This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Additionally, if you look at the mobile shift, the iPhone was released in 2007 but we didn’t get our first mobile apps like Uber and Snapchat until 2009 and 2010. It wasn’t until years later that Workday and Salesforce and a whole generation of SaaS companies came along to build on top of that infrastructure.

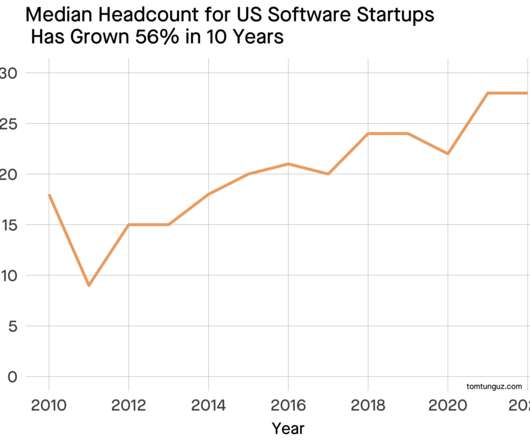

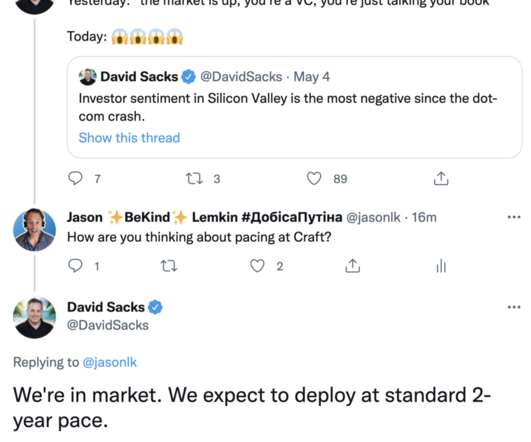

In 2010, the median software Series A startup raised $3.2m & employed 15 people at about $150k average cost. If the Series A market follows suit, the median series A will fall to $7.8m, which means a 28 person company will have 17 months’ of runway - effectively identical to 2010 runway. Let me explain : Era. Median Salary.

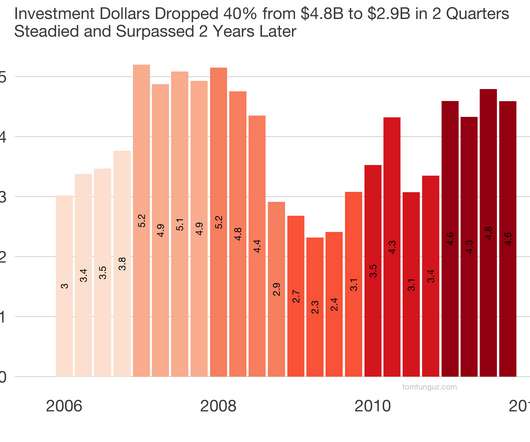

The market bounced back to similar levels once in Q2 2010, but needed eight quarters to return to its previous volumes. The Series B market had a nice resurgence as well, followed by a retrenchment in late 2010 and then another surge. That grew to about $5B per quarter in 2007 and early 2008. in the quarters following the crash.

Let’s compare data from 2010 and 2021 to understand the longitudinal trends in cash and equity compensation. A VP of Engineering in a Bay Area startup that has raised less than twenty-five million dollars earned 33% more in 2021 than 2010. 2010 Equity. Cash Change. A nice bump. 2021 Equity. Equity Change.

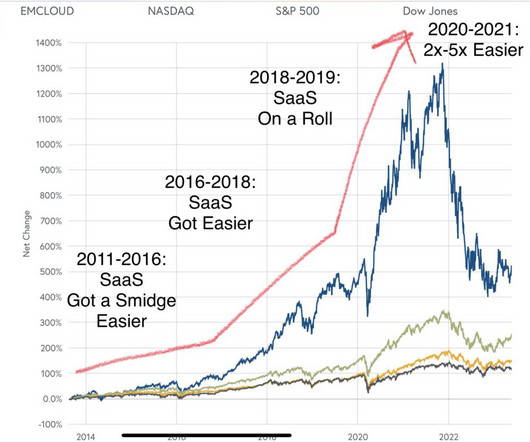

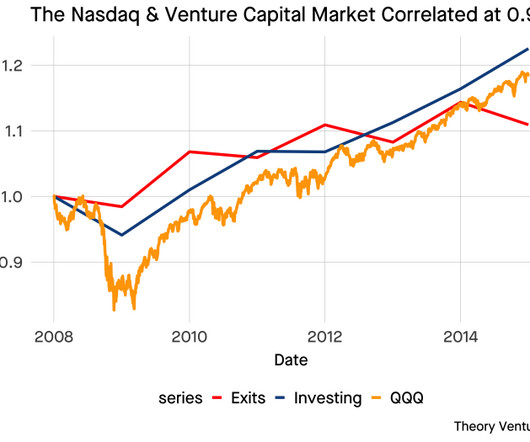

In 2010, classic SaaS was booming, the benefits of a subscription model were finally becoming clear to the public markets and the mass-market. The chart above breaks out 14 different software categories and shows the amount of dollars invested in each category indexed to 2010 levels.

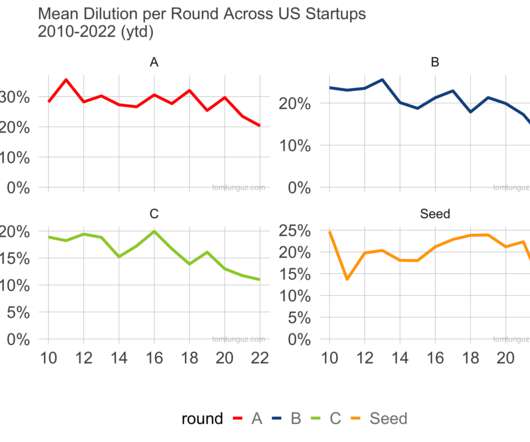

Series A has dropped from 30% to 20%; Series B from 22.5% to 12%; and Series C from 18% to 11%. Across financing rounds, dilution from capital has fallen by 30-50% in that decade. Cumulative Dilution Points. Here’s a table of cumulative dilution points for a hypothetical startup raising 4 rounds in one year.

The Seeds of the 2010 era are the pre-Seeds of today, making the comparison impure. Many new seed funds started & the rate of company formation surged during the early 2020s driven by an ebullient capital markets. Also, the definition of a Seed round has changed. Regardless, Series As haven’t grown to nearly the extent of Seeds.

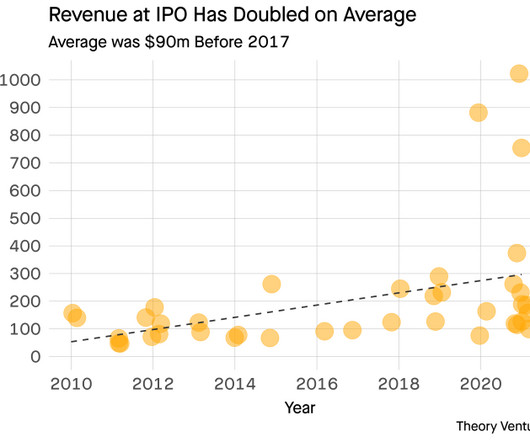

In 2010, one venture dollar bought $1.24 If we look at the ROIC across IPOs across the last 12 years or so, we see that same initial dynamic of incredibly efficient companies in the 2010 and 2014 IPO cohorts. It’s tripled from about $92m to more than $300M since 2010. One venture dollar bought forty-two cents at IPO.

The top left chart shows a $1M round had about 41% market share in 2010; that grew to about 54% in 2014; now it has fallen to 35%. But is now at the same level it was in 2010. In 2010, it was very likely that a business raised a $1M round before raising a $3-5M dollar round. The $3M round has suffered a similar loss of share.

in May 2009 … but then returned to normal 2% by 2010: #4. Customers kept buying more SaaS than ever, which masked all-time high churn in SMB accounts. SMBs just plain went out of business in ’08-’09. So our gross SMB churn spiked to a crazy high of 5.5%

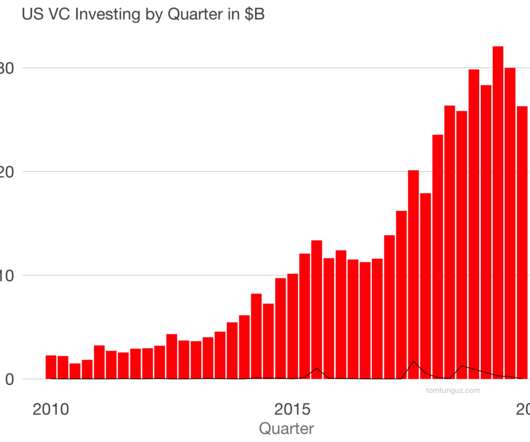

And it would be 4x the size of 2010. Let’s go through these one by one using the Pitchbook Venture Monitor Report. VCs have raised $57b through Q3, implying $75b for the year, a total which would eclipse any other year in the last decade. The late stage venture market is on pace to set a record in 2020.

We gathered data on the US venture-backed software companies that went public between 2010 & today. What does it take to go public? Has it changed over the last 15 years? We corrected the trailing 12 months’ revenue at the time of IPO for inflation & plotted the data.

Since 2010, the number of round by quarter has followed a periodic growth, with consistent seasonality. Mean round sizes have increased from 5 million in 2010 to 17.5 I wondered if Softbank's changes in investment strategy had much to do with it, but as the chart shows, they were not a meaningful contributor.

Founded back in 2010 (SaaS takes time!) So we’ve finally got another SaaS IPO gearing up — OneStream. It’s SaaS for CFOs and financial operations, a large but somewhat under-discussed category. SAP and Oracle are very strong here.

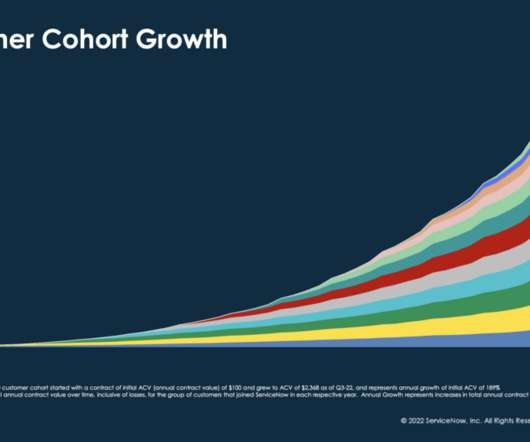

It’s 2010 customers have grown their ACV … a stunning 24x over the following 12+ years. Others are seeing this as well, although some, like MongoDB, aren’t. But many in SaaS are seeing tougher times in Europe than North America. ServiceNow’s growth has slowed there: And a few interesting learnings: #6.

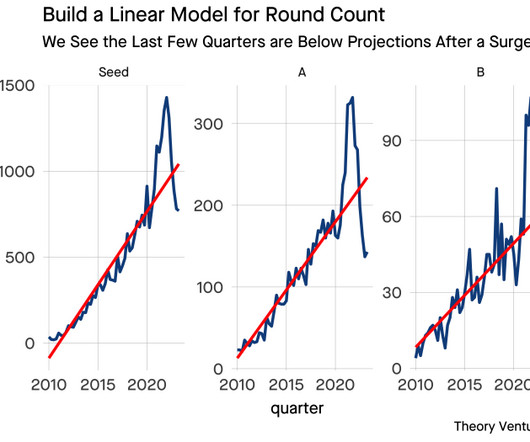

The red is a linear model based on data from 2010 to 2018 that predicts activity rates for each financing series of US & Canadian software companies. [1] By looking at the cumulative rounds since 2010, we can see that Seed, A, & B volumes all trended meaningfully above their predicted counts.

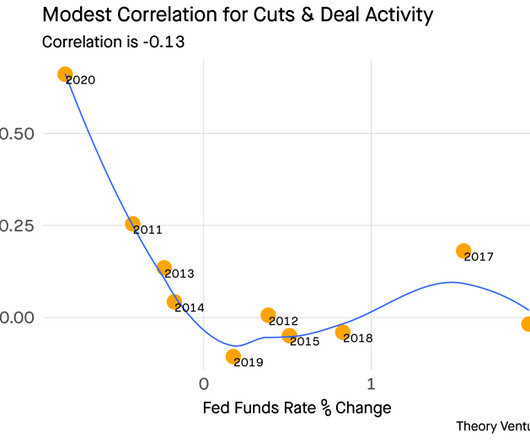

1 I’m using PitchBook US venture backed software exit data & running Spearman correlations on data from 2010-2020 on the subsequent year’s change in the relevant field. But there is some evidence within the data that laxer monetary policy will increase exit activity in the subsequent twelve months.

Circa 2010, there was only one full-time analyst at the company working on data, and his laptop was effectively the company’s data warehouse. Oh, Revenue_new is the old column. The company moved to customer_revenue last quarter when we hired a new VP of Finance and they updated the definition. Airbnb faced this problem, too.

SproutSocial was founded in 2010. It’s not your valuation today that matters. It’s where you can grow into, in SaaS. Also a reminder that power laws are everywhere in SaaS. Nine years layer, it was worth $815m — impressive. But then 2 years after that, they are worth $4.7B. Keep going in SaaS. Value compounds.

Big Bet #1: Cast Your Net Wide — Bet On Inbound While Going Global Freshworks was founded in October 2010 in Chennai, India. Big Bet #2: Find Tomorrow’s Great Anglers — Hire Talent With A Learning Mindset In 2010 and 2011, San Francisco was the place for SaaS talent. It helped them get funding in the first round.

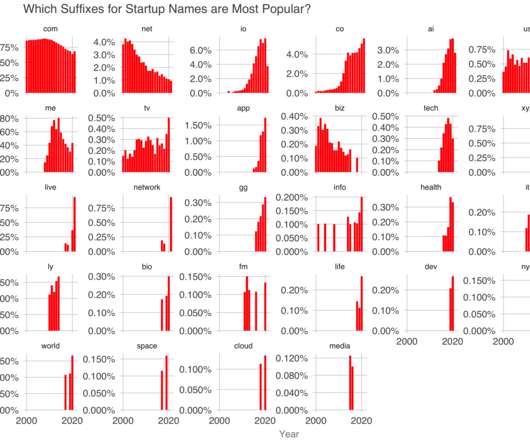

Appearing suddenly in 2010, it promptly disappeared - confoundingly abruptly and surprisingly unexpectedly - in 2015 - albeit, justly in my view. ” As a SaaS investor, these businesses aren’t in my bailiwick, but since.gg suffix certainly is in yours. polyptoton). killing Hemingway softly).

The best of us kept growing , albeit with elevated churn through 2010: What Really Happened to SaaS in the ’08-’09 Recession And to those of us who have been doing SaaS a long time … 2023 just feels Like it Used to Be. SaaS markets had fully recovered later that year. Back when you needed CFO approval on a bigger deal.

2018 observed the fewest number of angel-led financing rounds since before 2010. Angel investing was an important part of the Startupland ecosystem. Today, you can’t make the same argument. Angels led 156 rounds last year, a figure that collapsed from 714 in 2015.

Founded back in 2010, it had steady growth to $100m ARR, IPO’d quietly in 2019, then has grown 30%+ annually every year since. So sometimes steady and even is the right path. SproutSocial is one of those. That’s compounded to $360m in ARR today, and a market cap of $3.4 Billion, so about 9x ARR.

2010: Ease-of-Use. By 2010, we were finally started to get to basic feature parity. If you haven’t localized an app before, and didn’t architect it that way from the beginning, it’s a big project. We won Google, Facebook, Twitter, and so many other deals just with this feature. Phew, a long time!

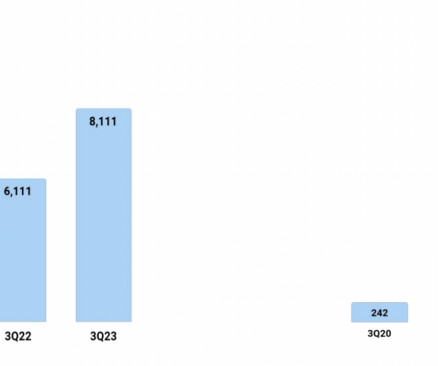

The chart above depicts the total disclosed value of US venture-backed SaaS startups which have been acquired by PE firms since 2010. The median venture-backed SaaS acquisition by PE has increased to $250M, up from $50M in 2010. Private equity hasn’t been a common exit route for venture backed startups in the past.

A Good Day: Dec 31, 2009; Dec 31, 2010; Dec 31, 2011; Dec 31, 2012. A Bad Day: When I Had No Salary And Didn’t Get My Requested $10k Bonus Even Though I Brought In an Extra $300k All-Cash Upfront Deal. And again, Dec 31, 2018 and Dec 31, 2019. When we killed it every year on the last day of the year. New Years was spent in the office.

Venture investing clocked more than $329b invested last year , up 10x since 2010. The rapid halving of software multiples has disjointed the valuations between public and private companies, and between growth and value companies.

The point is that SaaS multiples are still higher than where they were from 2010-2017. The Bear Case: Multiples are still elevated compared to the pre-2018 period. You can see a lot of VCs and others talking about this on Twitter. It just went nuts during Peak Covid. The argument here is that SaaS even in 2018 was overvalued.

Then GreenDot’s IPO in Q2 2010 at $1.4b Companies chewed gravel, gritting out each quarter. About 5 quarters later, the exit market offered a little sprig of hope. In Q4 2009, Amazon acquired Zappos for $1b. suggested the IPO market wasn’t icy. at $1.5b.

He was also awarded the 2010 Salesperson of the Year at the MIT Sales Conference. Prior to these roles, Mark was the founding CRO at HubSpot, where he scaled annualized revenue from $0 to $100 million and expanded his team from 1 to 450 employees. Mark was ranked #19 in Forbes’ Top 30 Social Sellers in the World.

2010: Ease-of-Use. By 2010, we were finally started to get to basic feature parity. If you haven’t localized an app before, and didn’t architect it that way from the beginning, it’s a big project. We won Google, Facebook, Twitter, and so many other deals just with this feature. Phew, a long time!

The book recounts five crashes: 1907, 1929, 1987, 2000, and 2010. I read Galbraith’s The Great Crash of 1929 and it’s good, but focuses only on a single event. A History of the United States in Five Crashes is the best I’ve found. So it doesn’t cover all US stock market crashes.

If we plot San Francisco startup fundraising activity through the first six months of the year, rounds A through D, beginning in 2010, we see the surge during the 2014-2015 heyday and then a reversion to an elevated mean in 2016 and 2017. Note, the levels still exceed 2010-2013. But the 50% decline is real.

In 2010, he joined DGF Investimentos, one of the top VC firms in Brazil. In 2010, he became one of the Co-Founders of Warehouse Investimentos, a prominent Brazilian VC company. In 2010, he founded Influitive, which helps B2B companies employ brand advocates for faster growth and development. His focus there was deal-sourcing.

In 2004 he became CEO of MarkLogic where he stayed until 2010. Dave Kellogg has a lengthy history in tech from his start in product marketing at Ingres Corp in 1985 to his ensuing leadership positions at Versant and Business Objects. Today he is an avid blogger on his personal blog “Kellblog” and sits on the boards of Alation and Nuxeo.

Professor Adam Grant wrote Emotional Intelligence is Overrated in 2010. A paper published in 2010 called Emotional intelligence: An integrative meta-analysis and cascading model accumulated the largest data set on emotional intelligence until that point. Professor Grant teaches at Wharton. Is this broadly true?

Deeper Bio: Early Life and Education Graduated with a Computer Science degree from The Academic College of Tel Aviv-Yaffo Demonstrated early interest in technology and software development Served in the Israeli Defense Forces’ Intelligence Corps, where he developed technical and leadership skills Early Career Began career as a software developer (..)

.” — Brian Halligan, co-founder and chairman of HubSpot “Secondary” liquidity for SaaS founders has been part of the VC toolkit for funding later stage SaaS founders since at least 2010-2011 or so. I got a significant offer as we approached $10m ARR back in the day at Adobe Sign / EchoSign — and I should have taken it.

Lucid launched in 2010 (before PLG was a term), and their team had an intense focus on product early on, so much so that the COO at the time read through hundreds of thousands of customer support tickets to hear directly from customers. As we know today, a strong product-led motion starts with a strong product.

Two Case Studies Scale Ventures invested in Box in 2010 while in the high-growth, low-burn bucket. In the later-stage venture market today, companies are rapidly trying to get to that gray box by lowering their spend, even though growth might take a hit. It means they’ll survive and maybe have a chance to move back up to the green box again.

2004-2010 marked the early days of SaaS where the model was still risky, and cloud providers were competing hard with their on-prem predecessors. . Because the SaaS model wasn’t entirely proven, venture capitalists took more risk, and expected a higher return. .

Looking for: – Microsoft visio 2010 manual pdf free. Microsoft visio 2010 manual pdf free. Microsoft visio 2010 manual pdf free.Beginner tutorial for Visio. Microsoft visio 2010 manual pdf free. The post Microsoft visio 2010 manual pdf free. Microsoft Visio 2010 in pdf first appeared on Natalie Luneva.

In 2010, COSS was valued at $10B, and 90% of that value was attributed to a single company: Red Hat. Open Source is one of the most successful enablers of global innovation in history, and Linux has grown into the most important software platform in the world, dominating every market it enters.

We organize all of the trending information in your field so you don't have to. Join 80,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content