This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The price for inference has massively plummeted this year, so you have more powerful models to build into your application, and they cost less every time you use them. Additionally, if you look at the mobile shift, the iPhone was released in 2007 but we didn’t get our first mobile apps like Uber and Snapchat until 2009 and 2010.

And it would be 4x the size of 2010. When demand exceeds supply, prices increase. And we know from a previous analysis that the public markets price high growth B2B companies at more aggressive prices than the private markets. Prices are higher, investment rounds larger, exits more valuable. Check check.

Let’s compare data from 2010 and 2021 to understand the longitudinal trends in cash and equity compensation. A VP of Engineering in a Bay Area startup that has raised less than twenty-five million dollars earned 33% more in 2021 than 2010. 2010 Equity. Cash Change. A nice bump. 2021 Equity. Equity Change. Owning 1.4%

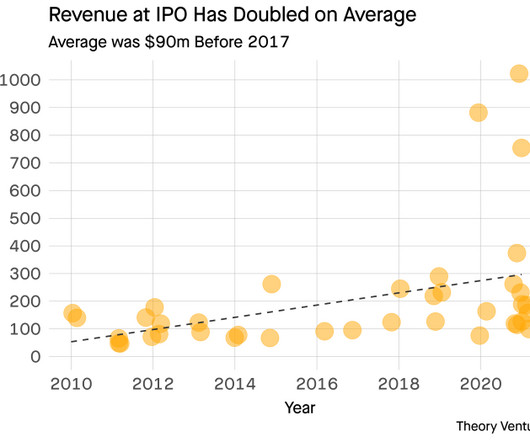

We gathered data on the US venture-backed software companies that went public between 2010 & today. Private market capital values companies at higher prices (from higher multiples) & is less expensive to raise. What does it take to go public? Has it changed over the last 15 years?

Company 2 compounds revenue at 83% the rate of company 1, but at half the price. The revenue trajectory mirrors company 3 at one-half the price. Venture investing clocked more than $329b invested last year , up 10x since 2010. Nine digits of hot money rushed into venture in the last two years, doubling prices.

Lucid launched in 2010 (before PLG was a term), and their team had an intense focus on product early on, so much so that the COO at the time read through hundreds of thousands of customer support tickets to hear directly from customers. Customers still needed simple pricing and seamless expansion.

When Patrick and John in 2010 were at Y Combinator and spend their days doing office hours with the whole Y Combinator and a little water in the valley. We look at annual churn, given the nature of those businesses that have annual or multi annual contracts with much bigger price items and tickets. Seven percent annual churn is good.

The chart above depicts the total disclosed value of US venture-backed SaaS startups which have been acquired by PE firms since 2010. The excess increases prices and valuation multiples for acquisition targets. The median venture-backed SaaS acquisition by PE has increased to $250M, up from $50M in 2010. The result?

.” — Brian Halligan, co-founder and chairman of HubSpot “Secondary” liquidity for SaaS founders has been part of the VC toolkit for funding later stage SaaS founders since at least 2010-2011 or so. And if the price they is selling is less than $100m pre, it sort of tells me they aren’t really building a Unicorn.

In 2010, he joined DGF Investimentos, one of the top VC firms in Brazil. In 2010, he became one of the Co-Founders of Warehouse Investimentos, a prominent Brazilian VC company. Campbell is probably one of the world’s foremost experts on pricing. Its focus is on businesses in Big Data, mobile, and SaaS.

The book recounts five crashes: 1907, 1929, 1987, 2000, and 2010. Technology companies of the era - the radio companies and the utility companies - traded at stratospheric multiples and endured nausea-inducing swings in their daily share prices ( SaaS ). A History of the United States in Five Crashes is the best I’ve found.

From 2010 until 2015, the SaaS world was becoming more complex with the introduction of static bundles and recurring revenue as an addition to the annual/monthly subscription model. We are seeing more agile packaging and pricing methods, dynamic deals, ramp-up revenue, and consumption and usage. Era 2, SaaS 2.0: Era 3, SaaS 3.0:

359: The Secrets to Vertical Growth, What it Really Takes to Build a $1B SaaS Company with Matt Garratt, SVP, Managing Partner @ Salesforce Ventures, Trisha Price, Chief Product Officer @ nCino and David Schmaier, CEO & Founder @ Vlocity. Trisha Price. Trisha Price: nCino is a little bit different in its background.

If we plot San Francisco startup fundraising activity through the first six months of the year, rounds A through D, beginning in 2010, we see the surge during the 2014-2015 heyday and then a reversion to an elevated mean in 2016 and 2017. Note, the levels still exceed 2010-2013. But the 50% decline is real.

If you don’t have tickets, lock in Early Bird pricing today and bring your team! About 2010, we started a completely different product line. I will really understand, “What is the price I want for my product?” I get to set the price of the apples, because they’re my apples. Get tickets here. TRANSCRIPT

The typical SaaS company going public in the last three years has a 77% smaller average revenue per customer than companies in 2010 – 2011. When these newer cohorts of companies have gone public, they have roughly four times the number of customers paying one-fourth the price of their older brothers.

The problem is the software that makes them possible is usually priced for huge companies with deep pockets. And so you hope that companies price their software in a way that both makes it accessible and reflects the actual value you’re getting back. Our New Conversion-Based Pricing Plans Support Your Growth.

DataDog provides a very popular IT monitoring solution that has grown from its founding in 2010 to a huge business. DataDog is playing across price points. Recently, we’ve seen a series of product-driven companies building huge customer bases with tremendous account expansion and terrific sales efficiency.

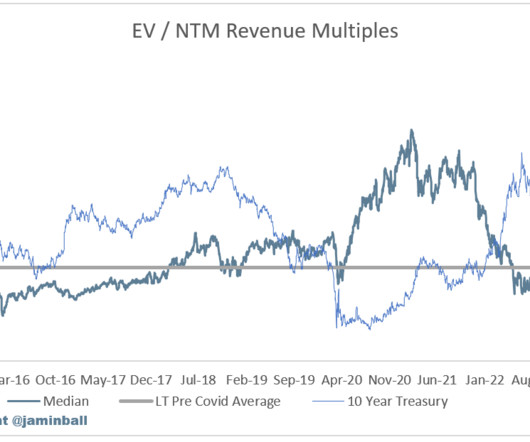

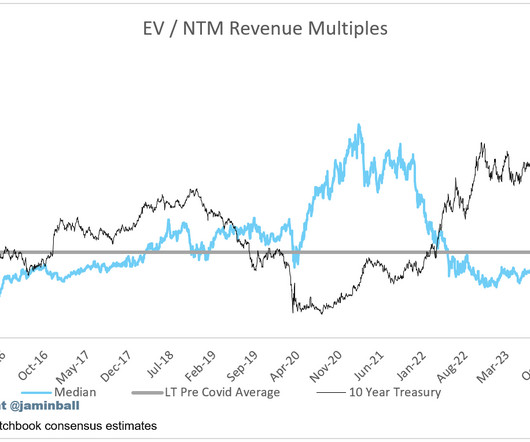

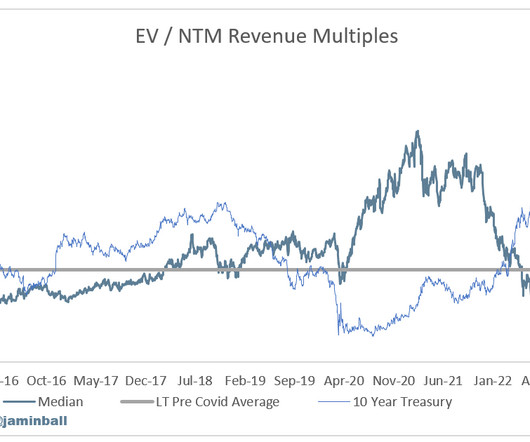

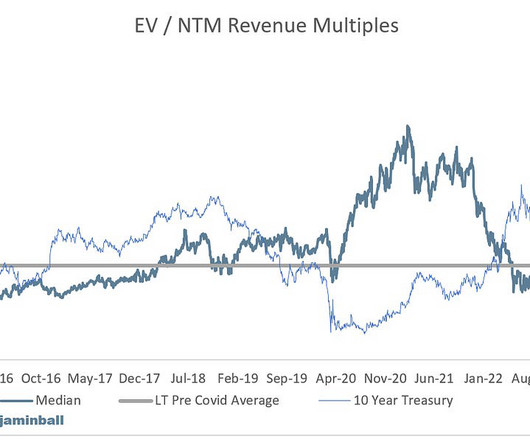

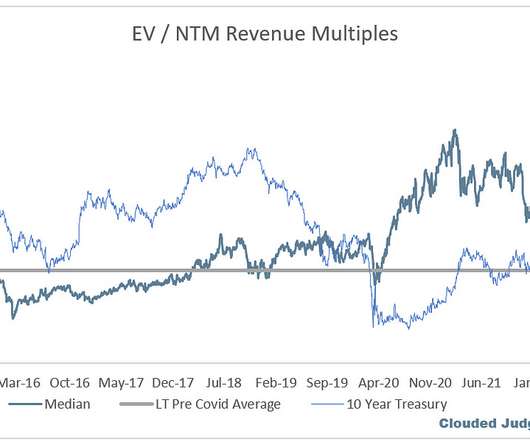

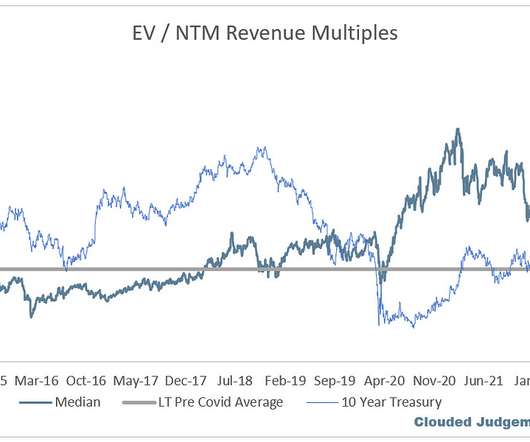

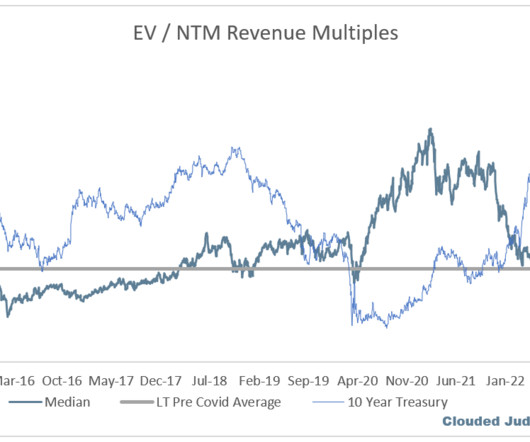

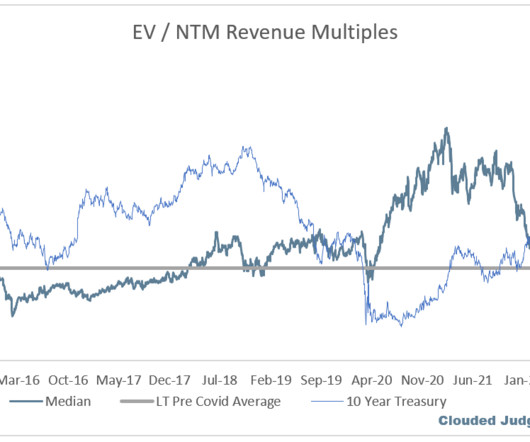

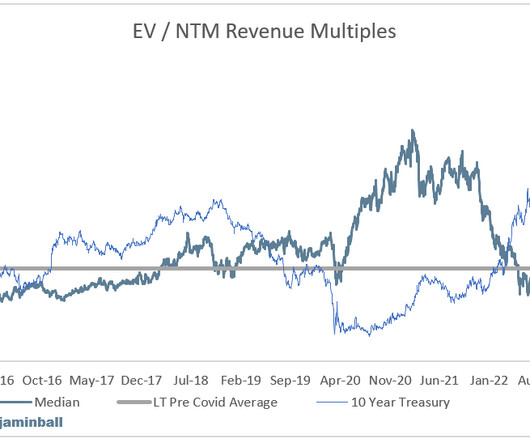

As a reminder - the average software multiple from 2010-2020 was ~7.8x, and the average 10Y over that same period was ~2.3%. Seems like something has to give… Either software valuations need to fall to more appropriately price in the discount rate, or rates need to fall. The current median multiple is ~5.7x.

Microsoft launched Azure in 2010, and Google launched GCP to the public in 2011 (they launched a preview of Google App Engine in 2008, but made it publicly available in 2011). On top of that- we HAVE seen significant pricing pressure. S3 has dropped nearly 97% in price, while EC2 has fallen nearly 90%!

Pass-through pricing Form of card processing pricing that allows the actual cost of processing (interchange, assessment, and processor fees) to be passed directly to the merchant; benefits of this pricing model include transparency and potentially lower costs when compared to discount rates.

For context on a 10Y at 5% - from 2010 to 2020 the 10Y averaged roughly ~2.5%. Said another way, the 10Y today is double what it averaged from 2010 to 2020. In general economic data has continued to come in strong (a data point suggesting inflation could stay sticky, and the economy can absorb rates staying higher for longer).

The story you tell to the market, the competitive moats you build, the pricing models fueling your growth – everything that got you to where you are needs to be reimagined for your new buyer. When Eren Bali founded Udemy in 2010, he had a vision for what the marketplace would be: a place where anyone could teach and learn anything.

The company went public in 2010, three years after competitor Blackstone did, which is captured in the book King of Capital. 2 1 I’m using price-to-book multiple in this analysis. APO Apollo Global Management 76 1.55 CG The Carlyle Group 16 3.85 TPG TPG Inc. ARES Ares Management Corp.

Continuing my little 2010 portfolio review ( here's part 1 ), the next stop after San Francisco ( Zendesk ), Vancouver ( Clio ) and Berlin ( Momox ) is Edinburgh, home of FreeAgent Central. And there's more to come. Konnichi wa , myGengo.

The median projected growth rate today is 14% The piece left out of the analysis is interest rates, which are obviously higher today than the period of 2010 to 2020. Wrapping all of this up, it appears that the market is either “pricing in” forward estimates coming up in 2024, or a big drop in rates (or both).

We’re also happy to share a more sustainable way of providing this information — our new transparent pricing dashboard. Another important detail to note is how Average Sales Price (ASP) and Expenses have changed over time. Our Average Sale Price (ASP) in 2014 was $13, while our total Operating Costs were $3,575,897.

As a reminder - from 2010 - 2020 the average 10Y rate was ~2.3%. That was more broadly a period of ZIRP, and it’s interesting that today the 10Y isn’t hugely different from where it was in the period of 2010 - 2020 Morgan Stanley CIO Survey Everyone is eagerly awaiting 2023 forecasts to be “de-risked.”

As the chart above shows, the total number of venture-backed acquisitions, in red, has exceeded the 14 year average (gray dashed line), every year since 2010. In 2014, acquirers will reveal the price of their acquisition 30% of the time. The bar chart above shows the fraction of startup acquisitions with undisclosed prices.

And to get ahead of some questions, the long term average I’m using is from 2010-2020 (so excluding the crazy multiples of Covid). The average 10Y in the period of 2010 - 2020 was ~2.3%. I don’t think it goes back to ZIRP, but I think it looks closer to the average from 2010 - 2020 than what it does today.

Said another way, the median NTM revenue multiple is ~23% below it’s historical average, but forward growth expectations are the lowest ever (~40% below historical average), and the 10Y is ~40% higher than it’s historical average (from the period 2010-2020). Clearly this is what the market is pricing in.

The choice they have is to pass those price increases back on to the consumer (who appears to be getting much weaker), or take margin hits. It makes sense the median multiple today is lower than the 2010-2020 average given the difference in rates. Either way, the situation seems less rosy than the beginning of year data suggested.

To answer the question, I’ve prepared three charts used Crunchbase data and focused on the seven states with more than 20 acquisitions since 2010. There is no statistically significant difference between the acquisition prices across any of these states to better than 95% confidence.

Unlike later rounds, Series A pricing has no correlation to MRR or next-twelve-months (NTM) revenue, which is a proxy for growth rate. This lack of a relationship indicates the Series A market pricing is more of a function of supply and demand and the ability of the founders to engender an active auction, than a mark-to-market pricing event.

In 2017, there will be a lot of comparison between the prices public bound companies fetch at IPO compared to the last round private valuations as the public window opens. Seed rounds have seen the greatest growth since 2010 from approximately 1000 rounds per year to more than 4000 rounds per year in 2014. In 2010, there were 1.4

She was Trello ’s very first sales hire in 2010, built the company’s sales and account management teams, and was instrumental in scaling its business from 5 million to 25 million users within two years. But if anyone knows how to walk this tightrope and make it to the other side, it’s Kristen Habacht.

In addition to increasing labor costs, startups in San Francisco are facing monotonically increasing real estate prices. Rising prices reflect an increase of demand. Total vacancy rate has dropped to 8% from a high in 2010 a 17.1%, meaning only 8% of available spaces are available to be rented.

This growth adjusted premium also comes at a time when the 10Y is nearly double what it was from 2010 to 2020. So what’s holding up software stocks valuations?? We can revisit this statement when macro pressures ease or rates change. Revenue multiples are a shorthand valuation framework.

In May 2010, I bet a good friend of mine that Android would overtake iOS in total devices shipments in 12 months' time. So have the Motorola Droid phones which have similar price points to the iPhone. In fact, Apple has a mobile product at every $50 price point between $0 and $850. My prediction was completely off the mark.

Founded: 2010. Founded: 2010. Grab a ticket before March 5th when prices increase. Singtel Innov8 invests in businesses developing new solutions in network capabilities, next generation devices, digital services and customer experience enhancement. Size of fund: $250M. Stage: Corporate Venture Capital. Size of fund: $57.5M.

ServiceNow commands 30%+ annual price increases from its customers, an impressive figure. And in fact, ServiceNow has generated positive operating cash flow for every year but 2010. In addition, the company has grown its base of customers substantially. ServiceNow reports its upsell rate, which is equivalent to a negative net churn.

Segment CEO and Co-founder Peter Reinhardt was recently reflecting on what were his top lessons learned from changing packages and pricing. While Segment may be an extreme case, the business is far from unique in learning that it was leaving money on the table due to its pricing. Pricing Is Your Best Shot at Growing 25% Faster.

What’s the price difference? What do you get for the price? What’s the price per profile? Sprout Social's cheapest plan, priced at $249 per month, restricts users to connecting only five social profiles. In contrast, Sprout Social's cheapest " Standard " plan begins at $249 per month.

I plotted the mean round size of Series As from 2010-2016 in the bar chart above. Greater competition in June and November drives greater prices and larger round sizes. Are there more prosperous months to raise than others? That’s a simple question to answer - or so I thought. Also in December?

We organize all of the trending information in your field so you don't have to. Join 80,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content