This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The top quartile companies are growing at slower rates today than the bottom quartile companies in 2016. There are few, fast growing, younger SaaS companies to sustain the growth rates. The median has never been lower in the last ten years.

We’ve used various bits of the BVP Nasdaq Index and metrics since they launched a few years ago to highlight trends in SaaS and Cloud. This week even after a pullback, public SaaS and Cloud companies are up an eve 1000% (!) SaaS and Cloud are up +1000% since 2013. since 2013. But does it even matter?

In the latest installment of SaaStr’s What’s New series – where we sit down with the leaders in SaaS and Cloud for the inside scoop on what’s top of mind and what’s new, SaaStr CEO and Jason Lemkin chats with the CMO of Google Cloud, Alison Wagonfeld. They also compete with Microsoft in a big way.

In this informative SaaStr Annual session, Bessemer Partners Sameer Dholakia, Mary D’Onofrio, and Elliott Robinson present the State of Cloud report, a look at the latest in SaaS trends, predictions, and cloud economics. Cloud Stocks Impacted by Macro Environment. Reminder: Cloud Fundamentals Are Still Strong.

UiPath is one of the most amazing not-really-an-overnight success stories in Cloud, SaaS and software. It was founded way back in 2005 as an outsourcing company, then developed Windows software to automate scripts and more, and turned this into a powerhouse for automating complex functions integrating Cloud and on-prem. 2016: $3.5m

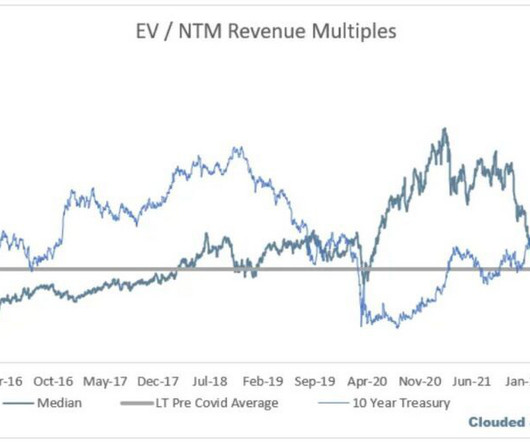

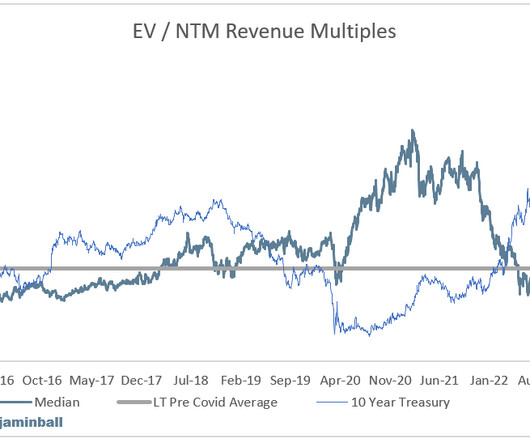

Since 2016, public software has witnessed four corrections. Also, 2014 to 2016 saw a 57% reduction in multiples and of course after 2008. In fact, the 75th percentile multiple has appreciated 25% annually since 2016 and the median has increased by approximately 20%. Today, we’re in the midst of the fifth. Correction Year.

So Microsoft announced that LinkedIn, which it bought in 2016, has now crossed a stunning $10 Billion in ARR — and growing 27% year-over-year. Because SaaS and Cloud are. Revenue tripled since Microsoft acquisition in 2016. Cloud is an awesome force. #4. LinkedIn sold to Microsoft in 2016 for $26B.

100k+ customers have gone from 50% of revenue in 2016 to almost 80% today: #2. Almost all the Cloud leaders accelerating after $100m ARR, let alone $1B ARR, are multi-product. #3. A reminder there is no ceiling to top tier NRR in SaaS and Cloud. From 2 $1m ARR customers in 2016 to 145 today. 10 new products this year.

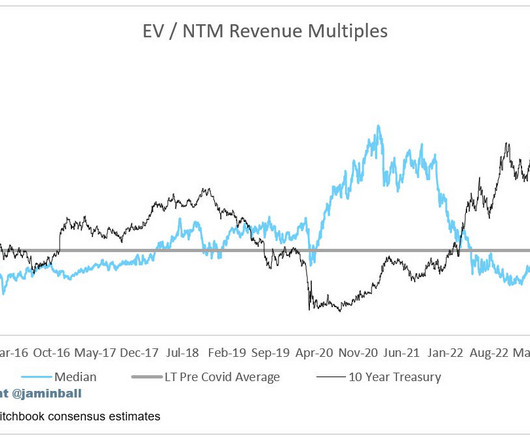

Many SaaS and Cloud leaders are down more than 50% from their all-time highs. But Covid did create a lot of artificial demand for Cloud products, especially the lockdown phase. Update on cloud software multiples, charted alongside the 10Y and 5 year pre-covid NTM rev multiple average. January 2016, SaaS stocks were riding high.

With each passing year, more and more of our online existence becomes tethered to the cloud. But how does the cloud take shape, and what can companies do to position themselves at the heart of its growing infrastructure? Infrastructure: Reloaded for the Cloud. Pro Tips for Modern Cloud Infrastructure.

And yes, no one could have predicted the run we’ve seen in Cloud in the past few years. 2016: IPO at $1.15B market cap. These are the Best of TImes in Cloud and SaaS. Or move on to the next thing. But take a look at these examples: Marketo (and Hubspot): Founded 2006. Marketo IPO’s in 2013 at $700m market cap.

It’s not slowing down Salesforce, Snowflake, or almost any other SaaS or Cloud leader. Blame “the economy” too much, and you’re doing yourself a disservice. Salesforce Growth: 2023 $31.8B (guidance) 2022 $26.5B 2021 $21.25B 2020 $17.1B 2014 $4.1B. Thank you Ohana! pic.twitter.com/CMhrBXgHSF. — Marc Benioff (@Benioff) May 31, 2022.

But like “Cloud” and “SaaS”, its definitely has evolved. Well, if it were 2016, we’d say no. So many startups these days are claiming they have “ARR” from revenue that … doesn’t recur. Doesn’t ARR stand for Annual Recurring Revenue? Well of course it does. But it isn’t.

Around 2013 or so, the Cloud started to grow far faster than any of us had thought it would: Amazon Web Services revenue 2018 | Statista. There were dips in 2016 and otherwise. It turned our CIOs and bigger companies were ready to transfer as much as another 20% of their $1 trillion+ IT budgets to Cloud far faster than any of us knew.

and as Cloud continues to scale: Many of the best in SaaS are accelerating even at massive scale. Zscaler , a quiet giant in Cloud security, also accelerated to 60% growth at $700m ARR! Cloud is just on fire. They did it the hard way, with SMBs. — Jason BeKind Lemkin (@jasonlk) May 6, 2021. Growth at $500m ARR is 51%.

The company exploded from 3,000 restaurant locations in 2016 to 40,000 in 2020. Not uncommon in fast-growing Cloud companies, but a CAC that does consume a significant amount of capital, especially in a business with lower margins and a large hardware component. #5. But it took 6+ years to get there. Mediocre margins in payments.

California-based VCs in their portfolio invested 43% of their new investments outside California , up from 29% in 2016. Crazy times in SaaS and Cloud indeed. But California funds continued to look outside of the Bay Area. That’s interesting to see quantified. note: Sapphire Ventures is an LP in SaaStr Fund).

2004-2010 marked the early days of SaaS where the model was still risky, and cloud providers were competing hard with their on-prem predecessors. . In 2016, Digital Ocean opened a $130m credit facility with Keybanc. . The SKYY First Trust Cloud Computing ETF has grown to $3.3 This venture debt is a form of production capital.

This led to our first meet-ups in 2013 and 2014, the first SaaStr Annual in 2015 , the industry’s leading podcast in 2016, the first SaaS founder coworking space in 2017, and SaaStr Pro , the first learning management system for SaaS founders in 2018. 2016 The Second SaaStr Annual: From Impossible to Inevitable . It was a hit!

Every week I’ll provide updates on the latest trends in cloud software companies. Subscribe now Azure Report - Cloud Infra Looks Good! The full quote is below: “We expect capital expenditures to increase materially on a sequential basis driven by cloud and AI infrastructure investments.

Which of the 16 major start of categories in information technology will reap disproportionate share of investment dollars in 2016? Cloud computing, which encompasses the infrastructure products used by developers to build services, has remained flat at 4% over the past five years despite some recent declines in 2013 and 2014.

Founded in 2016, Lark effectively combines messaging, schedule management and online collaborative documents in a single platform. Our mission at Vanta is to be a layer of trust on top of cloud services, to secure the internet, increase trust in software companies, and keep consumer data safe.

10 years later, they hit $100m ARR in 2016 and growth just compounded from there. Gotta Radically More Efficient in 2023 This is really the theme of the year in SaaS and Cloud. AppFolio, up 87% this year when many in SaaS and Cloud have struggled. They’ve made up for it by being leaner, as we see above.

Shopify’s first quarter revenue: Q1 2021: $989 million Q1 2020: $470 million Q1 2019: $321 million Q1 2018: $214 million Q1 2017: $127 million Q1 2016: $73 million Q1 2015: $37 million Q1 2014: $19 million Q1 2013: $9 million. Cloud and ecommerce may end soon, but it hasn’t ended yet. 5 Interesting Learnings: #1.

It’s a time when SaaS and Cloud spend are also at record highs , and many Cloud leaders are still growing at strong rates … yet many startups have stopped growing at all. You can see here multiples are touching the lows of early 2016 and are even lower than 2015 and those early days of SaaS. And really worst of all is multiples.

Every week I’ll provide updates on the latest trends in cloud software companies. Some of these drops rival one of the worst ever software earnings reaction of Tableau in 2016! This is very reminiscent of the Tableau drop in 2016. Subscribe now Share Clouded Judgement Leave a comment Follow along to stay up to date!

This week in enterprise software: Top 10 #SaaS #Cloud multiples as of today's market close. The median multiple fell below 5x at market close for the first time since 2016 (when it briefly fell below 5x) pic.twitter.com/QZ605lMswz. That’s massive change. — Jamin Ball (@jaminball) October 14, 2022.

It is a cloud-based platform that offers the services of Asia’s top AI assistant for hotel staff – Gaia. Founded : 2016. It provides smart hardware self-development and cloud service. Mobingi integrates server deployment, scaling and application lifecycle automation through its cloud solution. Funding to Date : $1.3M

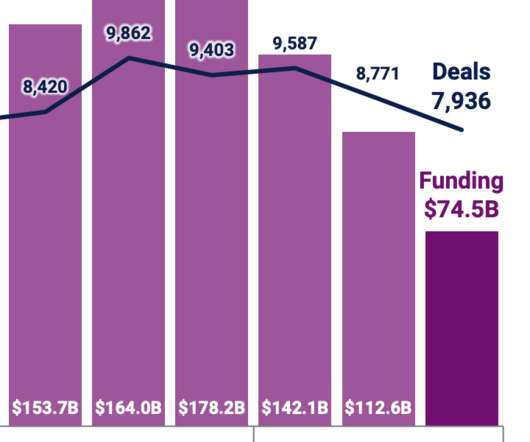

On the one hand, to any of this that have been doing this for a while, there are a ton of new funds in market (1,000+ new funds since 2016!) We’ve had 2 records years in a row of VC investment: But … but look what’s happened in tech and the Cloud: Explosion! and the exiting funds have raised vastly more capital than before.

After 11 years in finances, in 2016 she became the CFO of Brinc.io, boldly entering into the tech world. With more than 15 years of solid experience, today she is the Chief Operations Officer at the Ping An Health Cloud, known as the most advanced AI healthcare technology. In 2016, she moved to Hong Kong to head Innovation at HSBC.

Prior to joining Squarespace in 2016 she was the CFO of Info and spent 17 years in leadership roles at IBM. Hear how the company grew from its small beginnings to the cloud behemoth it is today. The software platform allows customers to build and host websites while using pre-built templates. Rahul Vohra, Superhuman Founder, and CEO.

About Mikkel… According to Mikkel “the cloud’s biggest days are yet to come”, his stories of a time when “the cloud” wasn’t exactly the reality it is today inspired SaaStr attendees to heavily bookmark his session ahead of the event. In 2016 they sold Pagar.me, left Brazil and enrolled in Stanford.

In addition, 2018 acquisition values for this type of acquisition exceed $60B, more than twice 2016, which included the Microsoft/LinkedIn merger. The shift to the cloud has happened at a greater scale than most legacy software businesses estimated. It’s the best M&A market in the last seven years for $1B+ sales with six.

As is the case with Dell Technologies, one of the largest tech companies — which went private 2012-2013 and then also pulled off one of the most epic mergers of all time with Dell + EMC + VMWare 2015-2016 (and which we wrote about here at the time). Is there a method to the madness?

BetterCloud is featured in 145 G2 Winter 2025 Grid Reports and named a Leader in SaaS Operations Management, SaaS Spend Management, Data Loss Prevention, and Cloud File Security. See why BetterCloud is a leader in SaaS Operations Management and Cloud File Security. To our amazing customers, thank you! Eduardo R.,

Jennifer has been at PagerDuty since 2016, a disruptive company that took automation to the next level before AI was hot in 2024. Looking back in history at every other disruptive automation or technical step-change, whether the smartphone or Cloud computing, people stepped up their game and built more creative and interesting things.

Tencent has done 43 investment deals in 2018, 72 investment deals in 2017 and 50 in 2016. It’s also running the Capital Innovation Accelerator Fund targeted at cloud computing, Internet of Things (IoT), mobile and e-commerce startups. Founded: 2016. In 2016, Ardent Capital merged with Wavemaker Partners. Founded: 2013.

Omie is a management platform in the cloud for small and midsized companies, bringing together ERP, Financial Services, Entrepreneur Education and a vibrant Marketplace for vertical 3rd party solutions, all combined in an easy to use environment. Founded : 2016. Founded : 2012. Based in: Rio de Janeiro, Brazil. Funding to Date : $6.6M

Looking for: Microsoft office and home business 2016 free. Microsoft Office 2016. Office E3 is a cloud-based suite of productivity apps and services with information protection and compliance capabilities included. Click here to Download. Share and manage content, knowledge, and apps with SharePoint Online storage.

Bessemer Venture Partners’ Alex Ferrara takes a look at trends and predictions for the cloud industry in 2019. One of the most popular sessions from SaaStr Annual, this presentation will provides an in-depth look at the cloud computing industry across Europe and globally. Want to see more content like this? A few more.

In 2016, Janz did research and tried to answer this. It’s no surprise when looking at a chart like this one showing Bessemer’s Emerging Cloud Index. They aren’t dinosaurs that didn’t manage to move to the Cloud. The Proverbial Napkin What does it take to raise capital in SaaS in 2023?

Duo Security, now a part of Cisco, is a provider of unified access security and multi-factor authentication delivered via the cloud. Adaptive Insights is a cloud-based platform for modernizing business planning. In 2008, Jeff founded Twilio and has since seen the company through it’s 2016 IPO and beyond.

” Microsoft 2016 Annual Report You can read more about IDC’s analysis of Microsoft’s channel structure here. Modern companies are born in the cloud, and independence is in their DNA. Thomas Hansen was Worldwide Vice President of SMB at Microsoft. The Channel Distribution Opportunity. by Thomas Hansen.

We organize all of the trending information in your field so you don't have to. Join 80,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content