This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

What is a paymentfacilitator? A paymentfacilitator (or PayFac) is a software platforms all-in-one paymentprocessing solution. Instead of your customers needing to create their own merchant account to processpayments, you as the PayFac developer handle all the payments setup and complexity for them.

But throughout this turmoil, startups must adopt a process to craft a good pricing strategy, and re-evaluate prices periodically, at least once per year. Many infrastructure as a service companies do this. Contract Length Many SaaS startups launch with monthly pricing which encourages customers to try the product and engenders demand.

SaaStr CEO and founder Jason Lemkin chats with Mangomint CEO Daniel Lang about why vertical SaaS is booming and how Mangomint got to 110% NRR. What was once considered too small or too niche, vertical SaaS has recently emerged as a hotbed of innovation and profitability. Full-Stack SaaS for SMBs Toast today is worth $14B at $1.5B

Jason starts with the meta-question we’ve been asking a lot of SaaS leaders lately ( Klaviyo , ZoomInfo ) — ‘are we in a downturn?’ Going Long We’ve written before on the power of going long in SaaS. Then, in 2017, with around $50M in revenue, BILL added payment capabilities. in revenue.

Fraud is ever changing – especially for merchants that offer online services and subscriptions. In the report, you’ll find: The scale and type of fraud seen in the global marketplace. How fraud changes based on the size of business.

What To Do Next Audit your current payment/finance offerings Survey your customers about their financial pain points Start conversations with embedded finance providers Focus on partners who can scale globally with you Remember: In SaaS, revenue diversity is power.

The world of Embedded Payments saw remarkable developments in 2024, shaping strategies and innovations across the industry. In a compelling discussion on PayFAQ: The Embedded Payments podcast, Ian Hillis hosted payments veterans Ella Aguirre and Michael Veatch to reflect on the past year.

Selling internationally can get complicated very quickly if you’re trying to manage cross border payments yourself. And typical paymentservice providers won’t help you with most of those concerns. Read on to learn: Why cross border payments are key to taking your business global.

Pricing is more than just a number on a contract — when used thoughtfully, it can become a strategic tool for your SaaS product that can drive product adoption, customer satisfaction, and business growth. Scaling stage: Reduced to single-user plans to maximize accessibility.

Lesson #1: Invest In Customer Support Early Cloudinary strongly believes that customer success and support are enablers of PLG growth and aren’t just a cost center. Twelve years after hiring their first CS person, customer service is still the number two reason people like Cloudinary and what drives word of mouth in the developer ecosystem.

In this episode of PayFAQ: The Embedded Payments Podcast, host Ian Hillis welcomes Matt Downs, President of Worldpay for Platforms, to discuss software-led payments predictions for 2025 and beyond. Navigating market dynamics in 2025 and beyond Matt emphasized the cyclical nature of the payments industry, likening it to a pendulum.

What makes a company choose one SaaSpaymentprocessing provider over another? We know that conversion rates for SaaS and software companies will vary by 30% or more just based on the checkout experience. If you’re taking payments, your customer’s financial and personal data is one of your top concerns.

Subscription Models: Usio will provide general insights into why subscription-based paymentprocessing is often considered advantageous for Software as a Service (SaaS) businesses. Predictable Revenue Streams: Subscription models provide a consistent and predictable revenue stream for SaaS companies.

With thousands of new startups emerging everyday and the average turnover rate for business applications trending at 39% annually, the SaaS industry couldn’t be more competitive. Despite the hyper competition, many SaaS providers take their organization’s paymentprocessing experience for granted. Securing payments.

SMB SaaS has a lot going for it: – Millions of them – Short sales cycles – Easier compete. So many VCs and others have gotten more and more excited about SMB SaaS. But SMB SaaS has a lot of challenges, too: Churn is much higher. of public SaaS companies are primarily SMB focused. Much higher.

As a growing SaaS company, there is a lot to think about in a day: How is my ARR doing? vary on how they handle sales tax and SaaS. As you scale up, it’s essential to ensure that your sales tax management process is accurate and automated, so you don’t run into compliance issues in the future. . Here’s why you should. .

I was lucky to catch up recently with one of my very favorite SaaS founders, René Lacerte, CEO Bill.com. Bill.com had to develop a network that today has millions on vendors processing bills and payments on it. Bill.com had to develop a network that today has millions on vendors processing bills and payments on it.

The Latin American SaaS landscape is hustling and bustling, having seen more IPOs in the last 6 months than the previous 20 years combined. We will gather 300 leading SaaS founders, executives and investors for three days packed with opportunities and rich exchange of knowledge to push the whole ecosystem forward. Founded : 2013.

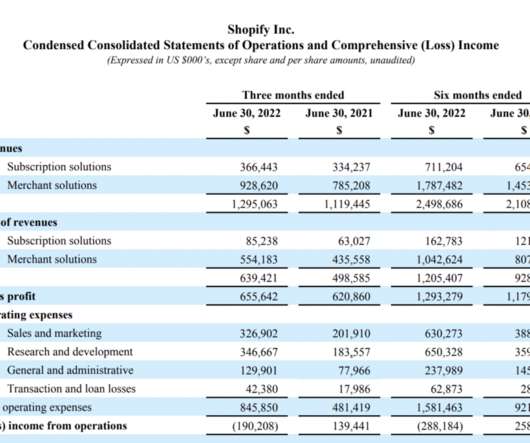

Few SaaS leaders have gone through more post-pandemic change than Shopify and Zoom. SaaS growth slowed to 10% year-over-year, down from a peak overall growth of almost 100% (!) Gross Margins declining toward 50% as payments, merchant services and more outpace the growth of SaaS subcriptions. More on that here.

Monetizing ecommerce via subscriptions, but not paymentprocessing. Billion in GMV processed, up a stunning 91% from 2019. But in contrast to Wix and Shopify, it doesn’t keep much of the revenue from merchant services itself. Rather, it charges for software subscriptions to take payments on its websites.

Offering its services as a freemium-based model, CircleCI recognizes driving trials as the cornerstone of a go-to-market strategy for any developer tool. . Developers come to CircleCI to use their services for free but the user needs increase as they build for commercial purposes. changes the key processes of your business.”.

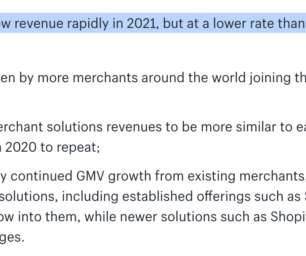

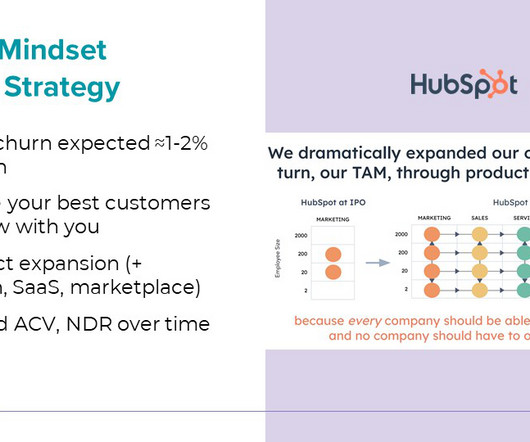

The Covid Boost for SaaS. It would be so helpful to know, as the #1 leader in SMB eCommerce, and also one of the very top leaders in SaaS SMB overall. When you add in payments, i.e. merchant services, NRR for 2018+ is about 110%, based on the below new chart. But likely it’s below 100% excluding payments.

A lot of our SaaS older times don’t quite know what to make with a lot of B2B startups these days, let alone some public SaaS companies. But like “Cloud” and “SaaS”, its definitely has evolved. But like “Cloud” and “SaaS”, its definitely has evolved. Only half does.

Bill.com is one of the quiet SaaS success stories. Now they’ve scaled to $200m+ ARR growing 38% selling just to 100,000+ SMBs, solving a hard problem (i.e., automating the back office and payments and billing for SMBs), and doing it with 120%+ NRR. Making more and more money on each payment. Even small customers.

So over the past decade-and-a-half we’ve come up with a lot of yardsticks, metrics and rules for SaaS companies. But — they are broken if you aren’t really a traditional, 100%+ NRR SaaS company. In particular: Hybrid SaaS with payments and fintech usually has far, far lower gross margins than pure software.

Simplify Subscription Payments with SaaS Solution Say goodbye to long, confusing, and costly paymentprocesses. Say hello to efficiency and simplicity with advanced SaaSpayment solutions for subscription services. Improved Payment Security : Security is a major concern in paymentprocessing.

SaaS companies are continually seeking innovative strategies to not just maintain but amplify their growth trajectory and increase revenue. One pivotal yet often overlooked area is payments. We’ll delve into how SaaS companies are leveraging Usio Integrated Payment Solutions to propel their growth and increase revenue.

In a world where we’re spending more and more time online and every click is a potential transaction, it’s no surprise the eCommerce and digital payments sectors are experiencing exponential growth. In this article, we’ll dive into the intricacies of two types of players in the eCommerce ecosystem: payment gateways and paymentfacilitators.

So, despite SaaS multiple and the public markets being at near record highs, we’ve seen things start to … wobble a bit overall in tech: The WeWork IPO simply failed , and the Peloton and Direct Smile IPOs were broken. One of the greatest SaaS companies of all times, but still, it turned out to be mortal. Slack is mortal.

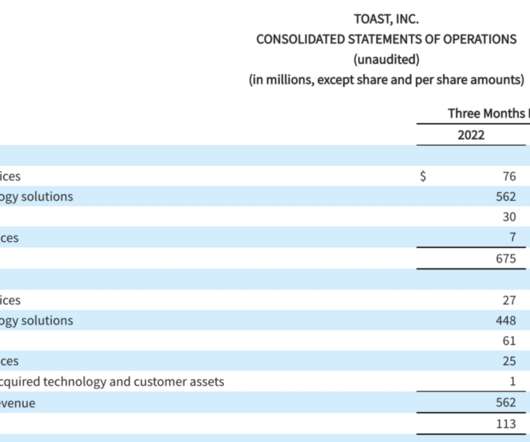

Toast isn’t accelerating the way some SaaS leaders are, but still, 59% growth at $800m in ARR is something a few years back we would never have thought possible. #2. As the brand scales, they get more of a boost from inbound. #5. Overall, Toast isn’t quite a SaaS company. 5 Interesting Learnings: #1.

So there’s a vertical SaaS company at over $600m ARR that is extremely well known to its customers that you’ve probably never heard of — Instructure. It was founded in 2008 but took a while to get going, hitting $1m in revenue in 2011 selling to Utah schools — and then scaled from there. It took on $1.7

This episode is an excerpt from a session at SaaStr Scale. What you’ll see in that cloud spend box is actually Gartner’s 2020 estimate for infrastructure as a service spending for companies, which was $50 billion. million subscriptions transacted and Google’s marketplace has seen 3X growth in SaaS sales.

With more and more businesses offering their services online, paymentprocessing is now taking centerstage. Creating a secure and smooth payment pipeline is becoming increasingly important, with users expecting more in-app freedom with the ability to purchase or upgrade their accounts with just a few clicks.

When we announced a few weeks ago that we would be bringing our leading SaaS conference to Asia, and running it in Hong Kong, many locals thanked us for choosing the city. Tienpay enables merchant payments, person-to-person transfers, and vouchers, among other functionalities. . Founders : William Tien. Founded : 2011.

It’s done it by going more upmarket, and better monetizing partners and services. A reminder that adding a bit of fintech to your SaaS can be a huge accelerant. A reminder that adding a bit of fintech to your SaaS can be a huge accelerant. Services and partners are also a big part of their growth story.

Fast forward to today, and we can add an important nuance to that: a second core product not only helps you grow faster at scale (a bigger TAM), but it drives up NRR and more revenue from your existing customers. Pretty good for SMB SaaS. In fact, now it’s more than 2x the size of its SaaS software alone.

20X year 1⃣ 12X year 2⃣ 5X year 3⃣ #deelspeed @deel [link] — Shuooo (@shuoshuooshuooo) January 23, 2023 When we look at SaaS companies’ success stories, everything looks great on their growth maps. Shuo Wang is the CRO and co-founder of Deel, one of the fastest-growing SaaS companies.

I felt like when I was a SaaS CEO and had to go profitable, they helped saved my rear. But as time has gone by, and I’ve worked with more SaaS companies, I’ve also seen the downside of annual contracts at many start-ups as well: Annual deal collections can be tough for start-ups. This is still true. So for sure, do that.

Throw in the rise of social media and mobile web payment systems like Stripe and Braintree, and something revolutionary was at our doorstep. 2020 wasn’t the only reason small business owners adopted software solutions, but it sure sped up the process. Anyone can open a store and go through the process without talking to anyone.

1M in ARR per employee could be a new efficiency record at IPO for SaaS. Sometimes, the self-serve / PLG engine stalls out at a certain scale. Their tiniest customers still have higher churn, as with almost every other SaaS company. Fintech is the engine of growth at scale. 5 Interesting Learnings: #1. Oftentimes, even.

In the dynamic world of Software as a Service (SaaS), staying ahead of the curve means continuously evolving and integrating new functionalities that enhance user experience and streamline business operations. One such critical functionality is integrated payments. As your SaaS business grows, your payment needs will evolve.

The SaaS industry has seen explosive growth in the past decadeand this is expected to continue this year. Data cited by Statista shows that the software as service is expected to hit $299 billion by the end of 2025. Part of this can be attributed to the SaaS model’s unique aspect of relying primarily on future revenue.

For operations leaders in healthcare SaaS, scaling is a balancing act. As demand grows, so does the pressure to get new clients up and running without sacrificing service quality. Slow underwriting, poor communication, and delayed onboarding with payment providers can turn a growth opportunity into a logistical headache.

No matter how innovative a product might be, a business can only succeed if it enables its customers. Suzanne Xie kicked off her journey in SaaS as the Founder and CEO of Lightwell. What makes a SaaS business so hard? You can deploy subscriptions as a service, billing as a service, fraud prevention as a service.

We organize all of the trending information in your field so you don't have to. Join 80,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content