This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Everyone knew mobile commerce was exploding (from 15% in 2014 to 75% in 2024), but reaching customers on mobile was broken. CEO Amit Jhawar joined us at SaaStr Annual for a deep dive: 1. Solve The Hard Problem First And Patent It The first key insight? Attentive spent months with brands, consumers, and regulators to crack this.

It was started in 2014 when founders Daniel and Jonathan were working together at a delivery startup and experienced firsthand how slow background checks were slowing down worker onboarding. Checkr’s go-to-market strategy was already well-established when Lindsay joined in 2022.

Also, 2014 to 2016 saw a 57% reduction in multiples and of course after 2008. Cloud companies' fast growth multiplied by an appreciation in multiples has pushed valuations higher since 2014. Today, we’re in the midst of the fifth. But let’s look at the most recent five years. Correction Year.

With Ironclad’s journey from an AI-first concept in 2014 to a Series E+ company and a16z’s extensive portfolio view, their insights offer a valuable perspective on the current state of AI in SaaS. What’s Currently Working in AI for SaaS 1.

In 2014, when I invested in then up-and-comer Talkdesk , it had long since IPO’d and was struggling at a $200m market cap. Five9’s revenues were 60% enterprise at IPO in 2014, but now are 83% enterprise. And Five9 has grown from just 3 $1m ACV customers in 2014 to 91 today: #2. Five9 is particularly interesting.

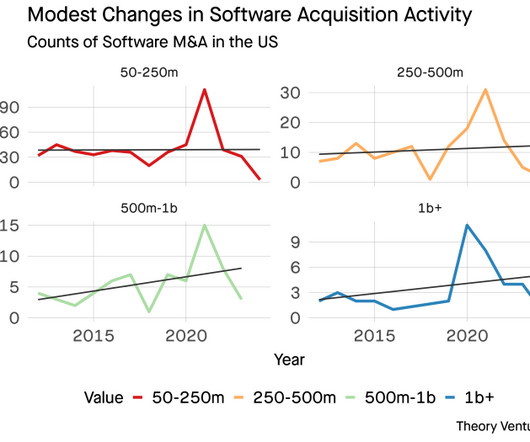

In 2014, 2016, 2020, 2021, these big mergers drove the figures into the tens of billions. Year Share Good Year 2012 18.4% - 2013 25.9% - 2014 65.5% Multi-billion dollar acquisitions, the blue bars, are the largest contributors to this swing. X 2015 20.1% - 2016 43.0% X 2019 23.4% - 2020 61.1% X 2021 43.8%

Sailpoint x Thoma Bravo story is incredible Sep 2014: Thoma Bravo acquires VC-backed Sailpoint Nov 2017: TB takes Sailpoint public at ~$1.1B Because it’s not just new names. It’s also dozens of SaaS companies that went private and will IPO again … a second time. valuation Apr 2022: TB takes Sailpoint private at $6.9B

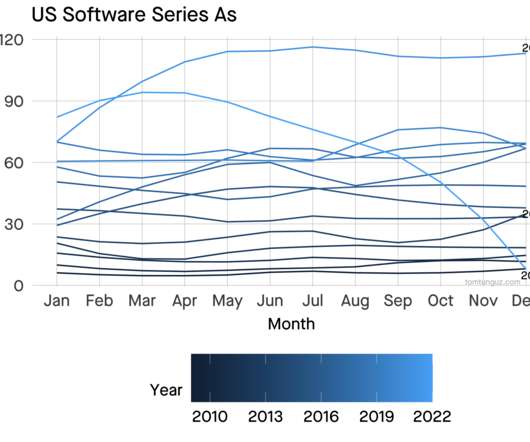

I set out to determine if fundraising seasonality had changed from this post I published in 2014 which suggested Q2 & Q4 were best for founders. The US software Series A market has become much less seasonal since that post in 2014. The answer is yes. I’ve plotted the data above & smoothed it to clarify the patterns.

This change in the exit market parallels a surge in acquihires in 2014 when corporate development departments began to acquire seed-stage companies for talent rather than waiting for Series A businesses. During the 2013-2014, median acquisition prices increased by 50% in less than a year, from $36m to $54m.

In 2014, Atiyah co-founded Parabus, a consumer-focused startup that automatically secured refunds when prices dropped on online purchases. At its peak, Parabus saved millions of dollars for its 10 million customers before being acquired by Capital One after just three years.

HubSpot is a great one that IPO’d way back in 2014 ?? HubSpot has gone global with a fury since 2014, driving from 22% international revenue to 40%. 5 Interesting Learnings from Slack at $700m in ARR. 5 Interesting Learnings from Zoom. As it IPOs. 5 Interesting Learnings from Bill.com’s IPO. With a $10k ACV. RingCentral ).

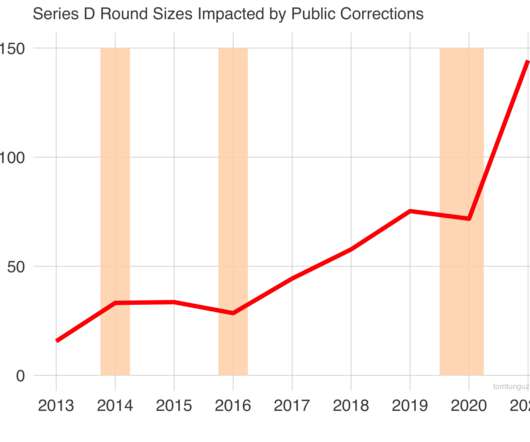

2014’s correction stalled and then reversed Series D round sizes for 2 years through the second correction in 2016. Three corrections in the last ten years have contracted multiples by 40% or more. These are marked in peachpuff orange rectangles above. The Series D mean round size is plotted in red.

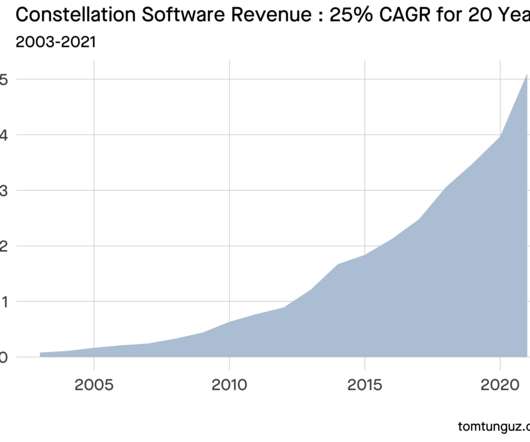

From 2003 to 2014, Constellation’s revenues compounded from $80m to more than $5b, an average of 25% annually. In 2014, Constellation grew revenues 40%, which today would place the company in the top quartile. But Constellation arrives at that growth in a very different way : they acquire to grow.

In 2014, I published a post called Do Startup Require Less Capital to Succeed than 10 Years Ago ? In 2014 we saw increasing efficiencies over time, which was very exciting because it reaffirmed the efficiency of SaaS go-to-market. It’s been five years and time to see how things have changed. The chart above updates that analysis.

It was March 2014. It’s a far cry from 20 people and sub-$100M valuation in 2014. The debate about partnering with Snowflake went back and forth during the investment committee meeting. My partners, Satish and John, had met the company and were proposing to lead the Series B. It grew 174% year on year at scale.

When I invested in Talkdesk in 2014, Five9 had a $150m market cap. That’s accelerated more Cloud leaders than it has harmed. It’s not just Zoom and Slack. Many other functions have quickly moved to the Cloud, e.g. call center like RingCentral and Five9. Today, six years later, it is $7 billion. Let that sink in a bit ??.

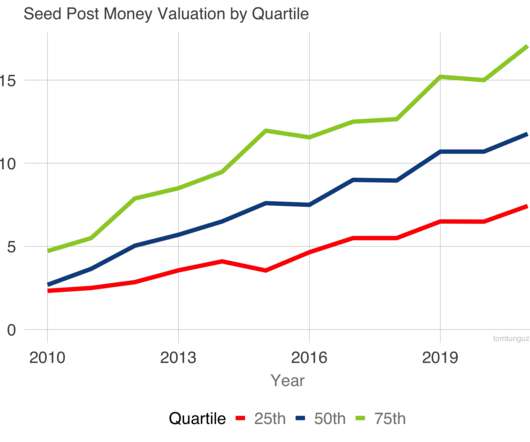

The top left chart shows a $1M round had about 41% market share in 2010; that grew to about 54% in 2014; now it has fallen to 35%. Today, the first institutional round of capital is that $3-5M in 54% of cases, up from 39% in 2014. These numbers would be more extreme if benchmarked to 2014. But something changed.

The company initially launched back in 2012 but didn’t officially acquire its first customers until two years later, in 2014. Monday.com has become one of the most popular project management solutions available. Today, 115,000+ organizations worldwide rely on Monday.com.

Which is that we have literally 100x more quality content than 2011-2014. Organic Search remains our #1 source of SaaStr readers for 13 years straight: But, I can also tell you what our data says. Our content page ranks remain high. And we’ve actually increased our output.

2014 $4.1B. It’s not slowing down Salesforce, Snowflake, or almost any other SaaS or Cloud leader. Salesforce Growth: 2023 $31.8B (guidance) 2022 $26.5B 2021 $21.25B 2020 $17.1B Thank you Ohana! pic.twitter.com/CMhrBXgHSF. — Marc Benioff (@Benioff) May 31, 2022. We may be headed for a big downturn, we’ll see.

First, the science of building SaaS companies is better understood today than in 2014. To be fair, 22% of companies raised at $0 in ARR. But the average MRR has increased substantially from the last time I analyzed the data. note I’m switching from median to average here). That’s quite a growth rate.

In 2014, it had 6 employees. Folks want to start startups because they have a chance to look like this: The true definition of a tech startup is probably one that if it truly achieves product-market fit, can scale almost infinitely. The above example is of my third venture investment, Talkdesk. Today, it has 2,000 employees and is worth $10B.

2014: Alibaba. If we plot the annual growth rates for the 75th percentile Series A, we observe the expansion in valuations occurs in fits and starts. 3 of the 11 years recorded 40%+ growth. 3 of the years saw declining prices. Perhaps these prices are tied to blockbuster IPO markets. 2012: Facebook.

Over time, rates decline and then in the 2012-2014 era, they begin to surge upward culminating 6-8 years later at the top-left of the chart and $200b+ invested. The y-axis tracks enture capital investment by year and the year of the data point resides in the reddish circle. Do you remember this shape from high school math?

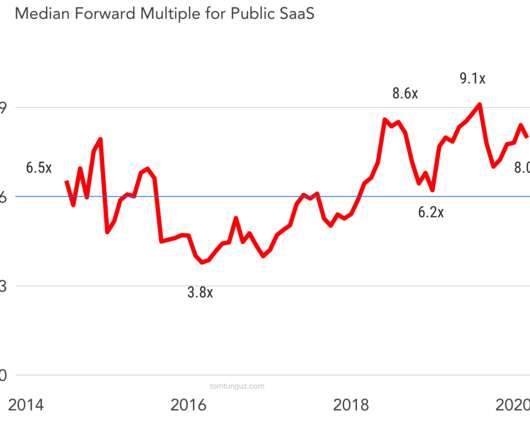

It includes a basket of all the next-generation software companies since 2014.* Let’s double-click on the impact of last week on the valuation environment. This is our familiar forward multiples chart. You will see that multiples are still meaningfully above the median of 6X which is the thin blue line.

Pretty incredible for a product that just launched in 2014. And that’s with direct and indirect competition from Asana, Atlassian, Clickup, Wrike, Smartsheet, Notion and so many others. 5 Interesting Learnings: #1. 121% NRR from 10+ seat customers, 107% overall, ~85% from smallest customers.

During the dotcom crash in 2001, the Global Financial Crisis of 2008, and the SaaS corrections in 2014, 2016, and 2018, Lee was either COO/CFO or CFO at Twilio, SAY Media, and Ofoto. Lee Kirkpatrick is no stranger to downturns.

VC in Algolia back in 2014, and it’s now a $2B+ search API giant. CEO of Algolia, Bernadette Nixon. First up was a walk-and-talk with one of my favorite CEOs, Bernadette Nixon of Aloglia. I was lucky enough to be the first U.S. Casey did a deep dive on the future of APIs and more here: 2. Jeff Yoshimura, CMO at Synk.

2014 $4.1B. Salesforce Growth: 2021 $20.8B Guidance 2020 $17.1B Thank you Ohana! — Marc Benioff (@Benioff) August 25, 2020. If you haven’t done a SaaS start-up before, it’s different. The reasons are many, but I think they can almost all be summed up in one key factor: SaaS compounds.

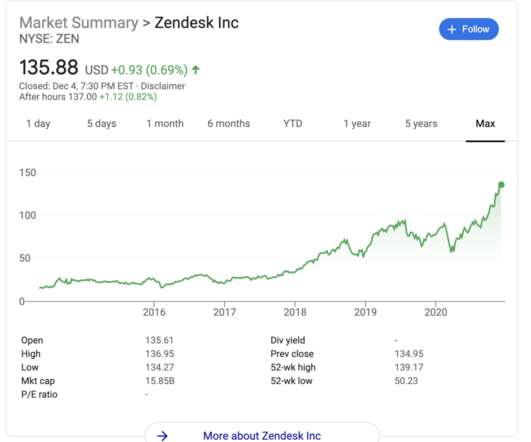

IPO in 2014 at $1B. First product doesn’t work, no revenue for 3 years. 2013: first investment. 200m from Silver Lake. 2016: IPO at $1.15B market cap. 2020: Worth $7B today. Zendesk : Founded 2006. Raised $500,000 (!) in first angel round in 2007. Worth $2B by 2017. Crossed $1B in ARR in 2020. Today worth $16B.

UIPath History 2005: Started as a tech outsourcing company 2014: $500k rev. UiPath has had an incredible history, taking 10 years to get to that first $1m in ARR … and then turning into one of the fastest growing software companies to $1 Billion in ARR ever ! seed round 2015: $1m rev. 2016: $3.5m rev 2017: $30m rev. 2018: $155m rev.

After the initial event exceeded our expectations, I decided to up my game for 2014. So at Pulse 2014, I became a “grown-up CEO.” Pulse 2014 was by far my worst keynote of all time. I hired a speaking coach (who was great in her own right, despite this story). Try writing out your speech and reading from a teleprompter.

Early businesses tend to create more instruments to hire, grow, and incentivize. tokens resemble equity in most ways, but possess one additional function: they can be used to pay for service. Trailing 2 Year Inflation Rate. Founded Year.

#1 source of traffic to [link] : 2022: SEO 2021: SEO 2020: SEO 2019: SEO 2018: SEO 2017: SEO 2016: SEO 2015: SEO 2014: SEO 2013: SEO 2012: SEO. Even Year 1 pic.twitter.com/5FtzBG2v1O. — Jason BeKind Lemkin #???????????? jasonlk) March 15, 2022. So we’re coming up on Year 10 for SaaStr!

We analyzed the S-1 in 2014. Yesterday, Salesforce announced it would acquire Tableau for $15.7B. Tableau sells data visualization software and the team has built an incredible business. The company has grown since its public offering to generate about $1.1B in revenue, growing at 29%. Let’s put this acquisition in context.

Put differently, if you look at multiples of revenue for top SaaS and Cloud companies above from 2014-2022, you could come to one of (at least) two conclusions today: Conclusion #1: Q2’20-Q4’22 Cloud Revenue Multiples Were a Covid Anomaly. This version of the BVP Nasdaq Index illustrates the question.

I remember back in 2014, I was at an event with a CEO that was truly great. Every startup I’ve joined or startup has almost failed. Heck, SaaStr itself has almost failed. We lost $10,000,000 in March 2020, and half the team then quit. But: He couldn't raise any money from anyone. Quite a bit.

(Note this is an update / refresh of our classic 2014 post). There are some real mysteries in SaaS. Even now that I understand them, I still see them as a bit of a mystery. Let me list a few: Why do customers buy a ton of seats up front , when they could start with a few and buy more later? Great for sales reps looking to hit their quota.

This led to our first meet-ups in 2013 and 2014, the first SaaStr Annual in 2015 , the industry’s leading podcast in 2016, the first SaaS founder coworking space in 2017, and SaaStr Pro , the first learning management system for SaaS founders in 2018. But all this was pretty novel back in 2014.

And when we wrote in 2014 that Box would surely cross $1B in ARR , many at the time didn’t quite get SaaS yet — or the power of recurring revenue. Box has been an important part of SaaStr almost since the beginning. Aaron Levie was kind enough to come to our first SaaStr Annual in 2015, just a week after their IPO.

2014 $4.1B. It seems like every market in SaaS is even bigger than we expected, and importantly, able to not just hit $1B in ARR but accelerate afterwards. Seize the day. Salesforce Growth: 2022 $26B (guidance) 2021 $21.25B 2020 $17.1B Thank you Ohana! From 1st Earnings Call Inside. We’re all vaccinated!) pic.twitter.com/DQAwBNHm2A.

. #13 SaaStr 222: Flexport CRO Ben Braverman on Why It Is Total Horseshit That The Best Sellers Don’t Make Good Managers, Why Specialisation Does Not Lead To The Best Customer Experience & Scaling Revenue From $18k MRR in 2014 to a $472m Year In 2018.

A year later, those trends have continued to converge, and SaaS valuations have resurged, reaching their highs of the 2014-2015 boom. If the first six months of 2017 are any indication, then 2017 should be roughly similar to 2016 and 2014 in terms of total dollars raised by SaaS startups in seed rounds through Series C.

Shopify’s first quarter revenue: Q1 2021: $989 million Q1 2020: $470 million Q1 2019: $321 million Q1 2018: $214 million Q1 2017: $127 million Q1 2016: $73 million Q1 2015: $37 million Q1 2014: $19 million Q1 2013: $9 million. — Jon Erlichman (@JonErlichman) April 28, 2021. But Shopify is growing so fast — 110% a year (!)

We organize all of the trending information in your field so you don't have to. Join 80,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content