This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

A typical payment processing procedure involves multiple parties, including the merchant, customer, payment processor, payment gateway, issuing bank, acquiring bank, and card networks. The processor facilitates the transaction by communicating with the payment gateway, issuing bank, and acquiring bank.

In 2023, 27% of all point-of-sale (POS) payments were made using credit cards while 23% were made with debit cards. Behind every seamless payment card transaction is a complex network of banks, credit card companies, and payment systems working together to transfer money from the customer to the merchant.

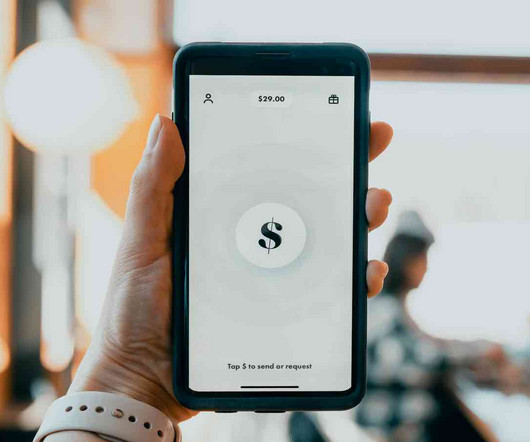

TL;DR: Electronic Funds Transfer (EFT) is the umbrella term for all electronic payments made between bank accounts. Talk to sales Understanding EFT: The Umbrella Term for Digital Transactions Ever paid for your coffee with just a tap of a card or received payment from a customer thousands of miles away? No cash or checks needed.

There are a wide variety of digital payment types, such as mobile POS systems, contactless payments, and digital wallets. Mobile phone and online bank transfers, mobile wallet payments, in-app payments, online payments, QR code payments, and all other electronic payment methods that qualify as a digital payment.

Talk to sales Understanding Ecommerce Payment Solutions An eCommerce payment solution is the underlying infrastructure that allows eCommerce businesses to accept and process card and online payments seamlessly and securely. Its the bridge between an eCommerce website, its customers, and the bank. Do you process international payments?

You may not be able to control the rates set by the banks and card providers, but what you can do is manage those fees through your payment processor. There are many processors out there that claim to save you money, and in this post we’ll take a look at two of them: Riverside Payments and Stax.

Set rate processing Subscription rate processing TL;DR Interchange fees are not collected by your payment processor or bank; they go directly to the card-issuing banks. Interchange fees vary significantly depending on the card issuer, the issuing bank, type of transaction and/or merchant type.

Years ago, point-of-sale (POS) systems were reserved for large enterprises with big budgets. Today, a small business is barely complete without a POS system. If you feel left out, the good news is that there’s a POS system out there ideal for your business. Finding one for your business can be overwhelming.

TL;DR Merchant processing ensures that all entities, such as the issuing bank, the acquiring bank, and the card company, work cohesively to facilitate payments between a customer and a business. This account temporarily holds the transaction funds until the bank verifies the payment.

TL;DR A payment gateway is a solution that securely reads and transfers a customer’s payment information to a merchant’s bank account—both for online and in-person transactions. It’s also the software in your POS system or card readers that processes the customer’s payment data in a brick-and-mortar setting.

The move was aimed at allowing both companies to focus on their core competencies: FIS on banking and capital markets technology, and Worldpay on merchant services and payment processing, transforming the way the world pays. Talk to sales Quick FAQs about Worldpay Merchant Services Q: What is Vantiv Worldpay Merchant Services by FIS?

The original sensitive data is still secured and hidden in an external data bank. Payment verification by the issuing bank means the customers bank will check whether the customer has sufficient funds to complete the transaction. Your provider should help with this. Request a Quote

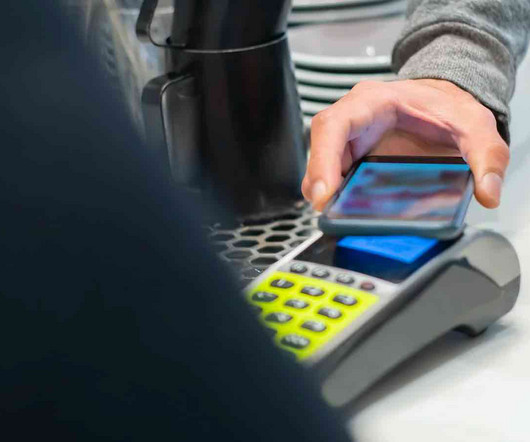

Customers can pay with their watch or phone just by tapping it on a card reader, and businesses can host an entire POS system on a mobile phone. Thanks to these modern payment solutions, credit card, and debit card users can now complete their purchases without swiping or inserting their cards at the point of sale (POS) terminals.

Embedded payments come with a lot of responsibilities, such as bank sponsorship and risk management, which is why finding the right payments partner like Stax Connect is essential to help you monetize payments and own the entire experience. Stax Connect streamlines the enrollment process for SaaS companies.

Look for a PMS that can serve as an all-in-one platform for payment processing, integrates with other technologies, offers appropriate POS equipment, and prioritizes security compliance. Your PMS is a central hub to manage payment requests and store banking information (like your routing and bank account number for ACH payments ).

Thankfully, with mobile payments from Stax , you can quickly accept and process payments from your customers. Learn all about mobile payments and why you may want to consider joining the Stax family to streamline payments and boost your small business’ productivity. Your customers are busy and so are you.

Since they’re relatively larger and have limited mobility, they’re not great options if you don’t have a single POS location. Mobile credit card terminals: These are smaller, more portable POS systems that connect to a smartphone or a tablet via Bluetooth, and are best used for businesses with no fixed locations, like food trucks.

For a merchant to accept credit cards, they need to pay both credit card processing fees to the banks involved and for the soft and hardware required to process cards. Acquiring Bank (Merchant Bank): The financial institution that establishes and maintains the merchant’s account, enabling them to accept credit card payments.

In 2015, many merchants switched to NFC-enabled terminals; by 2019, most banks were issuing contactless cards. Visa, Mastercard, and the customer’s bank) for authorization. NFC even enables smart packaging to provide customers with product and usage information at the point of sale.

Your payment terminal can be fully or semi-integrated with your POS system. Fully-Integrated Semi-Integrated Non-Integrated POS Requirements The POS and terminal are one and the same. As such, there is a 2-way sync between the devices The POS system offers One-way communication to the physical terminal. Card-present rate.

A merchant account acts as a pathway between your business, your customers, and the issuer and acquiring banks to process electronic transactions like credit cards. Without a merchant account, it’s very difficult to ensure consistent cash flow or manage multiple sales channels effectively. Request Quote What Is a Merchant Account?

That’s where Stax comes in. Legal Repercussions If a credit card data security breach occurs and the business is found to have used a non-PCI certified provider, they may face class action lawsuits from affected customers, banks, and credit card companies. Stax is a Level 1 PCI Service Provider.

A PSP (Payment Service Provider) can equip your eCommerce and brick-and-mortar business with an all-in-one platform that supports multiple payment systems, including debit & credit cards, eWallets, and bank transfers (ACH). The company also provides a card reader and mobile POS app for free. Read on to find out.

Merchants pay interchange fees to compensate the cardholder’s bank (issuer) for the risk of managing credit card accounts. You can communicate this through visible point-of-sale signage at checkout, verbal heads-up from staff, or on-screen alerts for eCommerce. Shoppers pay convenience and service fees to businesses.

Here are Stax’ Top Credit Card Processing Tips. Optimize your credit card processing speeds Slow transactions are, at best, an annoyance to customers, and at worst, result in lost sales, especially online. Request a custom quote to see how Stax Pay can work for you. It’s best to avoid long-term contracts.

Automated Clearing House (ACH) payments are a type of electronic bank-to-bank payment system in the US. An ACH payment facilitator, therefore, is simply a PayFac that allows users to accept payments through an electronic bank-to-bank network. In Q3 of 2023, the total volume of payouts on ACH networks reached 7.8

FIS Global reports that in Norway, Sweden, and other Scandinavian countries, more than 90% of transactions processed at point-of-sale (POS) in 2023 were cashless. PayFacs act as intermediaries between merchants and payment processors or banks. Contact us today for a consultation and learn how we can help.

Merchants can accept payments anywhere with mobile credit card processing, eliminating the need for a fixed point-of-sale terminal. That can mean paying the plumber by credit card in their own house or paying for a sweater with the sales associate who helped them pick it out, rather than going to find the POS desk.

The acquiring bank (or issuing bank or acquirer) is the financial institution that enables merchants to accept payments, transferring funds from customers to the merchant’s account. The payment gateway acts as a virtual bridge, securely transmitting payment information between the merchant, customer, and acquiring bank.

By facilitating credit card transactions, merchant service providers act as intermediaries between credit card companies and the issuing banks. Interchange fees An interchange fee is paid by the merchant’s acquiring bank to the issuing bank every time a credit card transaction is made. Account fees. PCI compliance fees.

Credit card merchant fees are split between multiple key players- merchants, credit card networks, banks, and processors. Interchange fees are set by credit card issuers, such as Bank of America, Citi, or Chase, and are adjusted every year in April and October. Stax is one card payment processor that uses this pricing model.

Stax, for example, charges 0% markups on top of interchange, giving you the lowest percentage per transaction rate. For example, Stax charges a flat monthly membership in exchange for a 0% markup rate, a transaction cost of just a few cents, and no ancillary fees.

TL;DR Merchant underwriting is the risk level assessment process an acquiring bank carries out on every new merchant before they grant them a merchant account. The bank assumes the risk on behalf of the business and needs to make sure that they screen new businesses before handing out merchant accounts. What Is Merchant Underwriting?

Most B2C transactions are performed at the point of sale (POS), whether it’s eCommerce or in-store checkout, which lends them to faster payment methods like mobile payments more often than B2B transactions. Business to consumer (B2C), by comparison, relies on speedy payment processing to transact on the spot.

CardX by Stax is a trusted leader in helping your business seamlessly and easily implement credit card surcharging, ensuring you stay compliant and save on transaction fees. It is important to note that if there is a difference between the card and cash price, it is essential to clearly communicate through proper signage at the point of sale.

Setting up ACH payments is easy with a great merchant account service like Stax. Once the client sets up a payment profile with their banking information, the payment can be automated and paperless. The Federal Trade Commission offers straightforward advice: “don’t give out your bank account number.”

TL;DR Credit card interchange fees are the fees that merchants pay to banks and credit card companies every time they accept credit cards. Credit card interchange fees are the fees that merchants pay to banks and credit card companies every time they take a non-cash purchase. Learn More What are credit card interchange fees?

Request Quote Understanding Embedded Finance Embedded finance is the seamless integration of financial services and digital banking into conventionally non-financial business services. Examples of embedded finance today include: Embedded Banking Embedded finance, embedded banking, and Banking as a Service (BaaS) are often used synonymously.

A secure payment gateway is a technology platform that facilitates the secure transmission of payment information between a merchant’s website or point-of-sale system and the payment processor or acquiring bank. With Stax, you can rest easy knowing your data is protected and secure.

Point of sale terminals are reprogrammed (or pre-programmed) to add the appropriate fee without manual input from merchants. If you’re working with a payment processing provider like Stax , they can take care of much of the following. Here at Stax, we can reprogram existing terminals and also have pre-programmed options.

It is added at the point of sale and depends on the total amount of a transaction and the cap set by credit card companies. It is added at the point of sale and depends on the total amount of a transaction and the cap set by credit card companies. What Is a Credit Card Surcharge?

It is added at the point of sale and depends on the total amount of a transaction and the cap set by credit card companies. It is added at the point of sale and depends on the total amount of a transaction and the cap set by credit card companies. Learn More What Is a Credit Card Surcharge?

Learn More Understanding Online Terminals (aka Virtual Terminals) An online terminal, often called a virtual terminal, is a web-based application that enables online payments without needing a physical credit card machine or POS (Point of Sale) system. Q: Why do businesses need an online terminal?

Being cloud-based allows you to sync your bookkeeping app with your bank accounts and other business management tools to generate real-time financial reports. These third-party integrations include your eCommerce, POS, payment processing, payroll, inventory management, and tax preparation software platforms.

We organize all of the trending information in your field so you don't have to. Join 80,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content