This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

With Databricks now one of the largest pre-IPO technology companies, with $10 billion of expected non-dilutive financing and a valuation of $62 billion, Ron’s insights are gold for any revenue leader looking to scale. Our founders focused on adoption first, not revenue, Ron explains. The takeaway? The takeaway?

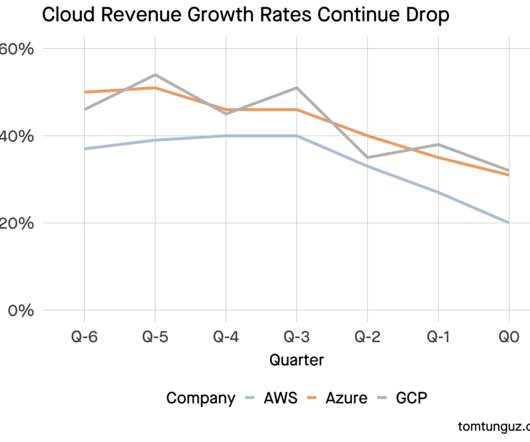

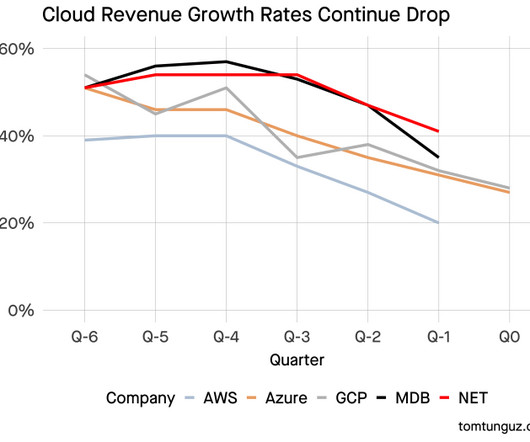

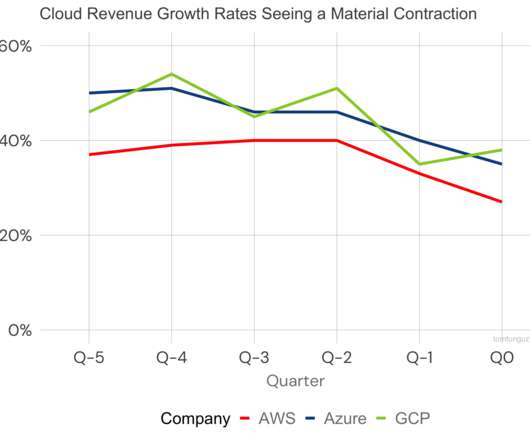

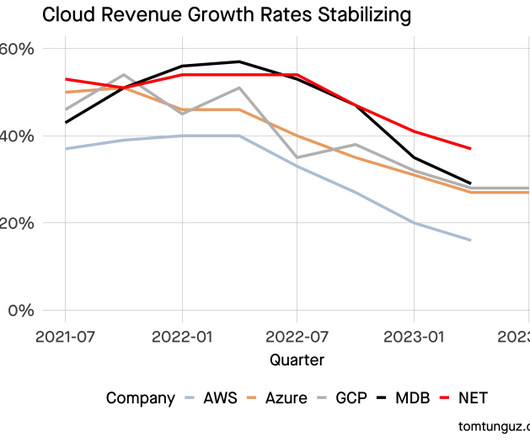

A year ago, AWS, GCP, & Azure averaged 44% annual growth. So far in the first month of the year, AWS year-over-year revenue growth is in the mid-teens. So far in the first month of the year, AWS year-over-year revenue growth is in the mid-teens. Google: [We] are pushing Google Cloud to Profitability.

The charts below show the change in quarterly revenue YoY (so Q1 ‘24 rev - Q1 ‘23 rev) going back to 2017. GCP data is a bit more noisy as they don’t disclose GCP itself, but rather Google Cloud which includes GSuite. Beating consensus revenue estimates is the first aspect of a successful quarter.

Google’s growth rate fell to 35%, a 29% decline from the trailing 4 quarter average of 49% annual revenue growth. GCP’s data point is less rosy. Here are some hypotheses: Google may have greater customer concentration in GCP than Azure. Why do these results diverge?

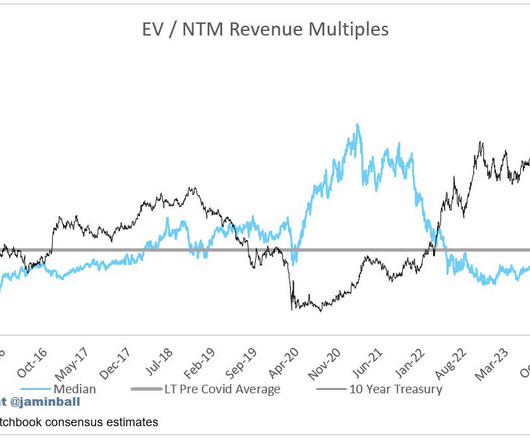

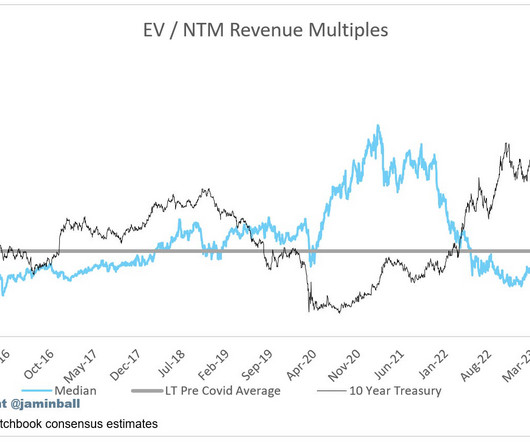

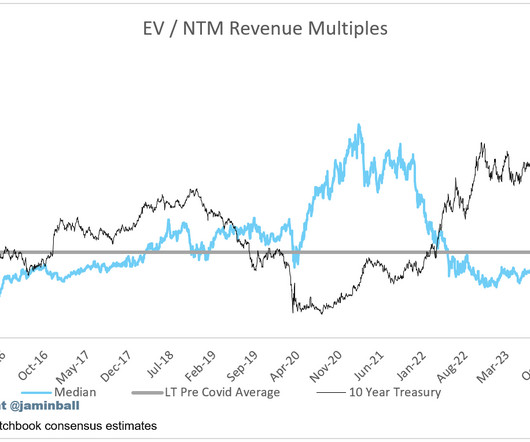

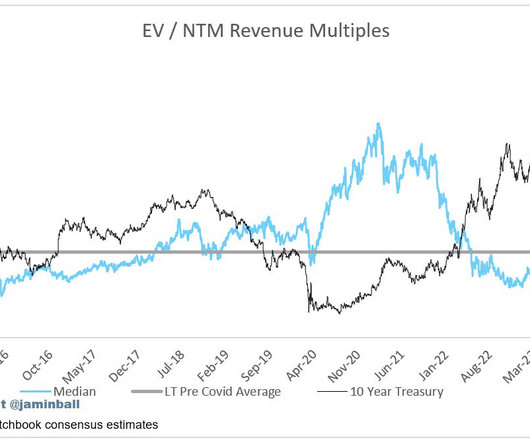

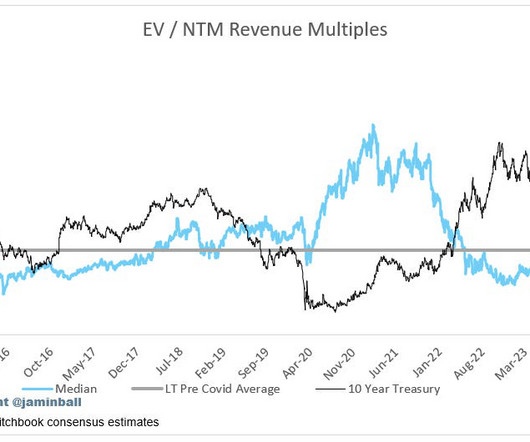

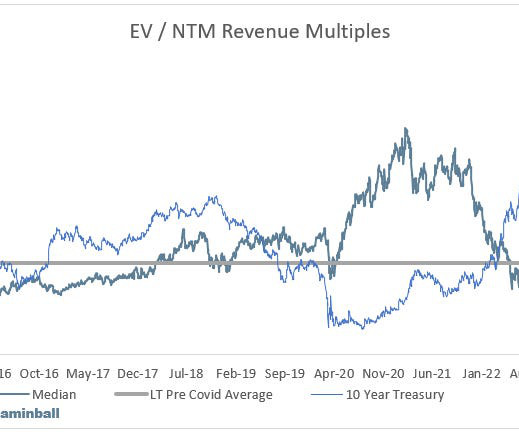

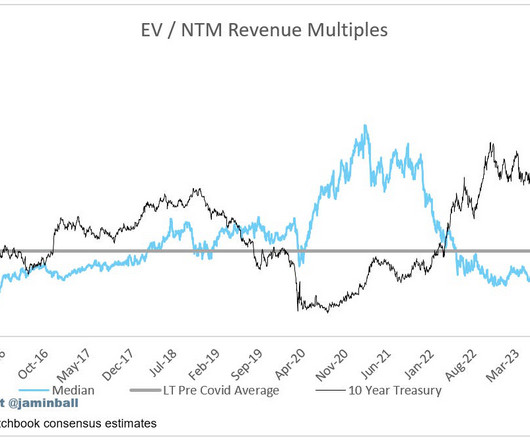

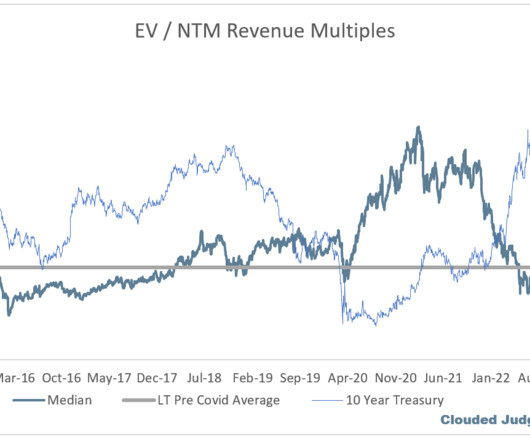

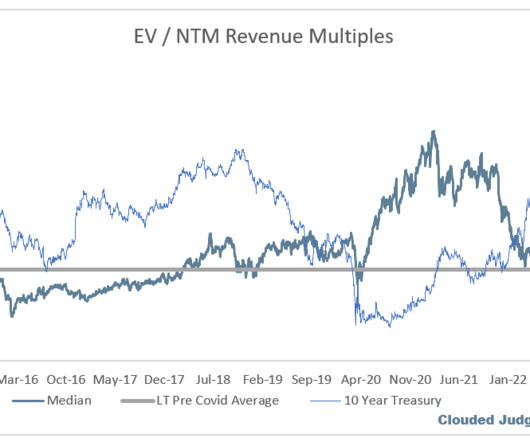

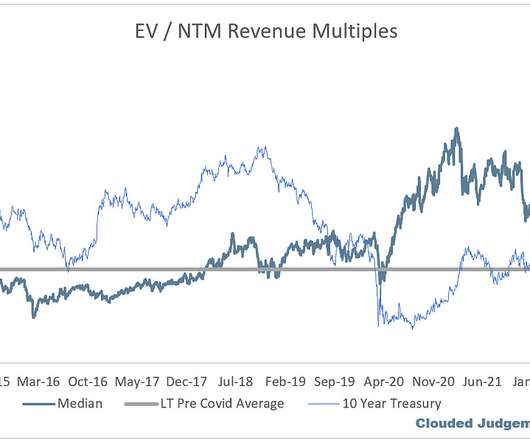

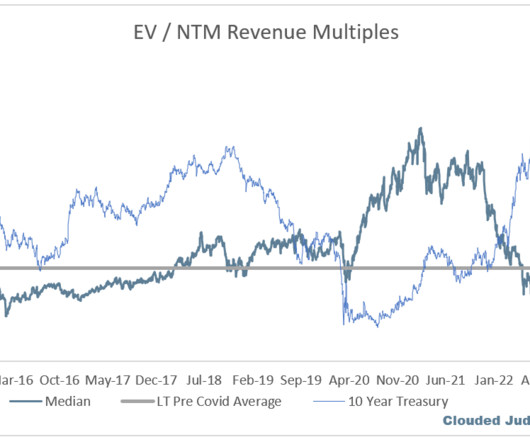

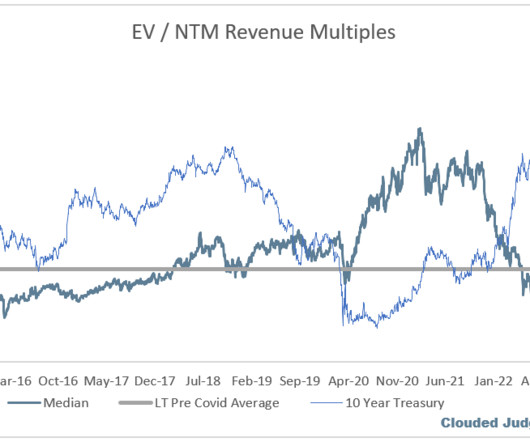

As a result, software vendors often see an uptick in revenue and bookings during these periods. Top 10 EV / NTM Revenue Multiples Top 10 Weekly Share Price Movement Update on Multiples SaaS businesses are generally valued on a multiple of their revenue - in most cases the projected revenue for the next 12 months.

Yesterday, Microsoft & Google announced earnings. Google Cloud Platform (GCP) & Microsoft Azure had strong quarters with about 28% annual revenue growth each. In Azure, we expect revenue growth to be 26% to 27% in constant currency, including roughly 1 point from AI services.

Maast offers payments, banking, lending and more as features in software provider’s platforms – with one relationship, contract and integration. Which means better customer relationships, more data, and new sources of revenue.

Using the Drift Conversation Cloud, businesses can personalize experiences that lead to more quality pipeline, revenue and lifelong customers. More than 5,000 customers use Drift to deliver a more enjoyable and more human buying experience that builds trust and accelerates revenue. Usually, it takes a paradigm shift to grow.

ChurnZero is the Customer Success platform and partner for growing SaaS and subscription businesses. You need an efficient way to keep your customers successful, reduce churn, drive adoption, and increase net revenue retention.

Infrastructure revenue growth averaged 33% this quarter, which is astounding considering we’re talking about businesses that sum to more than $50b of revenue per quarter. At a 7x multiple of revenue, that is another $84b of market cap creation, in theory. Let’s put these figures into context.

We help B2B SaaS marketers turn organic search into a source of repeatable revenue through software and coaching. DuploCloud offers an end-to-end DevOps software platform for dev teams that don’t have dedicated DevOps engineers and augments those that do.

“Q3 product revenue grew 34% year-over-year to reach $698 million. " Here’s another insight : Google’s cloud is more expensive for customers than others : " One of the reasons why GCP is not as big as just so much more expensive for our customers to operate in GCP than it is in AWS and Azure.

In my 148 public SaaS companies (including most of the categories of this list but not AWS, Azure, GCP) the aggregate revenue is $185B. No matter what, the wave of enterprise spending that fueled 100 SaaS and Cloud unicorns is just getting bigger and strong. This is your time, folks. Go make it happen.

Both Google & Microsoft announced growth rates in GCP & Azure that held steady from one quarter to the next. UIPath doesn’t share MAU count & Microsoft didn’t break out revenue, so comparing the two businesses’ size directly isn’t possible. Amazon, Cloudflare, & Mongo announce soon.

We now have results from the three hypersclaers (AWS / Azure / GCP). Quarterly Reports Summary Top 10 EV / NTM Revenue Multiples Top 10 Weekly Share Price Movement Update on Multiples SaaS businesses are generally valued on a multiple of their revenue - in most cases the projected revenue for the next 12 months.

Microsoft launched Azure in 2010, and Google launched GCP to the public in 2011 (they launched a preview of Google App Engine in 2008, but made it publicly available in 2011). Revenue multiples are a shorthand valuation framework. The promise of SaaS is that growth in the early years leads to profits in the mature years.

And no one raised full year guide >2% The median “beat” (Q1 revenue over Q1 consensus estimates) was 1.5%, which is the lowest it’s been in the last 4 years Overall, it’s been a TOUGH quarter for software companies. Revenue multiples are a shorthand valuation framework. Overall Stats: Overall Median: 5.7x

” As growth starts to slow, it gets harder and harder to justify using revenue multiples as a primary valuation metric. Any kind of inference really can rack up bills quickly (see growth in hyperscaler revenue…), and AI talent isn’t cheap. Revenue multiples are a shorthand valuation framework.

Hyperscalers (AWS, Azure, GCP as companies look for cloud GPUs who aren’t building out their own data centers) Infra (Data layer, orchestration, monitoring, ops, etc) Durable Applications We’ve clearly well underway of the first 3 layers monetizing. Revenue multiples are a shorthand valuation framework. Bucketed by Growth.

Cloud Giants Report Q2 We also got the Q2 quarters from AWS / Azure / GCP this week! Quarterly Reports Summary Top 10 EV / NTM Revenue Multiples Top 10 Weekly Share Price Movement Update on Multiples SaaS businesses are generally valued on a multiple of their revenue - in most cases the projected revenue for the next 12 months.

You can see more detail about their net new ARR added each quarter below Quarterly Reports Summary Top 10 EV / NTM Revenue Multiples Top 10 Weekly Share Price Movement Update on Multiples SaaS businesses are generally valued on a multiple of their revenue - in most cases the projected revenue for the next 12 months.

Next week we get all 3 hyperscalers reporting (AWS from Amazon, Azure from Microsoft, and GCP from Google). Top 10 EV / NTM Revenue Multiples Top 10 Weekly Share Price Movement Update on Multiples SaaS businesses are generally valued on a multiple of their revenue - in most cases the projected revenue for the next 12 months.

Hyperscalers Report Quarterly Earnings This week we saw AWS (Amazon), GCP (Google) and Azure (Microsoft) report earnings. Top 10 EV / NTM Revenue Multiples Top 10 Weekly Share Price Movement Update on Multiples SaaS businesses are valued on a multiple of their revenue - in most cases the projected revenue for the next 12 months.

While the overall median revenue multiple of the software universe is ~6x (which is ~25% below the long term average of ~8x), high growth software is currently trading at a premium to it’s long term average (9.4x The hyperscalers (AWS, Azure, GCP) are seeing some uptick, but this is largely from selling compute (ie cloud GPUs).

This week we had two of the hypserscalers report (Microsoft / Azure and Google / GCP), and everyone was eager to see their results. The bars represent the YoY revenue growth, and the yellow line is the stock price. However, revenue growth didn’t bottom until Q3 ‘09. AWS reports next week. So what did we learn?

Iceberg is open source, and is the leading table format, having been adopted by Snowflake, AWS, GCP, Databricks, Confluent and many others, with contributions and usage coming from some of the largest organizations like Netflix, Apple, LinkedIn, Adobe, Salesforce, Stripe, Pinterest, AirBNB, Expedia and many others.

Again, things get slightly more complicated for SaaS businesses who often have to take unearned revenue into account when calculating their profits. Examples of cost management software include in-platform cost optimization modules like GCP Billing and AWS Cost Explorer.

At Tackle, we have seen our sellers experience huge revenue growth, the product catalog is expanding rapidly for buyers, and budgets are growing at unprecedented rates. So, it’s no wonder that it has been a massive year in the Cloud Marketplace business.

It’s less expensive than it’s ever been in terms of actually getting a product to market, whether it’s leveraging platforms like Salesforce or GCP or AWS or Heroku. Revenue has only garnered after that fact. There are plenty of companies that actually have that initial success. You got 37 the first go-round.

There are many vendor benefits, too — it is easier to sell and it embodies a customer success solution orientation that drives high customer lifetime value and revenue. These contracts are very common in ‘revenue share’ models (i.e., Less predictable revenue. impact on recognized revenue and costs, E/R, SG&A, etc.).

Bigger swings generally mean a longer amount of time building toward something that could work in the future. Google on GCP? Extreme examples sure, but partially why they are extreme is these companies’ new product development has to move revenue growth at what are now some of the largest companies in the world.

“AWS’ AI business is a multibillion-dollar revenue run rate business that continues to grow at a triple-digit year-over-year percentage and is growing more than 3x faster at this stage of its evolution as AWS itself grew, and we felt like AWS grew pretty quickly.” GCP 23 35 52.2% Azure 26 33 26.9%

We organize all of the trending information in your field so you don't have to. Join 80,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content