This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

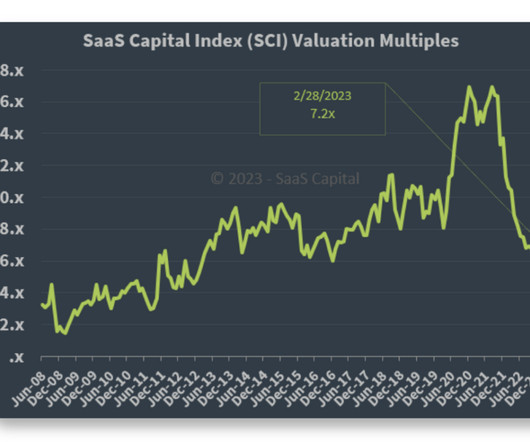

That’s when SaaS revenue multiples fell back to 6x, the lowest rate since 2013. I did a deeper dive on SaaS multiples, and what that means for founders and SaaS execs, below at SaaStr APAC: The post The Three Valuation Lows in SaaS: 2013, 2016, and 2022 appeared first on SaaStr. But we’ll see.

And a related SaaStr great deep dive with Parker Conrad, founder CEO of Rippling, here: The post The SaaS Era of 2013-2022 is Over. For often the same deal and deal size. Step up — or step aside. Welcome to The World of Hyperfunctional SaaS. appeared first on SaaStr.

In fact, in 90% of SaaS IPOs, the founder CEO is still the CEO at IPO: SaaS CEOs That Go The Distance, To IPO … Tend To Be Founder-CEOs (Updated) Of all the investments Ive made since 2013 , in only 1 have the VCs replaced the CEO. And in that case, one, I opposed it (I didnt have a vote).

The post Leadership Learnings: 5 Things I Wish I Could Have Told My 2013 Self With Advisor and Former CTO of Heap Dan Robinson (Pod 663 + Video) appeared first on SaaStr. Experienced leaders bring pattern recognition, problem-solving playbooks, and credibility to your company.

Think your customers will pay more for data visualizations in your application? Five years ago they may have. But today, dashboards and visualizations have become table stakes. Discover which features will differentiate your application and maximize the ROI of your embedded analytics. Brought to you by Logi Analytics.

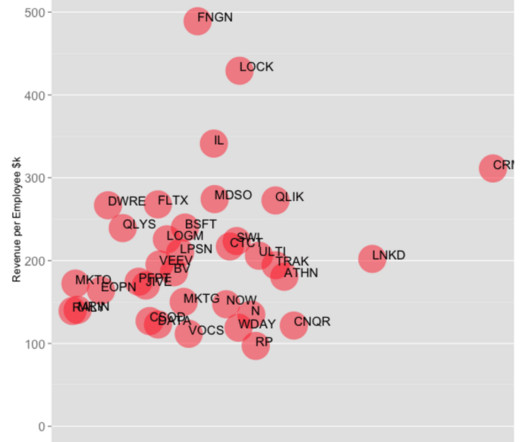

Compare that to the benchmarks in 2013! In 2013, the average revenue per employee of these companies totaled $200k. Company RPE 2013, $k RPE 2023, $k CAGR CRM 325 375 1.4% Both these companies also focus on enterprise accounts - in contrast to Bill.com at the bottom, which targets small businesses. VEEV 200 880 15.9%

since 2013. SaaS and Cloud are up +1000% since 2013. We’ve used various bits of the BVP Nasdaq Index and metrics since they launched a few years ago to highlight trends in SaaS and Cloud. This week even after a pullback, public SaaS and Cloud companies are up an eve 1000% (!) But does it even matter?

Early businesses tend to create more instruments to hire, grow, and incentivize. tokens resemble equity in most ways, but possess one additional function: they can be used to pay for service. Trailing 2 Year Inflation Rate. Founded Year.

Wildly Profitable — And Profitable Since 2013. The Trade Desk was founded in 2009 and began to take off in 2012. By 2013, it was profitable and never looked back. Top-tier growth + top tier profits beats Insane Growth in today’s world. As perhaps it always should have. #2. Today, it’s insanely profitable.

So I’ve been investing since 2013, and have done fairly well. Some of my top investments at seed stage include Pipedrive, Salesloft, Front, Talkdesk, Algolia, Gorgias, Greenhouse and more: But 2022 was a quiet time. My first year with no brand new investments, only follow-ons. So we’re behind.

The reliance on business messaging apps really took off when Slack joined the market in 2013 and introduced a highly efficient means. The post Microsoft Teams Vs. Slack appeared first on The Daily Egg.

Marketo IPO’s in 2013 at $700m market cap. 2013: first investment. And yes, no one could have predicted the run we’ve seen in Cloud in the past few years. But take a look at these examples: Marketo (and Hubspot): Founded 2006. Vista buys Marketo for $1.8B A little more than 2 years later, it was resold for $4.75B to Adobe.

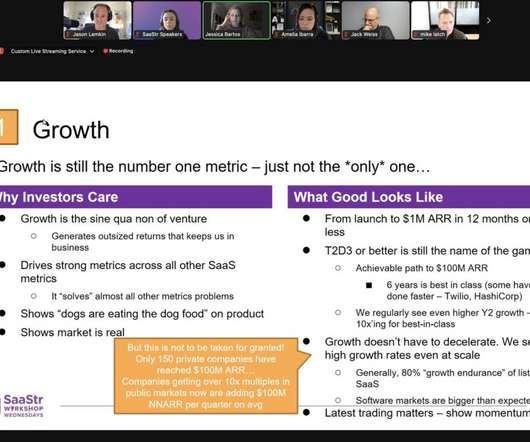

In the latest SaaStr Workshop Wednesday (sign up for FREE here ), Jessica Bartos of Salesforce Ventures did a great deep dive on the state of SaaS and venture in 2013. The full session is below and it’s a great watch. One metric stood out to me I hadn’t seen presented before: just how many private SaaS companies (i.e.,

At our first SaaStr event in 2013, some folks ask why we had a Mad Men-inspired theme. Well, you see this guy at the first SaaStr event, from 2013. And yet … I’d give it back and up in a heartbeat. You only get so many chances in life. In SaaS, revenue compounds. He’s thinking. He’s thinking on this question.

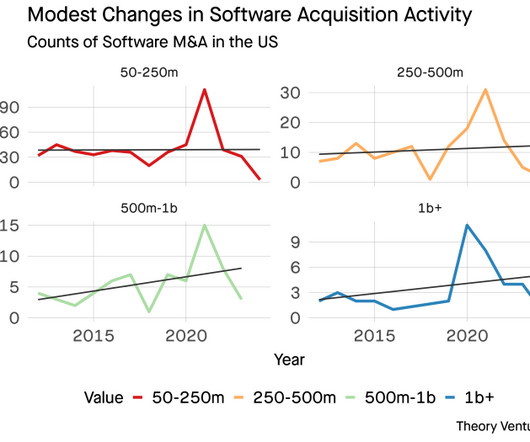

Year Share Good Year 2012 18.4% - 2013 25.9% - 2014 65.5% In 2014, 2016, 2020, 2021, these big mergers drove the figures into the tens of billions. It’s no surprise that in those years, the biggest acquisitions accounted for more than 53% of dollars on average. X 2015 20.1% - 2016 43.0% X 2019 23.4% - 2020 61.1% X 2021 43.8%

Shopify’s first quarter revenue: Q1 2021: $989 million Q1 2020: $470 million Q1 2019: $321 million Q1 2018: $214 million Q1 2017: $127 million Q1 2016: $73 million Q1 2015: $37 million Q1 2014: $19 million Q1 2013: $9 million. In fact, that’s what it was just back in 2013. — Jon Erlichman (@JonErlichman) April 28, 2021.

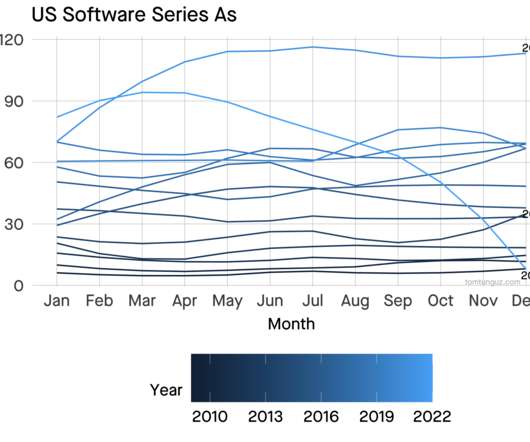

In 2013, the surge in June/July & December stand out. The answer is yes. The US software Series A market has become much less seasonal since that post in 2014. I’ve plotted the data above & smoothed it to clarify the patterns. Set that aside.

During the 2013-2014, median acquisition prices increased by 50% in less than a year, from $36m to $54m. This change in the exit market parallels a surge in acquihires in 2014 when corporate development departments began to acquire seed-stage companies for talent rather than waiting for Series A businesses.

Steady 14% Growth Since 2013 Has Grown Business From $1.3m And its stock price is up +35% the last year, and +192% the past 5 years: 5 Interesting Learnings: #1. About $1m Quotas for 5,000 Sales Reps Gartner is split into two divisions, and interestingly, both have quotas of about $1m per rep. #2.

In 2013, everyone that could come to the Bay Area to run a SaaS company, did. Atlassian, Adyen, Shopify and so many other leaders weren’t founded in the U.S., let alone the Bay Area. MongoDB, Datadog, and others have given New York a stronger and strong place in SaaS and Cloud. By 2018, it felt like about 50%.

In 2013 and 2015, the discipline’s merits dominated the conversation. A decade ago, Gainsight championed the creation of the customer success category. People curious and passionate about customer success convened at the Pulse conference to debate customer success.

The IPO in 2013 wasn’t an exit – it was just another milestone in building an enduring company. He led the company through its successful IPO in 2013, which was one of the most successful public offerings for an enterprise software company at that time. This focus turned customers into evangelists.

They started making that CRM bet way back in 2013 or so, maybe earlier. CRM is probably bigger than Marketing now (HubSpot doesn’t break it out anymore). If not, it will be soon. And HubSpot is still growing its new customer count > 20% at $2.5B

So when I started writing venture checks in 2013, I didn’t know what I was doing, but I had a strong start: First was Pipedrive co-leading seed, then acquired for $1.5B cash Second was Algolia leading U.S. Billion cash Fifth was Logikcull, acquired for $300m cash So it was a good start.

Back when I started investing, in 2013, VCs worked on getting acquihires for their struggling startups. Dear SaaStr: How Do Investors Feel About “Acquihires”? A lot of energy was put in to find a “soft landing” for struggling investments running out of money, even if the returns might be nickels on the dollars.

#1 source of traffic to [link] : 2022: SEO 2021: SEO 2020: SEO 2019: SEO 2018: SEO 2017: SEO 2016: SEO 2015: SEO 2014: SEO 2013: SEO 2012: SEO. Even Year 1 pic.twitter.com/5FtzBG2v1O. — Jason BeKind Lemkin #???????????? jasonlk) March 15, 2022. So we’re coming up on Year 10 for SaaStr!

One of the earliest posts I did on SaaStr was back in 2013 when I made my first venture investment, co-leading the seed round in Pipedrive. From 2013: I was asked on Quora why I recently invested in Pipedrive. But could be worth $10B by year 15 #itcompounds pic.twitter.com/qElNH78hl8. Most I quickly learned from.

Where it Went: IPO’d in 2013, hit $250m ARR by 2016, a cquired for $1.8b Where it Went: Acquired by Oracle in 2013 for $400m. in 2011 GAAP revenue. Where it Went: $233m+ in growth financing (at implicit valuation of $1B+) in 2021. #78 78 Marketo. in 2011 GAAP revenue. by Vista PE , and then Adobe for $4B+. #99 99 SugarSync.

Kyle’s foray into B2B tech sales started in 2013 when he joined Looker as the 6th employee. Not every conversation has to be a calendared meeting! #4. What’s your top “undiscovered gem” — an app you love but others may not have heard of? has been my best new tool.

He personally emailed every customer who canceled their Zoom subscription to understand their issues. This dedication to user experience helped shape Zoom into a more user-friendly platform than its competitors.

Zenefits was the hottest/fastest growing startup from 2013-2016. Either way, I’d pass on Been There, Done That. 1/ Want the best startup VP Sales candidates in the world? Here’s how to get the list of them. First, some context. We were valued at 4.5B

Launched in 2013, it has over 2000 employees and more than 60M active users. Canva started building collaborative design in 2013 and shipped it in 2020. Canva hit $1B in ARR at the end of last year. After a couple of years in building out Canva’s people functions, he is now investing in growing the company as a CMO.

The first one defined the Unicorn age in 2013, and the second one updated it in 2015. A few years back, Aileen Lee and Cowboy Ventures put out 2 seminal posts on TechCrunch about Unicorns. Many remember them just for data on Unicorns as they began to emerge from rare to seemingly everyday (100+ this year so far).

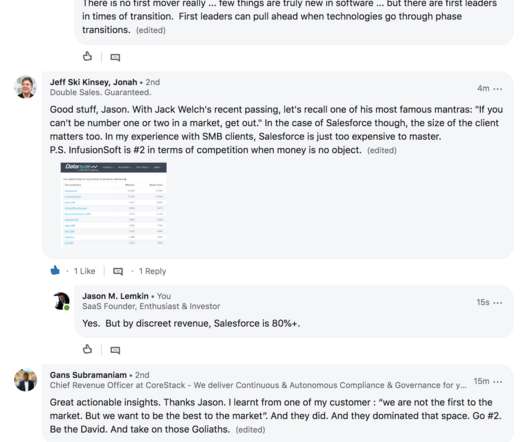

note: a 2020 update of a class 2013 post. And it eventually grows even faster downmarket … which #2 becomes well positioned to take advantage of. Just some thoughts. Again, I have no idea who is #2 to Salesforce in ondemand CRM. Sometimes, #1 does eat everything. But not always.

SaaStr 663: 9 Things I Wish I Would Have Told My 2013 Self: Lessons Learned from 9 Years with Heap’s Former CTO, Dan Robinson Top Videos This Week: 1. Scaling a SaaS Startup to $1B+ ARR: Insights from UiPath’s CEO and Founder 2.

SaaStr 663: 9 Things I Wish I Would Have Told My 2013 Self: Lessons Learned from 9 Years with Heap’s Former CTO, Dan Robinson 3. SaaStr 662: Things You Think as a First-Time Founder That Just Ain’t So With Lattice Co-Founder & CEO Jack Altman and SaaStr Founder & CEO Jason Lemkin 2.

SaaStr 663: 9 Things I Wish I Would Have Told My 2013 Self: Lessons Learned from 9 Years with Heap’s Former CTO, Dan Robinson 4. SaaStr 664: What You Need to Change at $10M to Scale to $100M with Sameer Dholakia, Partner at Bessemer Venture Partners 3.

Start with January 2013 and enter the number of new customers that you’ve acquired in that month. Then move to the right and enter how many of those January 2013 customers were still customers in February, March, April and so on. If your data goes further back than January 2013, extend the table accordingly.

SentinelOne was incorporated in January 2013. Which is slightly out of fashion in today’s world. #7. Pretty Much a Rocketship — Sentinel One is Just 10 Years Old, And Only in Market for 8 Years!

First up is RingCentral, which IPO’d relatively early and quietly in 2013. While companies that are about to go public get a lot of metrics analysis, we can perhaps learn even more interesting things from the quarterly reports and check-ins from various public SaaS companies after they’ve IPO’d.

[Update 12/20/2013: I have extended the dashboard to include multiple pricing tiers and annual subscription plans. Check it out here.] Update 01/17/2015: There's a new company called ChartMogul ( which we invested in ) which makes it easy to get a real-time dashboard similar to the template below. Check it out!

In 2013, Scott Berkun authored a book called The Year Without Pants. Scott shared his experience working remotely for Wordpress. After I read the book, I wrote : In the coming years, video conferencing and online meetings will become much more prevalent as stories like the ones Scott shares are told and retold.

Agricultural Technology (AgTech) boomed in 2013, but has not recovered after substantial drop from its one-year high. If those startups raised twice the amount of capital then the figure would be 2. Advertising technology has seen a resurgence in 2016, reversing a three year trend of declines.

Founded : 2013. Founded : 2013. Founded : 2013. Founded : 2013. Omie main goal is to bridge the efficiency gap in Brazilian SMB, helping customers to be more prosperous. Omie is the only SaaS company figuring among 100 fastest growing SMB in Brazil, according to Deloitte Consulting, ranking #3. CEO : Marcelo Lombardo.

We organize all of the trending information in your field so you don't have to. Join 80,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content