong.

Lost a bank customer we had served well for 5 years and up to.5M 5M in ARR b/c we were too small a co and compliance dept blocked renewal (shoulda raised price I guess…) ” — Jared Hansen, CEO Thrilling Foods. “Dig deep about their businessmodel before sending them a proposal.”

Compliance with financial laws Calculating your tax, and then making sure that you are compliant with all the relevant tax laws is something that you have to do often. If you sign up with a billing software that cannot auto-generate reports for you, or ensure compliance, you would have to consider migration.

Acquiring bank This is the merchant bank that allows the business to receive money from card transactions and store these funds. The issuing bank This is the cardholders bank or the financial institution that issued their credit or debit card. Think: Visa, Mastercard, American Express, and Discover.

Whether you are starting a new online store or looking to grow your existing brick-and-mortar small business, you must make provisions for accepting credit card payments. A study by the Federal Reserve Bank of San Francisco showed that credit cards account for 31% of all payments, significantly more than cash at 18%, and debit cards at 29%.

In recent years, businesses have seen this massive shift from desktop to mobile devices which has forced them to develop apps with built-in integrated payment gateways. In addition to the usual concerns around security and compliance, there’s also the issue of user experience. Alipay, iDEAL, M-Pesa).

The payment processor is a financial institution that handles transactions between the two banks. To choose the right solution, you need to look at various factors when evaluating potential providers, including supported payment types, transaction fees and pricing structures, payout speed, and PCI DSS compliance.

This setup is commonly used in marketplaces, software platforms, or businesses that facilitate payments for a network of sellers, service providers, or smaller businesses. The master merchant simplifies the onboarding process for sub-merchants by handling the complexities of payment integration, security requirements, and compliance.

Payment processors verify that all necessary information is present and in the correct format and then carry it to the issuing bank or credit card network for final authorization. MasterCard or Visa), issuing bank, or electronic wallet (a.k.a., e-wallet) that you want to accept. Local Payment Processors. Learn more here.

“Industry-Centric” SaaS businessmodels offer an alternative SaaS company categorization to the “Customer-Centric” SaaS model, which is defined based on the “go-to-market” strategy used by a management team. When SaaS businessmodels originated, the most successful venture-backed startups used a horizontal model.

Understanding Payment Integration Payment integration refers to the process of incorporating payment processing capabilities into your business systems. This enables you to accept various forms of payment, such as credit cards, digital wallets, and bank transfers, directly through your website, mobile app, or point-of-sale (POS) system.

A PSP (Payment Service Provider) can equip your eCommerce and brick-and-mortar business with an all-in-one platform that supports multiple payment systems, including debit & credit cards, eWallets, and bank transfers (ACH). Read on to find out. You can easily sign up for the services of a PSP because of the low barrier to entry.

Some challenges and considerations of embedded finance and fintech involve regulatory and compliance issues, data privacy and security, and stiff competition. Request Quote Understanding Embedded Finance Embedded finance is the seamless integration of financial services and digital banking into conventionally non-financial business services.

This feature allows businesses to accept credit and debit card payments from customers helping them manage their finances more efficiently. An integrated payment processing service, Quickbooks Payments, offers businesses the option to accept credit/debit card payments as well as bank transfers (ACH).

Legal compliance. Plus, you’ll need to consider whether or not the billing platform supports businesses like yours. Plus, FastSpring takes on the liability of transactions, which means we manage chargebacks, fraud prevention, gathering and remitting consumption tax, and legal compliance. Fraud prevention and chargebacks.

There are six main payment methods used in online payments, including credit & debit cards, digital wallets, ACH & bank transfers, direct debit, Buy Now, Pay Later (BNPL) services, and cryptocurrencies. The merchant account : this is a special bank account that allows you to accept and process credit and debit card payments.

TL;DR Payment tokenization (sometimes referred to as credit or debit card tokenization) involves taking sensitive information, such as credit card data or bank account numbers, and protecting it by replacing it with a token. Compliance is essential because it both helps to prevent data breaches and cultivates customer trust.

EFT payments are transactions between the sender and receiver that transfer funds electronically from the sender’s bank account to the receiver’s. This can include peer-to-peer payments, and business-to-business (B2B) or business-to-customer (B2C) transactions. Easy to use.

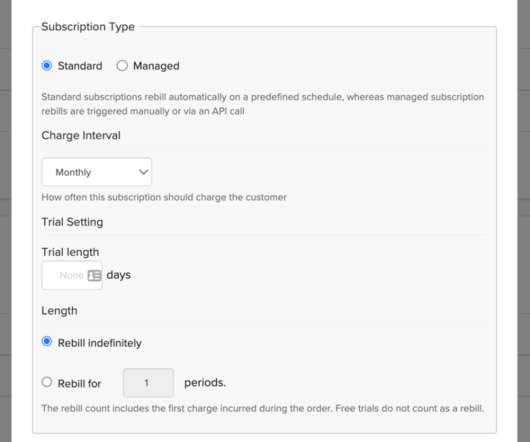

TL;DR Recurring payments refer to a financial arrangement where a customer authorizes a business to charge their account at regular intervals for products or services. There are a few types of recurring payments to be aware of, which one your business uses will depend on the businessmodel and need for recurring or automatic payments.

TL;DR Merchant processing ensures that all entities, such as the issuing bank, the acquiring bank, and the card company, work cohesively to facilitate payments between a customer and a business. In order to receive card-based payments, businesses need to have a merchant account.

If you’ve drawn on a line from your venture debt facility, money has been wired to your businessbanking account. Throughout this series, we have provided many resources to prepare you for this stage of your business journey. The lender would then wire money back through a separate bank account. What happens now?

Automated Clearing House (ACH) payments are a type of electronic bank-to-bank payment system in the US. TL;DR A payment facilitator (PayFac) is essentially a SaaS vendor or software provider that enables its users (businesses) to accept online payments from their customers through the platform itself.

There are two main ways that an ISV can become a payment provider—by adopting the ISO model or the PayFac model. In the ISO model, an ISV partners with a third party that handles merchant account setup, payment processing, risk, and compliance.

From our experience, companies who have successfully raised debt typically reach out to roughly 10 potential lenders (banks and credit funds) when setting up their initial discussions—though some ultimately decide to go even broader with 15 to 20. For now, we’ll define lenders in this section to include both banks and credit funds.

Recurring billing is a subscription payment model that automatically charges customers at regular intervals for access to a product or service. This businessmodel is used for subscriptions, memberships, retainers, and other solutions offered on a recurring basis. Learn More What is Recurring Billing?

TL;DR Payment facilitators remove the need for businesses to open merchant accounts of their own to accept payments. PayFacs handle risk assessment, underwriting, settling of funds, compliance, and chargebacks which exposes them to greater potential risks. On the other hand, this exposes PayFacs to greater potential risks.

For a merchant to accept credit cards, they need to pay both credit card processing fees to the banks involved and for the soft and hardware required to process cards. Choosing the payment processor and other items in your credit card processing tech stack will depend entirely upon your businessmodel. Card Network (e.g.,

From mobile banking and digital wallets to blockchain and peer-to-peer lending, Fintech innovations have made financial transactions more accessible, efficient, and secure. For many years, Fintech companies operated with minimal regulation, as regulatory bodies mainly concentrated on traditional banking institutions.

This approach creates a seamless experience for your customers and allows you to offload the risk, compliance, and operational costs to your payment facilitation partner, while still reaping the many advantages of Embedded Payments. Plus, a team of dedicated payments experts will be at your disposal to ensure success.

That’s why for most businesses, it’s almost impossible to make do without a credit card terminal. Finding the right credit card machine that fits your businessmodel, however, isn’t always an easy task. But if you’re stuck, worry not: in this article, we’ll help you find the best payment terminal for your business.

Speaker video: Stripe is really a set of developer tools for building and operating an online business. We work with hundreds of thousands of companies around the world on accepting payments, expanding globally, and increasingly on innovating their businessmodels for the internet and for mobile. So what did Stripe do?

They handle everything from underwriting to compliance and merchant onboarding. Additionally, they are established independent sales organizations (ISOs) with sponsorship from an acquiring bank. The best part is that it makes the entire procedure for businesses simpler. It is not just about processing payments.

Data security or compliance risks. Don’t hesitate to adjust your strategy or even pivot your businessmodel when necessary. Bank of America Bank of America’s omnichannel strategy revolves around empowering customers to carry out tasks with the same ease regardless of which channel they’re using.

It would take days or weeks to even get approved, but you also had to go through all these hoops of PCI compliance. Romain Huet : For Stripe, we had normally this idea of, this has to be much simpler, you can sign up in minutes, but you can also start accepting payments without going through all these craziness of PCI compliance processes.

We organize all of the trending information in your field so you don't have to. Join 80,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content