This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

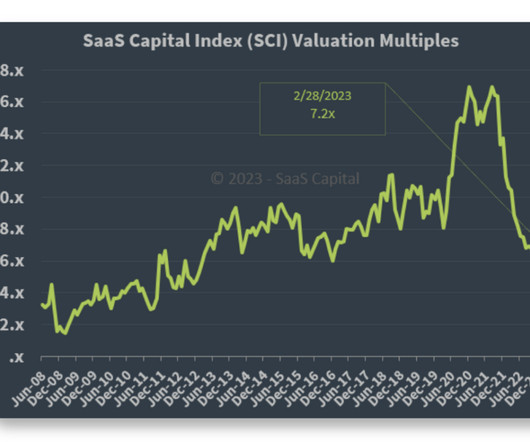

The SaaS Capital Index from SaaS Capital had a nice summary this week of the 3 low points we’ve seen in SaaS multiples, and this chart puts things in great context: As you can see above, in the early days of SaaS … it was tough to be a public SaaS company. It was just too hard to make money at 4x ARR.

Since 2016, public software has witnessed four corrections. Also, 2014 to 2016 saw a 57% reduction in multiples and of course after 2008. In fact, the 75th percentile multiple has appreciated 25% annually since 2016 and the median has increased by approximately 20%. Today, we’re in the midst of the fifth. Correction Year.

A sign many of those with the biggest checkbooks in SaaS think things will get substantially better. Let’s go back in time … to early 2016. The public markets were brutal then for SaaS, with LinkedIn, Marketo, and other leaders of that generation way down. Just like Marketo was in the 2016 downturn.

When we invest in a SaaS startup, which almost always happens at the seed stage, the next big milestone on the company’s roadmap is usually a Series A. Some SaaS companies got big without raising a lot of capital – Atlassian, Basecamp and Veeva are probably the most famous examples. They are a means to a bigger goal.

Public SaaS companies’ growth rates have halved since 2023, as David Spitz pointed , from 36% to 17%. There are few, fast growing, younger SaaS companies to sustain the growth rates. The top quartile companies are growing at slower rates today than the bottom quartile companies in 2016. When will it change ?

Many SaaS and Cloud leaders are down more than 50% from their all-time highs. A Covid Hangover in SaaS stocks.’ The top SaaS and Cloud leaders are even accelerating at $1B in ARR, for goodness sakes!! The point is that SaaS multiples are still higher than where they were from 2010-2017.

We’ve used various bits of the BVP Nasdaq Index and metrics since they launched a few years ago to highlight trends in SaaS and Cloud. This week even after a pullback, public SaaS and Cloud companies are up an eve 1000% (!) SaaS and Cloud are up +1000% since 2013. since 2013. But does it even matter?

2016: IPO at $1.15B market cap. These are the Best of TImes in Cloud and SaaS. The post The Power of Going Long in SaaS appeared first on SaaStr. And yes, no one could have predicted the run we’ve seen in Cloud in the past few years. But take a look at these examples: Marketo (and Hubspot): Founded 2006. Solo founder.

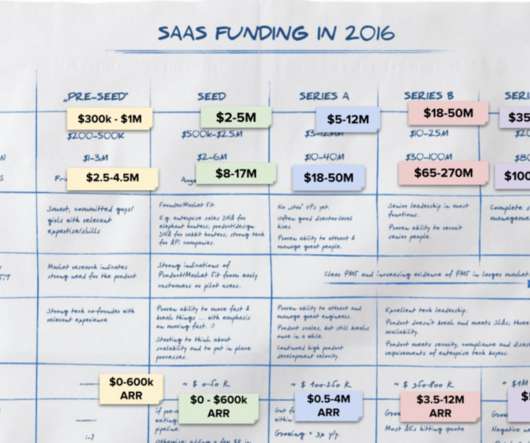

In less earth shattering news, the fact that it's 2017 also means that my "SaaS Funding in 2016" napkin needs an update. As a reminder, in the original post I tried to give a "back of a napkin" answer to this question: What does it take to raise capital, in SaaS, in 2016? Slack , unbelievably, reached $100M in ARR just 2.5

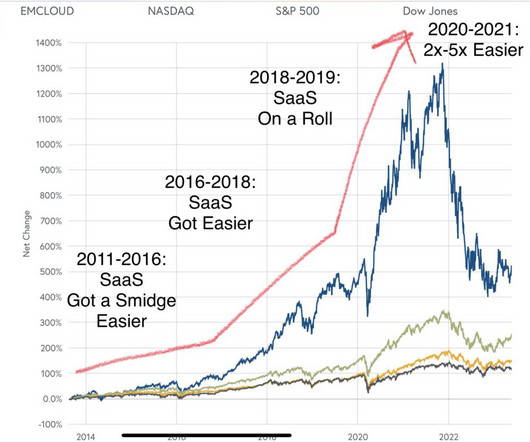

Not easy, but easier and easier: There was a bump in 2016, a Flash Crash in SaaS, when budgets were slashed, but it didn’t last long enough to really impact renewal cycles. SaaS markets had fully recovered later that year. Even the 2008-2009 downturn, while truly brutal, didn’t hit SaaS as hard as the rest of the economy.

2016 has been a year where knowledge has become freely available for anyone interested in knowing about all things SaaS. That’s because the people who are working in the SaaS industry or investing in these businesses are sharing much more of the details about all aspects of growing and scaling a SaaS business.

The SaaS Funding Napkin. What began as a blog post in 2016 has evolved into a yearly exploration and survey to founders and investors to discover what it really takes to raise capital for SaaS companies. The Evolution of SaaS Funding From 2016 to 2021. Pre-Seed Round: Round Size – 2016: $200K – $500K.

If you haven’t done a SaaS start-up before, it’s different. The reasons are many, but I think they can almost all be summed up in one key factor: SaaS compounds. What does this mean, that SaaS compounds? Success builds on success in SaaS. The post Want to Understand SaaS? Salesforce Growth: 2021 $20.8B

So there are a lot of rough and arm chair metrics for fundraising in SaaS in terms of valuations. For years, the standard was “about 10x” Top tier SaaS companies would tend to raise at around 10x ARR, with ones with slightly lower growth often raising at 5x. And then things just went crazy. For the best ones.

So Microsoft announced that LinkedIn, which it bought in 2016, has now crossed a stunning $10 Billion in ARR — and growing 27% year-over-year. Because SaaS and Cloud are. Revenue tripled since Microsoft acquisition in 2016. Members “only” up 70%, while revenue up 300% since 2016. B2B market is on fire.

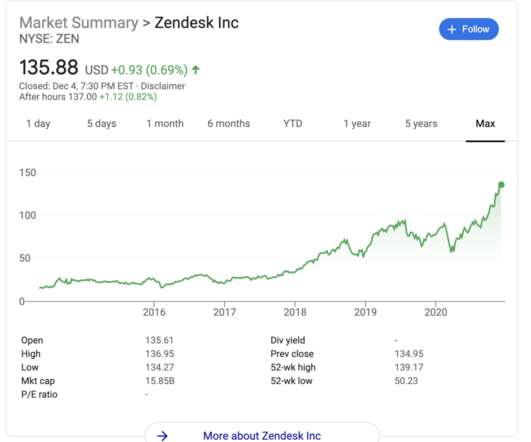

So two big PE $10B deals happened in SaaS this week, one agreed, the other closed. And the difference are so stark, they highlight all the changes in SaaS in just a few months: Zendesk agreed to be acquired a PE syndicate for $10.2 SaaS multiples have fallen sharply. Billion , going private. Billion closed.

UiPath is one of the most amazing not-really-an-overnight success stories in Cloud, SaaS and software. from 2015 to 2016 … and then exploded: UIPath History. 2016: $3.5m One of the fastest-growing SaaS companies ever. Is it really SaaS? Even if a lot of the revenue isn’t truly recurring SaaS revenue.

As an example, I showed a (fictional) SaaS startup that wants to grow from $1,000 in MRR to ~ $85,000 in MRR within one year. To follow-up on the topic, I've put together a very simple (Google Sheets based) calculator which startup founders might find useful when they work on their plan for 2016.

Debt for SaaS companies done right is a gift. Few folks have more data than Nathan Latka and he offers up some insights on how to properly leverage up in SaaS. Geoffrey Moore calls this group the Late Majority and the Laggards in his book Crossing the Chasm , a secret bible for many SaaS CEO’s. . — ed.

We just haven’t seen the type of acceleration at scale we’re seeing in SaaS leaders before. 100k+ customers have gone from 50% of revenue in 2016 to almost 80% today: #2. A reminder there is no ceiling to top tier NRR in SaaS and Cloud. From 2 $1m ARR customers in 2016 to 145 today. To 75% growth.

What started as a simple WordPress blog in 2012 has now become the world’s largest community of SaaS executives, founders, and entrepreneurs. And SaaStr Europa brings 2,500+ SaaS execs, founders, and VCs together to Europe every summer. We were the first major SaaS event back in the SF Bay Area. SaaStr is turning 10!

Braze is yet another SaaS leader growing even faster past $200m ARR. 2016 customer cohort spends 3.2x Blaze’s 2016 customers spend 3.2x more today than they did in 2016. A good yardstick for more enterprise-focused SaaS. What you’d expect, and it’s helpful to see this segmented. more today.

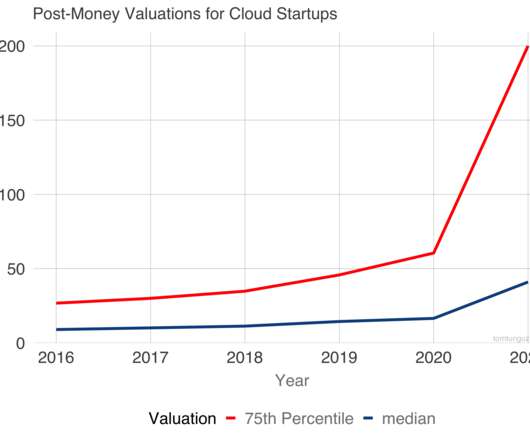

How far along was the typical SaaS Series A in 2018? The chart below shows a representative sample of SaaS Series As’ ARR and projected ARR growth rate for 2018. In 4 years, we’ve seen a 4x increase in the median MRR of a Series A SaaS company. The median business was at $1.8M in ARR and growing at 250%.

Q: What will SaaS companies look like in the future? I’m no brilliant futurist, but here’s what I see in the best SaaS companies today, so I assume will be table-stakes going forward: The Bay Area will remain a draw, but mainly as a small-ish HQ. Overall corporate budgets for SaaS will start to come under stress. It’s too much.

When I analyzed the SaaS fundraising market in 2016 , three trends emerged. The number of SaaS companies raising rounds had stalled, while the total number of dollars plateaued. A year later, those trends have continued to converge, and SaaS valuations have resurged, reaching their highs of the 2014-2015 boom.

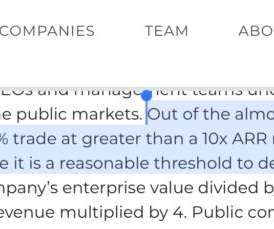

Last week, SaaS stocks fell by about 18% on average. The worst of them was in February 2016 when multiples fell by approximately 60%. The chart above shows the most recent enterprise value to forward multiple for a basket of next-generation software companies. As of Friday, the median forward multiple is 9.3x

If nothing else, expect a fraction of the new SaaS unicorns we saw in 2021. With so many amazing public SaaS companies now worth just $2B. So many top mid and later stage SaaS companies raised tons of capital in 2021, so much … that few really need to go back to market and raise again this year. 2016 was tough, too.

These 18 women are powerful, relentless and are all making SaaS and tech in general a better place. They have impressive professional achievements, all the way from founding companies through to running international operations across continents all the way to funding the SaaS companies of the future. They are stars in tech in Asia.

A lot of our SaaS older times don’t quite know what to make with a lot of B2B startups these days, let alone some public SaaS companies. But like “Cloud” and “SaaS”, its definitely has evolved. But like “Cloud” and “SaaS”, its definitely has evolved. Only half does.

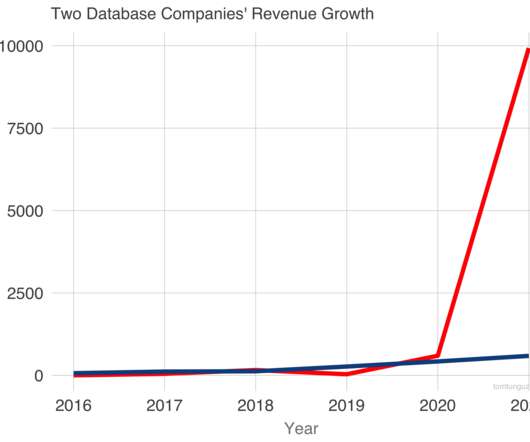

In 2016, each company recorded less than $50m in revenue. The fastest growing public SaaS company last year charted 1.1x Both have grown very fast. In fact, their revenue trajectories through 2020 are nearly identical. Both companies employ a usage-based pricing model: pay for what you use. They would both exceed $400m in 2020.

Some areas of spending are slowing in the economy, but SaaS overall is still growing faster than ever. It’s not slowing down Salesforce, Snowflake, or almost any other SaaS or Cloud leader. But it’s not here yet, at least not across the board on average in SaaS. Salesforce Growth: 2023 $31.8B (guidance) 2022 $26.5B 2014 $4.1B.

In 2017, SaaS companies reported their cost of customer acquisition had increased by 65% in the previous five year period. Since 2016, the average public software witnessed its sales efficiency winnowed from 52% to 47%, a decline of about 10%. What happened to these figures during Covid? What happened? Here’s my hypothesis.

The second SaaStr post ever, way back in late 2012, was “ Everybody Lies: SaaS Revenues in the Inc. 5000 “ It was a fun one, analyzing the only public source of data on just how much ARR a lot of SaaS companies had. Box in 2015 was the first IPO from the SaaS 2.0 Really more Adtech than SaaS. #8 generation.

In 2010, classic SaaS was booming, the benefits of a subscription model were finally becoming clear to the public markets and the mass-market. In other words, if machine learning startups raised the same amount of money in 2016 is 2010, the chart would show a value of 1. However, the story is different if we look at round counts.

Which of the 16 major start of categories in information technology will reap disproportionate share of investment dollars in 2016? This may be a breakout category in 2016 for Series A investments. During the period, we two salient education companys have gone public: 2U, a SaaS online college company worth $1.3B

When we announced a few weeks ago that we would be bringing our leading SaaS conference to Asia, and running it in Hong Kong, many locals thanked us for choosing the city. Horangi provides cyber security solutions based on SaaS. Founded : 2016. Fadada is a SaaS-based provider of electronic signature services.

More here: If You Have 10 {Unaffiliated} Customers in SaaS — You Have Something. Because SaaS and recurring revenue compounds. More on this stage here: How To Know You’ve Hit First Traction In SaaS. But again, SaaS compounds. You can’t always make something out of nothing in SaaS. Just never quit.

I miss #SaaStrAnnual and all my fellow SaaS peeps. 2016: Dharmesh joined us for the first time, with one of the most engaging and highly-rated SaaStr Annual session on ever: their journey to IP O. Hope to see you this year, @jasonlk. — dharmesh (@dharmesh) January 21, 2022.

As we have showcased in previous pieces, there are many reasons to be excited about the Latin American SaaS ecosystem. Not only is the region producing superstar SaaS contenders, but the interest from local and international VCs is increasing. However, our interest goes beyond the current state of SaaS in Latin America.

Through the end of July in 2016, $70B worth of SaaS companies sold. The more than $600B in cash on the balance sheets of large public tech companies combined with a recent pricing correction in SaaS companies presaged a flurry of acquisition activity. In 2016, these PE firms aren’t following that playbook.

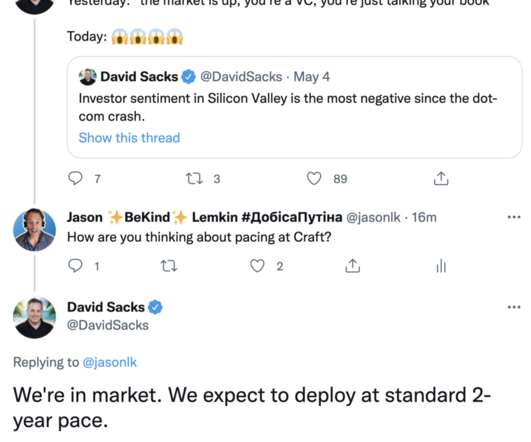

It was a really great deep-dive on where venture is right now: Multiples have fallen back to 2015 and 2016 Why VCs can’t justify investing at $100m+ valuations in many cases today How optimism is bleeding out of VC, and realism has seeped in Why the “next round” often isn’t coming anymore, and how everything got inverted in (..)

About $1B has been invested in early stage SaaS startups as of November 1. If we compare these trends to the total aggregate market capitalization of public SaaS companies by buyer, we observe a few interesting patterns. This operations category hints at the rising importance in the fundraising market of vertical SaaS companies.

The Latin American SaaS landscape is hustling and bustling, having seen more IPOs in the last 6 months than the previous 20 years combined. We will gather 300 leading SaaS founders, executives and investors for three days packed with opportunities and rich exchange of knowledge to push the whole ecosystem forward. Founded : 2013.

So there’s a quiet SaaS success story you probably don’t know much about, but can learn a lot from. But importantly, it’s raised its ACV 4x since 2016. Example: quiet SaaS learning software Docebo: pic.twitter.com/jtGwErBPu6. It’s Docebo. And yet … It’s worth $1.1 Yes, you can.

We organize all of the trending information in your field so you don't have to. Join 80,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content