This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

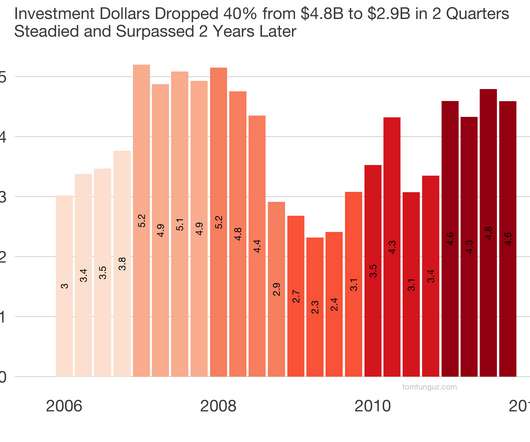

The market bounced back to similar levels once in Q2 2010, but needed eight quarters to return to its previous volumes. Let’s break down the trends by series. The Series B market had a nice resurgence as well, followed by a retrenchment in late 2010 and then another surge. in the quarters following the crash.

In 2010, classic SaaS was booming, the benefits of a subscription model were finally becoming clear to the public markets and the mass-market. The chart above breaks out 14 different software categories and shows the amount of dollars invested in each category indexed to 2010 levels.

Let’s compare data from 2010 and 2021 to understand the longitudinal trends in cash and equity compensation. A VP of Engineering in a Bay Area startup that has raised less than twenty-five million dollars earned 33% more in 2021 than 2010. 2010 Equity. Cash Change. A nice bump. 2021 Equity. Equity Change.

In 2010, one venture dollar bought $1.24 If we look at the ROIC across IPOs across the last 12 years or so, we see that same initial dynamic of incredibly efficient companies in the 2010 and 2014 IPO cohorts. It’s tripled from about $92m to more than $300M since 2010. One venture dollar bought forty-two cents at IPO.

The top left chart shows a $1M round had about 41% market share in 2010; that grew to about 54% in 2014; now it has fallen to 35%. But is now at the same level it was in 2010. In 2010, it was very likely that a business raised a $1M round before raising a $3-5M dollar round. The $3M round has suffered a similar loss of share.

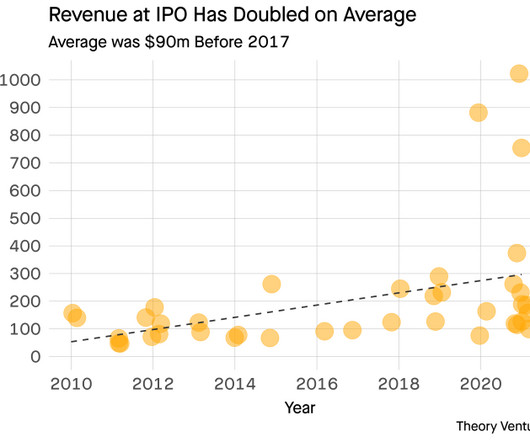

We gathered data on the US venture-backed software companies that went public between 2010 & today. which will further underscore the trend. What does it take to go public? Has it changed over the last 15 years? We corrected the trailing 12 months’ revenue at the time of IPO for inflation & plotted the data.

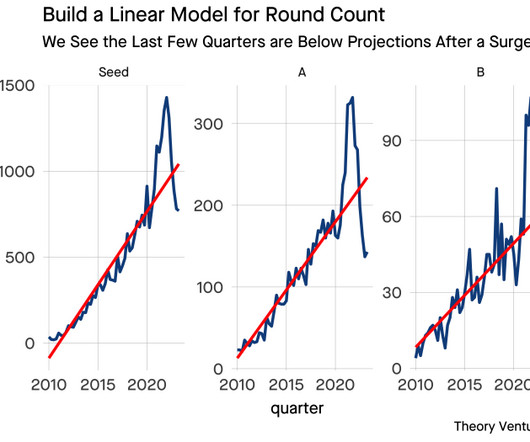

The red is a linear model based on data from 2010 to 2018 that predicts activity rates for each financing series of US & Canadian software companies. [1] By looking at the cumulative rounds since 2010, we can see that Seed, A, & B volumes all trended meaningfully above their predicted counts. But the gap is narrowing.

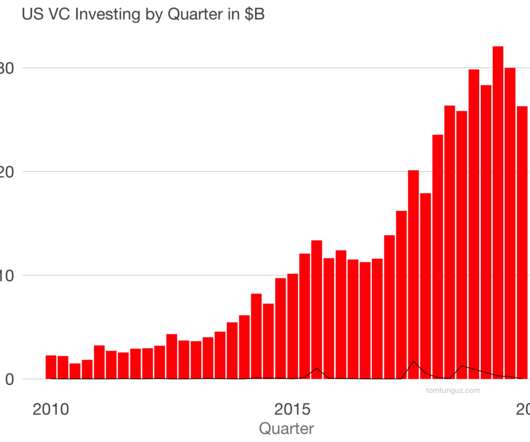

However, Q4 2019 saw meaningful dip from Q3, but it's too early to say whether it's an aberration, or the beginning of a longer-term trend. Since 2010, the number of round by quarter has followed a periodic growth, with consistent seasonality. Mean round sizes have increased from 5 million in 2010 to 17.5

2018 observed the fewest number of angel-led financing rounds since before 2010. Institutional seed funds might respond to this trend by writing bigger checks, raising bigger funds, raising opportunity funds or concentrating their portfolios. Angel investing was an important part of the Startupland ecosystem.

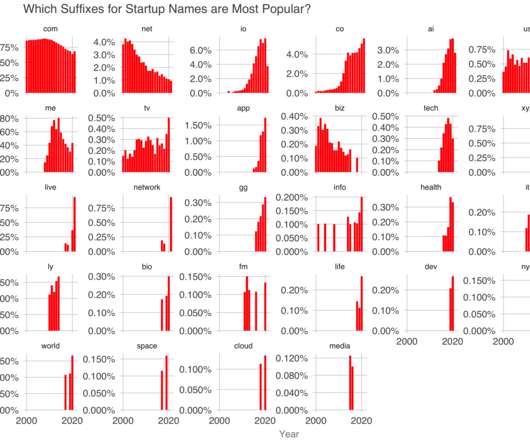

Appearing suddenly in 2010, it promptly disappeared - confoundingly abruptly and surprisingly unexpectedly - in 2015 - albeit, justly in my view. Aside from highlighting some of the trends in startup domain name preferences, this post has another motivation. killing Hemingway softly).

Big Bet #1: Cast Your Net Wide — Bet On Inbound While Going Global Freshworks was founded in October 2010 in Chennai, India. Big Bet #2: Find Tomorrow’s Great Anglers — Hire Talent With A Learning Mindset In 2010 and 2011, San Francisco was the place for SaaS talent. It helped them get funding in the first round.

I was curious about the drivers of these trends, so I ran my own analysis. If we plot San Francisco startup fundraising activity through the first six months of the year, rounds A through D, beginning in 2010, we see the surge during the 2014-2015 heyday and then a reversion to an elevated mean in 2016 and 2017.

Given this state of affairs, it’s a good time to take stock of the major trends in the startup market. As the chart above shows, the total number of venture-backed acquisitions, in red, has exceeded the 14 year average (gray dashed line), every year since 2010. Let’s dig a bit deeper into each one of them.

Year 2010 2011 2012 2013 2014. Q2 2010, Q2 2011 and Q2 2012 all saw similar drops before the levels rebounded. In 2010, the median was in the $3-4M range. Instead of acquiring companies after the Series A, as they did in 2010 and 2011, these corp dev groups are pursuing talented companies after the seed.

See an updated version of this post: Trends in the Startup Acquisition Market in 2015. In particular, how the number and value of startup acquisitions has changed, and more specifically, whether there are any trends in the sizes of acquisitions. I was curious how the strength of the IPO market has impacted the acquisition market.

Two Case Studies Scale Ventures invested in Box in 2010 while in the high-growth, low-burn bucket. Growth trends are returning to normal from post-pandemic peaks. In the later-stage venture market today, companies are rapidly trying to get to that gray box by lowering their spend, even though growth might take a hit.

In January 2010, Andrew Parker wrote a post called the Spawn of Craigslist. Nevertheless, the universe of opportunities for unbundling Excel is enormous, and a big trend in workflow software. Andrew identified companies that had built businesses by unbundling Craigslist. The vacation rentals link gave rise to AirBnB and HomeAway.

2010 101 4.5 From this table, we can identify five key trends: The number of SaaS IPOs has more than doubled in the past 12 years. IPO Cohort Median VC$ Raised Median # of Rounds Median Round Size $M Median IPO Size Number. 1998 42 2.5 2002 71 3.0 2006 66 4.0

It took a few years – which shows how much ahead of its time 37signals was – but eventually other SaaS companies redesigned their websites or rebuilt them from the ground up: Campaign Monitor in 2008 (click for a larger version) The trend was clear: Less and less text, bigger font sizes, larger images, videos.

The chart above shows the compound annual growth rate of venture investment rounds A through D in ten fastest growing venture markets plus the US from 2010-2016. Should that trend continue, in two years or sooner, the Chinese venture market will exceed the US in size. These inquiries made me wonder, how has the global market evolved?

This is resulting in several different and important trends. For now, though, the Series A market is the strongest its been since 2010. In the second quarter of 2018, there were three Series As for every five seeds. Startups benefit from the incredibly supportive financial environment.

Rewind The Clock — How Did We Get Here Most small businesses in pre-2010 didn’t have computers in their store or restaurant. This mentality has stayed around and has become a core part of running a business, and the trend will only grow. Most didn’t even have internet. Can you believe that? And then the iPhone changed everything.

In May 2010, I bet a good friend of mine that Android would overtake iOS in total devices shipments in 12 months' time. My prediction was completely off the mark. In May 2011, iOS led cumulative shipments by more than 100%: 191M to 95M. It would take another 10 months for Android to equal Apple in March 2011 at about 325M each.

DataDog provides a very popular IT monitoring solution that has grown from its founding in 2010 to a huge business. This has more to do with the trend that current IPOs tend to be around $200M and New Relic went public in 2014, when the median revenue at IPO was closer to $100M. DataDog is no exception. NewRelic filed with about $85M.

When Eren Bali founded Udemy in 2010, he had a vision for what the marketplace would be: a place where anyone could teach and learn anything. She’s also identified a much bigger trend happening in the world of work that plays to the business unit’s strengths. Turning a sales objection into a unique differentiator. We’re also B2B.

So it’s time for us all to put our ears to the ground and hear what the Mary Meeker report has to say about key trends that are currently shaping the digital world. At FastSpring, there were 9 key trends in the report that caught our eye. More and more companies are starting to realize the trend, too. Take note of the trends.

The GP metric trends from 100%+ to about 30% over about 15 years. For example, Workday charted the biggest GP figure in this data set of 189% in 2010 when the business grew from revenue by 252% and recorded net income of -57%. The chart above plots the median GP metric by years since founding. I’ve added a horizontal line at 40%.

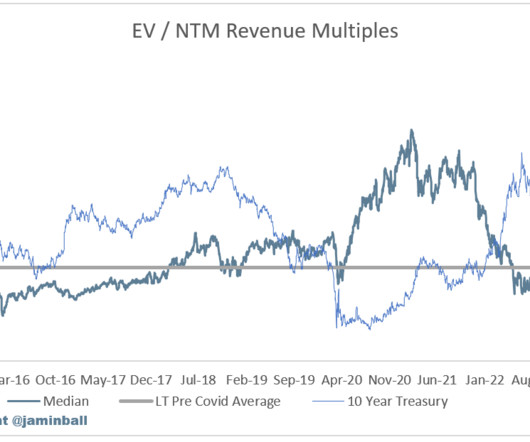

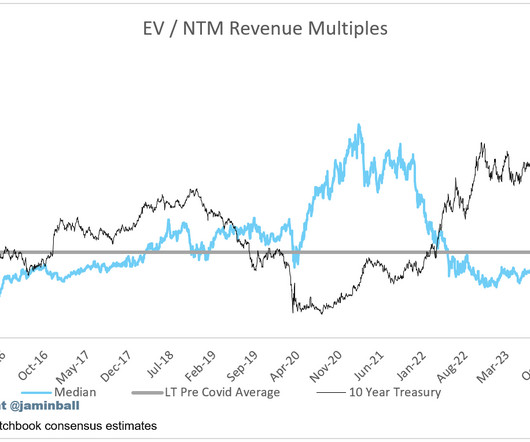

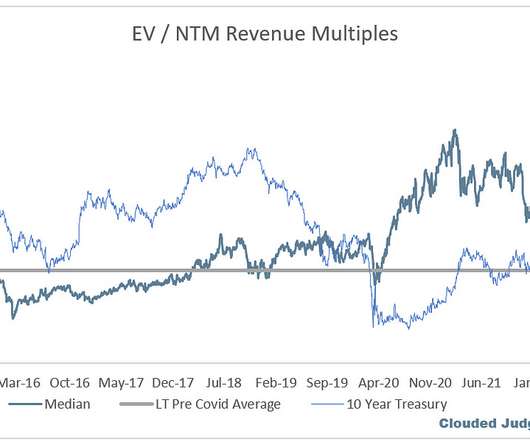

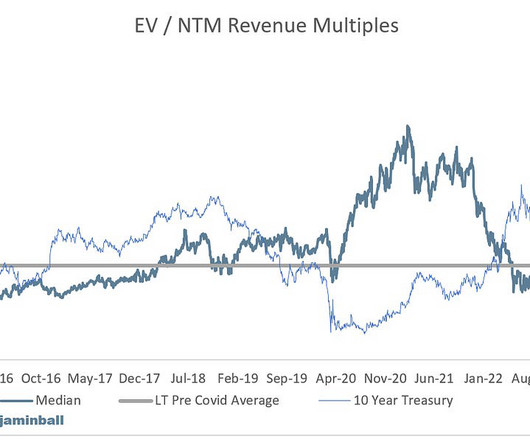

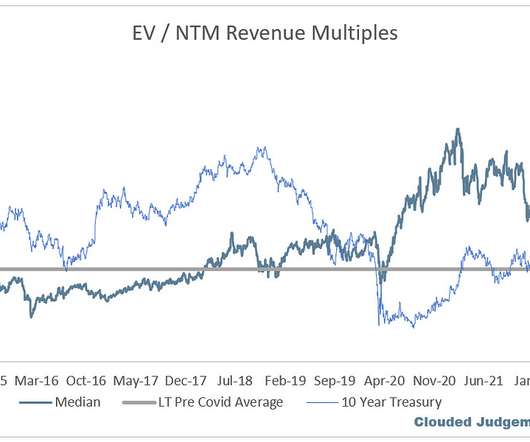

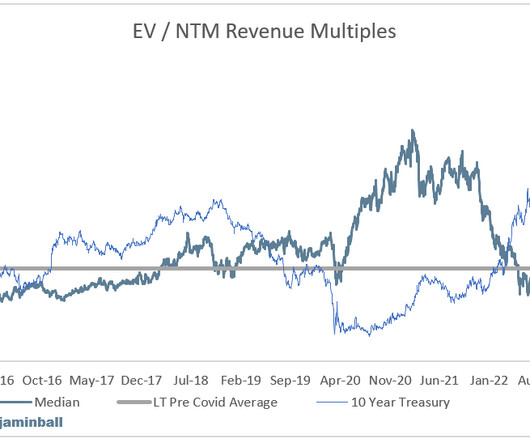

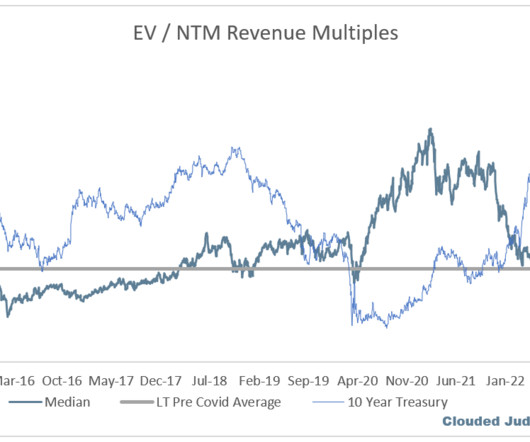

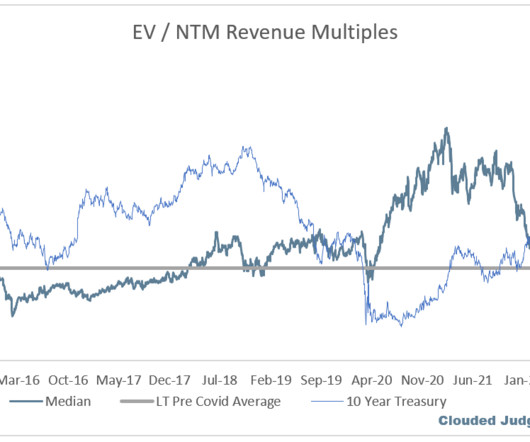

Every week I’ll provide updates on the latest trends in cloud software companies. For context on a 10Y at 5% - from 2010 to 2020 the 10Y averaged roughly ~2.5%. Said another way, the 10Y today is double what it averaged from 2010 to 2020. Follow along to stay up to date!

The chart above shows the sizes and frequency of hardware investment in the US since 2010 across different investment stages (Series A, B, C and Seed), using Crunchbase data. Each plot also shows a linear trend line for round sizes in gray. But do the data support the idea that the hardware ecosystem is as vibrant as it seems?

Every week I’ll provide updates on the latest trends in cloud software companies. As a reminder - the average software multiple from 2010-2020 was ~7.8x, and the average 10Y over that same period was ~2.3%. Follow along to stay up to date! ” messaging reverberates through the markets. Yesterday the 10Y hit 4.7%

About 2010, we started a completely different product line. If you take this ability to not follow the herd and the experience, you can spot trends. When you think about it, when a trend is early, everybody thinks you’re wrong. Peter : Long term, you go back the last 1,000 years, that has been the trend.

Every week I’ll provide updates on the latest trends in cloud software companies. Microsoft launched Azure in 2010, and Google launched GCP to the public in 2011 (they launched a preview of Google App Engine in 2008, but made it publicly available in 2011). Follow along to stay up to date!

Given that trend, I wondered if there is there any truth to the idea that startups today require less capital than before to succeed. The line chart above shows the trend across the four different IPO cohorts from 1998-2014. The trend is more pronounced in the average metric which grew from 0.822 2.0

Every week I’ll provide updates on the latest trends in cloud software companies. As a reminder - from 2010 - 2020 the average 10Y rate was ~2.3%. The average yearly growth in IT budgets from 2010 - 2019 was 4.1%, so the projections for 2023 are below the historical yearly average. Follow along to stay up to date!

Every week I’ll provide updates on the latest trends in cloud software companies. The median projected growth rate today is 14% The piece left out of the analysis is interest rates, which are obviously higher today than the period of 2010 to 2020. Follow along to stay up to date!

Every week I’ll provide updates on the latest trends in cloud software companies. And to get ahead of some questions, the long term average I’m using is from 2010-2020 (so excluding the crazy multiples of Covid). The average 10Y in the period of 2010 - 2020 was ~2.3%. Follow along to stay up to date!

How much of this trend is due to greater participation of venture capitalists investing in the seed market? Both types of rounds have increased by about 5x since 2010. The median seed round with VCs has increased from a median of $800k in 2010 to $2.1M The chart above plots the number of seeds rounds by year. in 2016 Q1.

The chart above shows the share of market cap commanded by companies which went public in three different decades: the Nineties, the Dotcom era (2000-2010), and the Cloud era (2010-2020). This trend is inexorable. Which era of companies drive this growth? Decade Count Average MC, $B Total, $T Share. Legacy 114 18.9

Every week I’ll provide updates on the latest trends in cloud software companies. This growth adjusted premium also comes at a time when the 10Y is nearly double what it was from 2010 to 2020. Follow along to stay up to date! Already we’ve seen huge earnings move. So what’s holding up software stocks valuations??

Every week I’ll provide updates on the latest trends in cloud software companies. I’m using the period of 2010+ given that’s really when cloud software came about. Follow along to stay up to date! The WCLD index is up 30%! The Nasdaq is up 12%. Given this move, where do multiples stand today?

Every week I’ll provide updates on the latest trends in cloud software companies. So today, the median multiple is ~25% lower than where it’s longer term average (pre 2010 we don’t have much data on cloud software multiples as there weren’t many public cloud software companies). Follow along to stay up to date!

Using Crunchbase data, I analyzed share of dollars commanded by each of these 16 categories over the last five years to understand the trends in both the seed and series A fundraising markets. Big Data, a term popularized in 2012 that has reached its apogee in 2015 according to Google trends increased from 2.5%

We know cost efficiencies are’t the driver behind these trends. In 2010, SaaS companies as a whole began investing more to grow faster and in the past three years, average growth rates have risen to about 35%. Older and younger companies are fetching these huge multiples indicating the valuation increase trend is broad.

We organize all of the trending information in your field so you don't have to. Join 80,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content