This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

And then the “Flash Crash” of 2016 came, our first big hit. I did a deeper dive on SaaS multiples, and what that means for founders and SaaS execs, below at SaaStr APAC: The post The Three Valuation Lows in SaaS: 2013, 2016, and 2022 appeared first on SaaStr. It was just too hard to make money at 4x ARR.

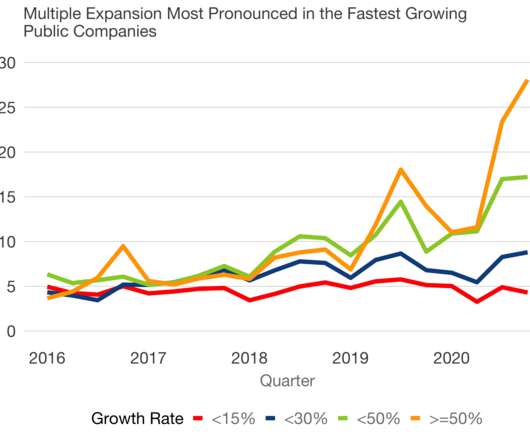

The top quartile companies are growing at slower rates today than the bottom quartile companies in 2016. There are few, fast growing, younger SaaS companies to sustain the growth rates. The median has never been lower in the last ten years.

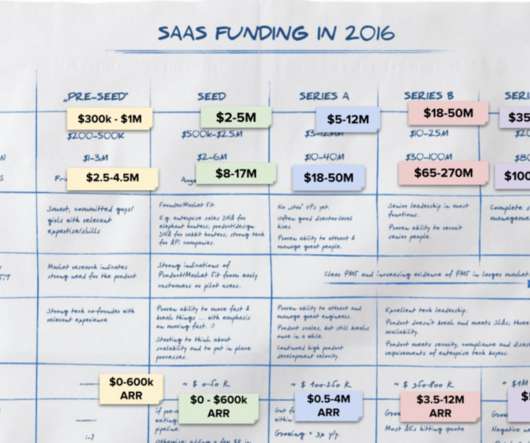

What began as a blog post in 2016 has evolved into a yearly exploration and survey to founders and investors to discover what it really takes to raise capital for SaaS companies. The Evolution of SaaS Funding From 2016 to 2021. Originally, in 2016, Point 9 measured MRR, but they have since changed their focus to ARR).

Since 2016, public software has witnessed four corrections. Also, 2014 to 2016 saw a 57% reduction in multiples and of course after 2008. In fact, the 75th percentile multiple has appreciated 25% annually since 2016 and the median has increased by approximately 20%. Today, we’re in the midst of the fifth. Correction Year.

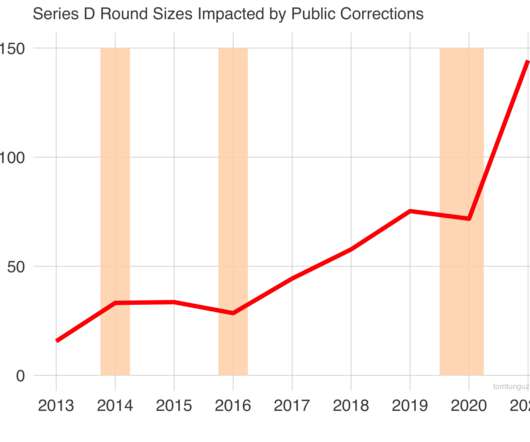

Only the 2016 reduction of 57% surpasses it. 2014’s correction stalled and then reversed Series D round sizes for 2 years through the second correction in 2016. The public software sector is weathering the second deepest multiple contraction in the last decade. These are marked in peachpuff orange rectangles above.

So Microsoft announced that LinkedIn, which it bought in 2016, has now crossed a stunning $10 Billion in ARR — and growing 27% year-over-year. Revenue tripled since Microsoft acquisition in 2016. Members “only” up 70%, while revenue up 300% since 2016. LinkedIn sold to Microsoft in 2016 for $26B.

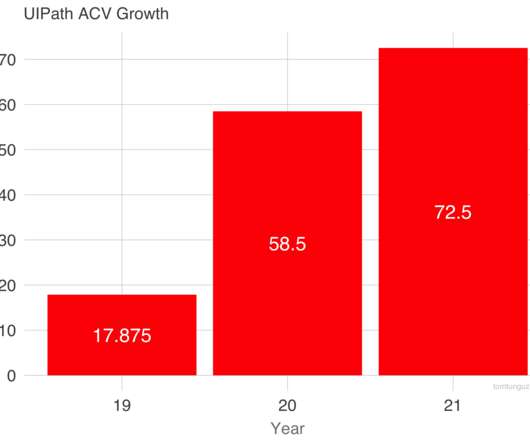

from 2015 to 2016 … and then exploded: UIPath History. 2016: $3.5m Top 50 customers grew bookings 81x since 2016, and all 2016 customers together grew 57x. These 2016 customers really leaned in on UiPath. And then after a decade … it started to come together. 2014: $500k rev. seed round. 2015: $1m rev.

Enterprise-value-to-forward-revenue multiples are now below 2016 levels for the first time in 6 in years. It happened in Feburary 2016. The public software market continues to compress. The 25th percentile of companies trade at 3.3x today compared to 4.0x The median or 50th percentile trade at 4.9x Would it be crazy to see 3.3x

2016 customer cohort spends 3.2x Blaze’s 2016 customers spend 3.2x more today than they did in 2016. But the past several quarters Braze has doubled its new customer growth, from 22%-29% to 48% today. That’s a challenge to everyone that says customer growth has to slow at scale. more today.

In 2014, 2016, 2020, 2021, these big mergers drove the figures into the tens of billions. X 2015 20.1% - 2016 43.0% Multi-billion dollar acquisitions, the blue bars, are the largest contributors to this swing. It’s no surprise that in those years, the biggest acquisitions accounted for more than 53% of dollars on average.

100k+ customers have gone from 50% of revenue in 2016 to almost 80% today: #2. From 2 $1m ARR customers in 2016 to 145 today. $100k+ customers are key to ARR growth. Datadog isn’t leaving the smaller customers behind, but they are increasingly a smaller percentage of revenue. More product, more products, more products.

Let’s go back in time … to early 2016. At SaaStr Annual 2016, in February, all the VCs were discouraged. “Unicorns are over,” they said. Just like Marketo was in the 2016 downturn. A sign many of those with the biggest checkbooks in SaaS think things will get substantially better. No way, you say?

January 2016, SaaS stocks were riding high. It was called 2016: * Everyone panicked * Seemed like multiples would never recover * LinkedIn sold to Microsoft for 7x ARR. That revenue multiples should rise from where they were in 2019. But I’m hardly sure this will happen in practice. And remember, we’ve seen this all before.

2016 was tough, too. But the markets also dropped 50% at the start of 2016, and VCs panicked. It was called 2016: * Everyone panicked * Seemed like multiples would never recover * LinkedIn sold to Microsoft for 7x ARR. There are enough good investors out there. — Jyoti Bansal (@jyotibansalsf) May 6, 2022. #6. And then ….

Since 2016, the average public software witnessed its sales efficiency winnowed from 52% to 47%, a decline of about 10%. Third, those lows touch the highs of the next rung down; i.e., the current levels of the 75th percentile companies’ sales efficiency is equal to the 50th percentile companies in 2016. What happened?

In other words, if machine learning startups raised the same amount of money in 2016 is 2010, the chart would show a value of 1. Advertising technology has seen a resurgence in 2016, reversing a three year trend of declines. There are fewer software startups raising capital in 2016 than 2015.

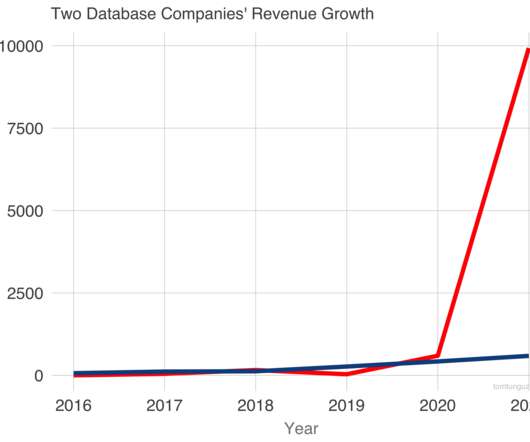

In 2016, each company recorded less than $50m in revenue. Both have grown very fast. In fact, their revenue trajectories through 2020 are nearly identical. Both companies employ a usage-based pricing model: pay for what you use. In two years, both would near $200m in revenue. They would both exceed $400m in 2020.

2016: IPO at $1.15B market cap. And yes, no one could have predicted the run we’ve seen in Cloud in the past few years. But take a look at these examples: Marketo (and Hubspot): Founded 2006. Marketo IPO’s in 2013 at $700m market cap. Vista buys Marketo for $1.8B A little more than 2 years later, it was resold for $4.75B to Adobe.

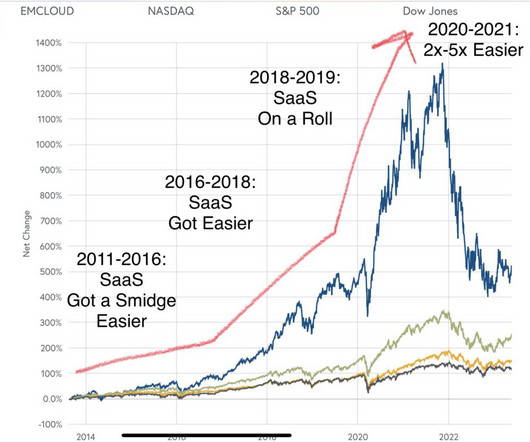

Cloud has been on an incredible tear since 2012 or so, and then even more since about 2016, and then as you can see above, went into hyperdive in about 2018 … and then into true warp speed after Covid. Yes, the markets have retreated a bit from their all-time highs. But does it even matter? SaaS and Cloud are up +1000% since 2013.

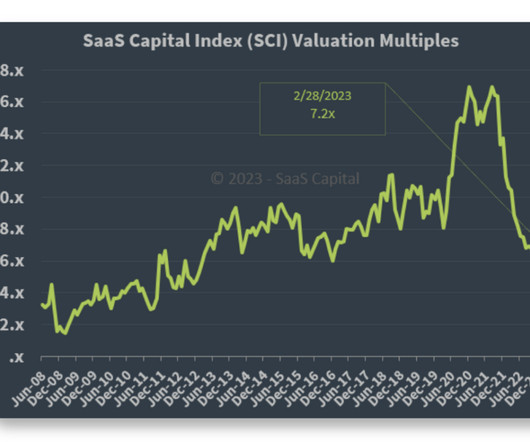

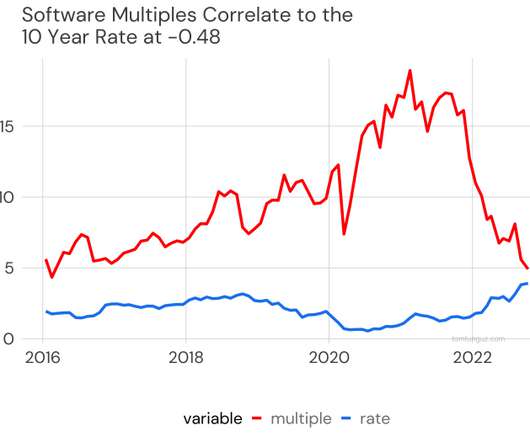

The chart above shows the median enterprise value to forward ARR value since 2016. To estimate ARR for a public company, we annualize the analyst consensus estimates for the revenue 4 quarters from today. It hovers around 5x until 2018, then spikes to 8x, and despite some volatility, reaches its current zenith at a bit more than 10x.

In less earth shattering news, the fact that it's 2017 also means that my "SaaS Funding in 2016" napkin needs an update. As a reminder, in the original post I tried to give a "back of a napkin" answer to this question: What does it take to raise capital, in SaaS, in 2016?

In 2016, valuations fell 57%. MongoDB fell 24%; UIPath fell 36% ; Salesforce fell 15% ; Workday was down 11%. Weaker revenue projections tend to cause sell-offs. These large drops aren’t unprecedented. Is it different this time? Growth rates have changed meaningfully.

2016: Dharmesh joined us for the first time, with one of the most engaging and highly-rated SaaStr Annual session on ever: their journey to IP O. In the run-up to SaaStr Annual 2022 on September 13-15 , we wanted to look back at some of the highest-rated SaaStr sessions of all time, since the first SaaStr Annual in 2015.

Well, if it were 2016, we’d say no. Bill.com is one of my favorite sleeper SaaS companies. Half of its revenues comes from its software. And half from fees on transactions it processes: Is this all really ARR? But it isn’t. With an incredible 121% NRR from SMBs, it all essentially recurs. Only half does.

It’s not slowing down Salesforce, Snowflake, or almost any other SaaS or Cloud leader. Salesforce Growth: 2023 $31.8B (guidance) 2022 $26.5B 2021 $21.25B 2020 $17.1B 2014 $4.1B. Thank you Ohana! pic.twitter.com/CMhrBXgHSF. — Marc Benioff (@Benioff) May 31, 2022. We may be headed for a big downturn, we’ll see.

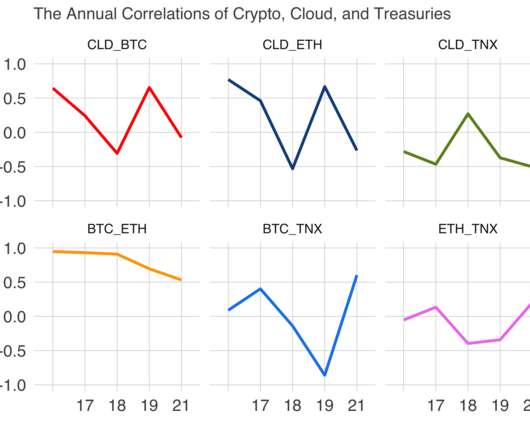

BTC and ETC moved more or less in synchrony from 2016 to 2018. Economics students would argue the discounted cash flow model predicts this behavior. Companies with profits in future years should be less valuable during times of higher interest rates. Three years ago, they went their separate ways.

Automattic was started in 2005 to democratize publishing, and WooCommerce was purchased in 2016 to democratize e-commerce. When WordPress purchased WooCommerce in 2016, they believed it would become their biggest business. Now, Woo is an open-source style Shopify and their largest business. Then, in 2023, they moved into messaging.

So the minor point is maybe we’re just back to 2016-2017 in SaaS venture capital for Series A and later rounds. For the best ones. But the bigger point is especially for new founders and execs to just look at the chart above. We’re never “going back” to how things were in late 2020 and 2021.

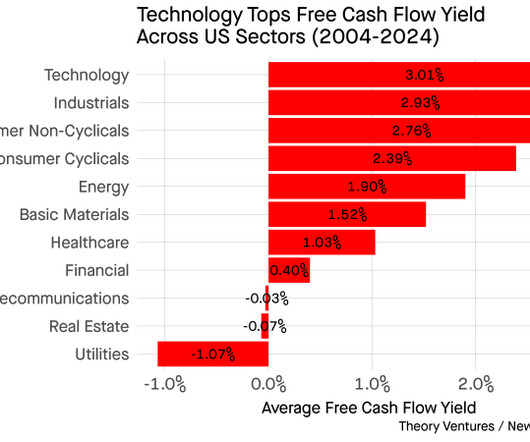

For a period from December 9, 2009, to approximately March of 2016, technology companies produced nearly 5% free cash flow yields on average. Software companies top the charts at 3% over the last 20 years, according to data from New Constructs , a financial research firm. There are times when other sectors yield more.

During the dotcom crash in 2001, the Global Financial Crisis of 2008, and the SaaS corrections in 2014, 2016, and 2018, Lee was either COO/CFO or CFO at Twilio, SAY Media, and Ofoto. Lee Kirkpatrick is no stranger to downturns.

But importantly, it’s raised its ACV 4x since 2016. Docebo’s pricing is on the “corporate” side of LMS. It doesn’t compete at the bottom of the market, and targets top logos with a reasonably priced product. Without that, the company would likely be a fraction of its current ARR. #3.

We’ll see, but Zendesk for $10B in 2022 may turn out to be the LinkedIn for $26B in 2016 of this downturn. Yet, founders have only partially adjusted to the new world. A much, much harder and higher hill. A deal that is fair & makes sense when markets are turbulent and worried. But in just a few years, looks like just such a huge bargain.

note: an updated version of a classic 2016 post). Even if today, it’s just not quite enough. It will be later, if your team is strong enough, you will is there, and your customers believe in you. The post Never Quit If appeared first on SaaStr.

Salesforce Growth: 2021 $20.8B Guidance 2020 $17.1B 2014 $4.1B. Thank you Ohana! — Marc Benioff (@Benioff) August 25, 2020. If you haven’t done a SaaS start-up before, it’s different. The reasons are many, but I think they can almost all be summed up in one key factor: SaaS compounds.

California-based VCs in their portfolio invested 43% of their new investments outside California , up from 29% in 2016. But California funds continued to look outside of the Bay Area. That’s interesting to see quantified. Crazy times in SaaS and Cloud indeed. note: Sapphire Ventures is an LP in SaaStr Fund).

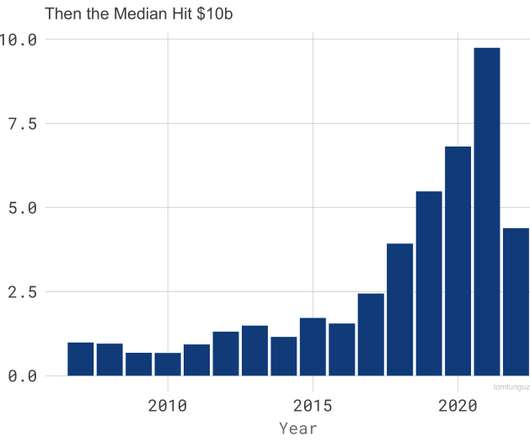

From 2007 to 2016, $1.5b I remember thinking a $1b M&A or IPO was so rare an investor might hope to achieve it once or twice in a career. Fewer than 15 SaaS companies traded on public exchanges then. With at least 20 firms and several partners per firm chasing unicorns, upstarts faced stiff odds. 2015 Return Multiple by Round.

2016: $3.5m UiPath has had an incredible history, taking 10 years to get to that first $1m in ARR … and then turning into one of the fastest growing software companies to $1 Billion in ARR ever ! UIPath History 2005: Started as a tech outsourcing company 2014: $500k rev. seed round 2015: $1m rev. rev 2017: $30m rev. 2018: $155m rev.

The company also mentions the 2016 cohort of customers expanded 51x in the last 5 years. In 2021, the business counted more than 8000 customers, with 1000 paying more than $100k and 89 paying more than $1m. In addition, 70% of new bookings in 2021 originated from expansions.

Not easy, but easier and easier: There was a bump in 2016, a Flash Crash in SaaS, when budgets were slashed, but it didn’t last long enough to really impact renewal cycles. SaaS markets had fully recovered later that year. Even the 2008-2009 downturn, while truly brutal, didn’t hit SaaS as hard as the rest of the economy.

#1 source of traffic to [link] : 2022: SEO 2021: SEO 2020: SEO 2019: SEO 2018: SEO 2017: SEO 2016: SEO 2015: SEO 2014: SEO 2013: SEO 2012: SEO. Even Year 1 pic.twitter.com/5FtzBG2v1O. — Jason BeKind Lemkin #???????????? jasonlk) March 15, 2022. So we’re coming up on Year 10 for SaaStr!

Karim previously built and sold Y Combinator-backed Paribus to Capital One in 2016. Ramp is a leading finance automation platform. Founded just in 2019, they were valued at $8.1 billion two years after launch. The second-timers see things differently.

When I analyzed the SaaS fundraising market in 2016 , three trends emerged. Across all rounds, both lines are up into the right, despite some volatility in 2016. In 2016, venture capitalists reduced their investment in staff companies by 1 ⁄ 3 , falling to $2.8 Meanwhile, round sizes swelled. billion from $4.2

This led to our first meet-ups in 2013 and 2014, the first SaaStr Annual in 2015 , the industry’s leading podcast in 2016, the first SaaS founder coworking space in 2017, and SaaStr Pro , the first learning management system for SaaS founders in 2018. 2016 The Second SaaStr Annual: From Impossible to Inevitable .

We organize all of the trending information in your field so you don't have to. Join 80,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content