This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

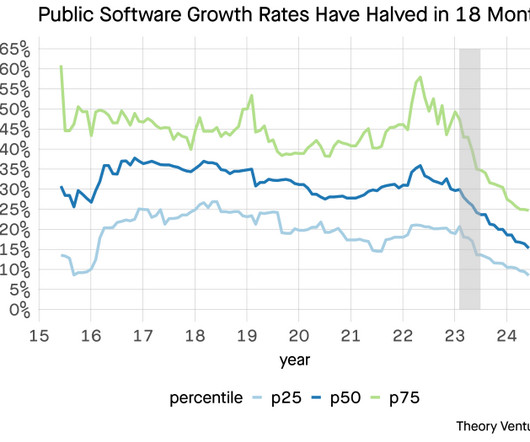

The top quartile companies are growing at slower rates today than the bottom quartile companies in 2016. It’s not to say software spending is slowing (it’s not), or that there aren’t fast-growing businesses (they thrive in the private markets). The median has never been lower in the last ten years.

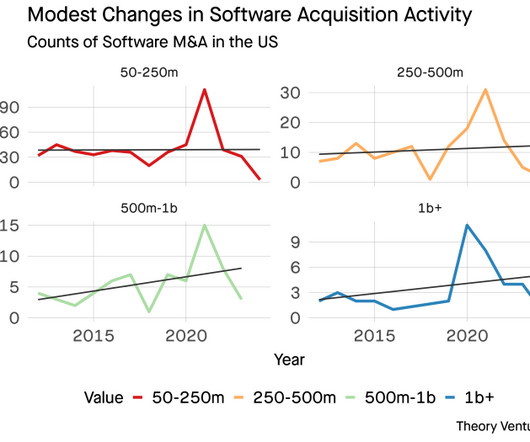

In the last decade, the total number of venture backed software M&A by count has remained relatively constant. Nevertheless, there are huge differences between the total value created by software M&A annually. In 2014, 2016, 2020, 2021, these big mergers drove the figures into the tens of billions. X 2021 43.8%

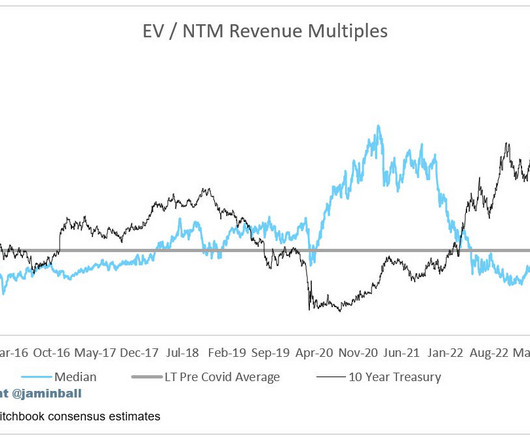

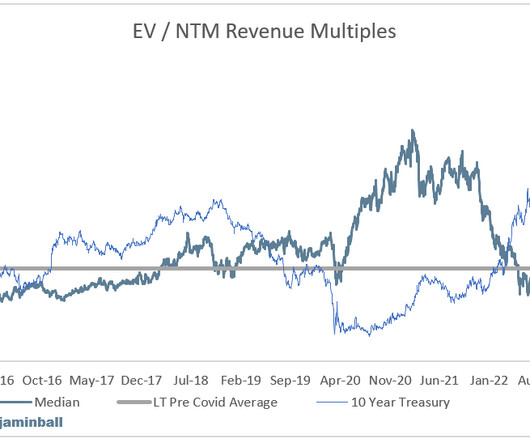

Last week, public software markets suffered significant compression. In 2016, valuations fell 57%. Future revenue ramps have been the dominant driver of software valuations for the vast majority of the last decade. Looking at the changes in software revenue, we see that the market is on a straight line to surge past $100b.

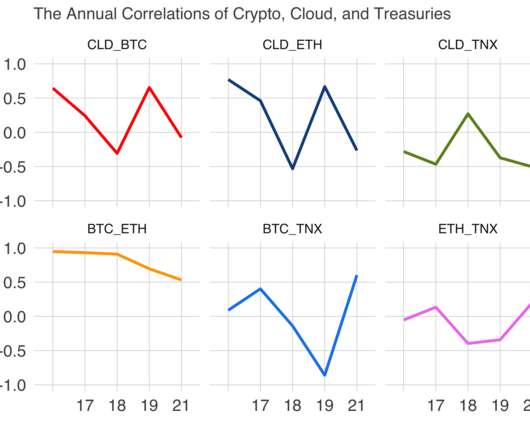

In the last few weeks, public software company multiples have halved. Beyond the most recent cycle, how often do the web2 and web3 software markets move in synchrony? Beyond the most recent cycle, how often do the web2 and web3 software markets move in synchrony? The cryptocoins appreciated much more than software.

In “Do software companies actually have good margins?”, ”, Benn Stancil makes a case for a counterintuitive point : Software companies are much less profitable than they might seem. Because the research & development costs associated with software should be part of their cost of goods sold.

Over the last seven years, software startup investing has changed quite a bit. Since then, many other types of software businesses have been created in new categories like agriculture technology and robotics. In other words, if machine learning startups raised the same amount of money in 2016 is 2010, the chart would show a value of 1.

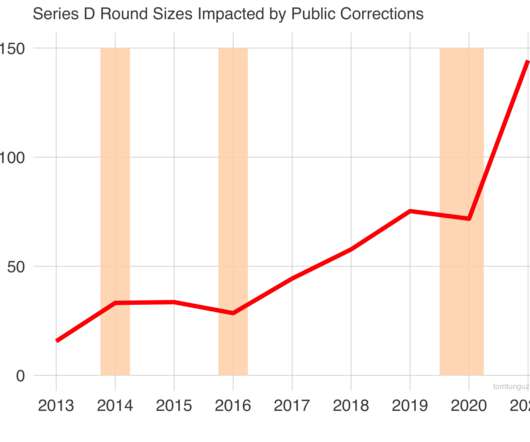

The public software sector is weathering the second deepest multiple contraction in the last decade. Only the 2016 reduction of 57% surpasses it. The question on every software founder’s mind today must be, how will this affect the private financing markets? These are marked in peachpuff orange rectangles above.

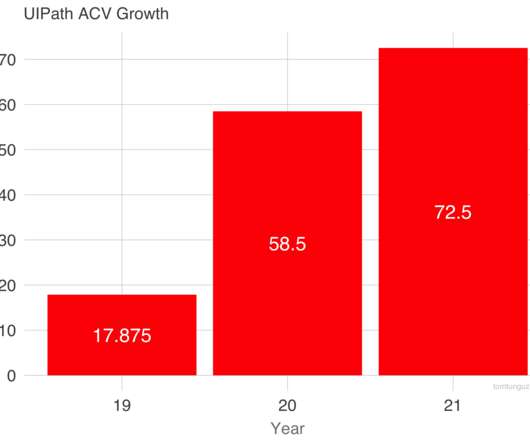

UiPath is one of the most amazing not-really-an-overnight success stories in Cloud, SaaS and software. It was founded way back in 2005 as an outsourcing company, then developed Windows software to automate scripts and more, and turned this into a powerhouse for automating complex functions integrating Cloud and on-prem. 2016: $3.5m

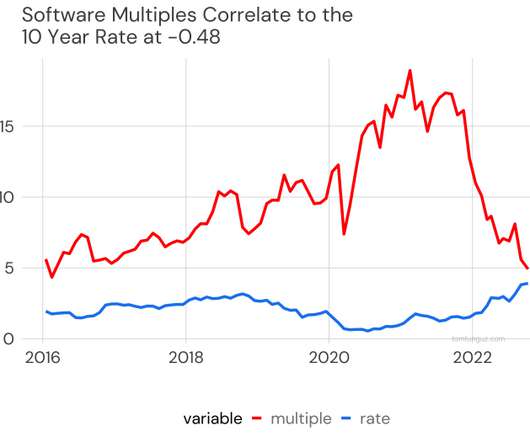

Since 2016, public software has witnessed four corrections. Also, 2014 to 2016 saw a 57% reduction in multiples and of course after 2008. In fact, the 75th percentile multiple has appreciated 25% annually since 2016 and the median has increased by approximately 20%. Today, we’re in the midst of the fifth.

The public software market continues to compress. Enterprise-value-to-forward-revenue multiples are now below 2016 levels for the first time in 6 in years. But it does illustrate the impact of rates on software valuations. It happened in Feburary 2016. The 25th percentile of companies trade at 3.3x today compared to 4.0x

Braze was early to taking a next-generation approach to marketing automation software, focused on being mobile and messaging first. 2016 customer cohort spends 3.2x Blaze’s 2016 customers spend 3.2x more today than they did in 2016. 60% still “counts” as software. more today. 60% Gross Margins.

We can examine the sales efficiency of public software companies to get a sense. Since 2016, the average public software witnessed its sales efficiency winnowed from 52% to 47%, a decline of about 10%. This chart segments the public software companies into the 25th, 50th & 75th percentiles. I observe a few trends.

Most high-growth software investors value public companies on enterprise value to forward revenue multiple. What if we could compare the relative valuation multiples of public and private high growth software companies? What if we could compare the relative valuation multiples of public and private high growth software companies?

2016 has been a year where knowledge has become freely available for anyone interested in knowing about all things SaaS. This slide deck comes from Brian’s brilliant SaaSFest 2016 presentation. In 2017, companies will find success by getting back to basics and focusing on the “service” part of Software as a Service.

50% revenue from software (recurring), 50% from payments (not-recurring). . Half of its revenues comes from its software. Well, if it were 2016, we’d say no. And yes, it’s a software company. Fast forward to day, Merchant Solutions is a much larger share of revenue than software subscriptions.

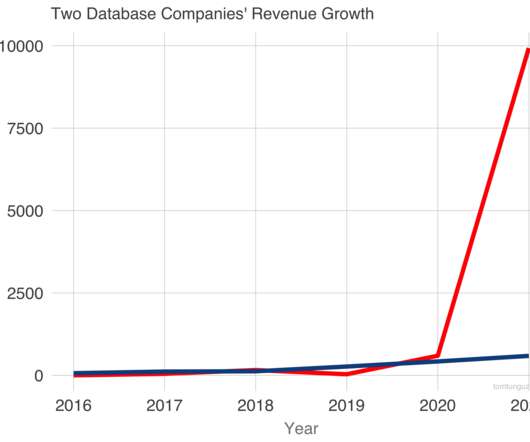

Both startups provide database software to developers to build applications. In 2016, each company recorded less than $50m in revenue. Both of these businesses are publicly traded. Both have grown very fast. In fact, their revenue trajectories through 2020 are nearly identical. In two years, both would near $200m in revenue.

In 2016, I believe they will enjoy a very active acquisition environment. The roughly 60 or so publicly traded software companies hold more than $380B in cash and short term investments on their balance sheets. In 2015, startups benefitted from a vibrant fund raising market.

Update on cloud software multiples, charted alongside the 10Y and 5 year pre-covid NTM rev multiple average. January 2016, SaaS stocks were riding high. It was called 2016: * Everyone panicked * Seemed like multiples would never recover * LinkedIn sold to Microsoft for 7x ARR. pic.twitter.com/JNnzizB82v. But it was just a panic.

2018 is a blockbuster year for software M&A multiples. The growing sizes of the software market. The pace of innovation within software. As I wrote earlier this week, forward software multiples have reached eight year highs at 8.5x Billion-dollar plus acquisitions in 2018 have commanded a median 17.7x EV/NTM revenues.

In less earth shattering news, the fact that it's 2017 also means that my "SaaS Funding in 2016" napkin needs an update. As a reminder, in the original post I tried to give a "back of a napkin" answer to this question: What does it take to raise capital, in SaaS, in 2016?

Which of the 16 major start of categories in information technology will reap disproportionate share of investment dollars in 2016? This may be a breakout category in 2016 for Series A investments. Given the amount of seed investor interest, I expect many of these marketplaces to raise series A dollars in 2016.

I don’t do a lot of predictions, but I very strongly believe enterprise software companies are going to do really well over the next 18/24 mos…. It’s not slowing down Salesforce, Snowflake, or almost any other SaaS or Cloud leader. Salesforce Growth: 2023 $31.8B (guidance) 2022 $26.5B 2021 $21.25B 2020 $17.1B 2014 $4.1B. Thank you Ohana!

UIPath offers software to build robots, programs that automate repetitive work. The UIPath suite includes the software to write, execute, monitor, and maintain these robots. The company also mentions the 2016 cohort of customers expanded 51x in the last 5 years. Some examples include streamlining customer onboarding.

And they are both incredibly impressive — 118% growth at $3B run-rate and $500m in ARR in software alone may be an all-time record — but also, perhaps not SaaS? #1. With gross margins of only 21%, is Toast really a software company? Wix just has more software revenue to blend the total margins higher.

UiPath has had an incredible history, taking 10 years to get to that first $1m in ARR … and then turning into one of the fastest growing software companies to $1 Billion in ARR ever ! 2016: $3.5m 2016: $3.5m UIPath History 2005: Started as a tech outsourcing company 2014: $500k rev. seed round 2015: $1m rev.

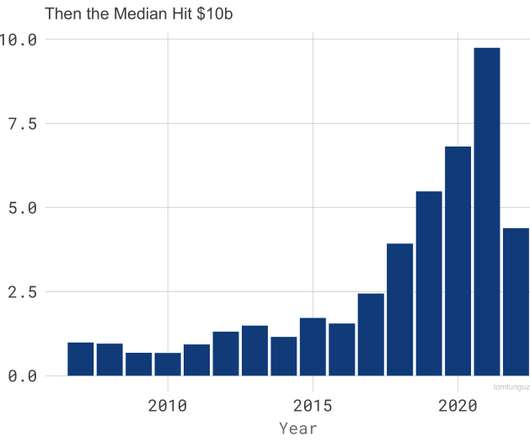

From 2007 to 2016, $1.5b marked the upside case for most VC software and infrastructure investment memos. The silver lining: the median public software company in 2022 is three times as valuable as in 2015, which suggests valuations should settle higher than that era. Fewer than 15 SaaS companies traded on public exchanges then.

Shopify’s first quarter revenue: Q1 2021: $989 million Q1 2020: $470 million Q1 2019: $321 million Q1 2018: $214 million Q1 2017: $127 million Q1 2016: $73 million Q1 2015: $37 million Q1 2014: $19 million Q1 2013: $9 million. Shopify doesn’t call its non-software revenue “MRR” A small but interesting note.

But importantly, it’s raised its ACV 4x since 2016. Example: quiet SaaS learning software Docebo: pic.twitter.com/jtGwErBPu6. Docebo’s pricing is on the “corporate” side of LMS. It doesn’t compete at the bottom of the market, and targets top logos with a reasonably priced product. Yes, you can.

2016 was a year of change for SaaS, and most of the story was the public market. The Hottest Startup Sectors In 2016 - published on January 3rd, this post reviewed the patterns of investment in startups, and in particular, the sectors where investors were increasing their investment the fastest. The end of the year is fast approaching.

“Salesforce’s IPO is also seen as a test of a new business model that could shake up the software industry. The company is the poster child for subscription-based software, a model that’s gaining popularity among corporate buyers. In 2016, Digital Ocean opened a $130m credit facility with Keybanc. .

A massive amount of IT spend has not just moved to SaaS over the past decade, but almost as importantly, the % spent on business software by IT has also gone up. This will be the start of the end of the sweetheart run for SaaS from 2015–2016 through today. “No No code” enables much better software. “No But this can’t last.

There are several big leaders in property management software, and AppFolio is one of them. At $660m in “ARR” (a lot of that isn’t software, as we’ll see below), it’s trading at a $7.2 AppFolio is what the markets want in a software+ company, at least in 2023. Let’s dig in.

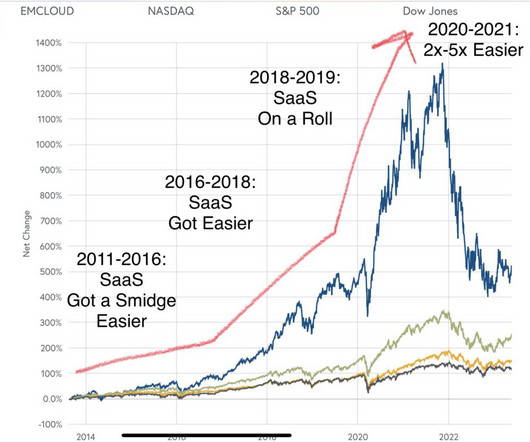

Not easy, but easier and easier: There was a bump in 2016, a Flash Crash in SaaS, when budgets were slashed, but it didn’t last long enough to really impact renewal cycles.

To illustrate the turbulence, consider the following metrics: The BVP NASDAQ Emerging Cloud Index (the public benchmark of software performance) has contracted by more than 40%. Cloud 100 multiples have fallen in 2022 –– ARR multiples rose nearly fourfold from 9x in 2016 to 34x in 2021 and down to 30x in 2022.

Every week I’ll provide updates on the latest trends in cloud software companies. For software, all eyes were on Azure - which grew 31% YoY (ahead of expectations closer to 29%). This is good news for the broader infrastructure software universe. Follow along to stay up to date! I have to “swag” this a bit.

Founded in 2016, Lark effectively combines messaging, schedule management and online collaborative documents in a single platform. Our mission at Vanta is to be a layer of trust on top of cloud services, to secure the internet, increase trust in software companies, and keep consumer data safe.

As a core part of Matt’s philosophy, people need to have their own domain and run open-source software because it allows them to control the entire stack of what they’re putting online. Automattic was started in 2005 to democratize publishing, and WooCommerce was purchased in 2016 to democratize e-commerce.

Through the end of July in 2016, $70B worth of SaaS companies sold. First, 15 of the 22 US software acquisitions worth more than $0.5B The largest private software acquisition is Transfirst, a payment software business founded in 1995. Perhaps the fastest growing software companies aren’t interested in selling, yet.

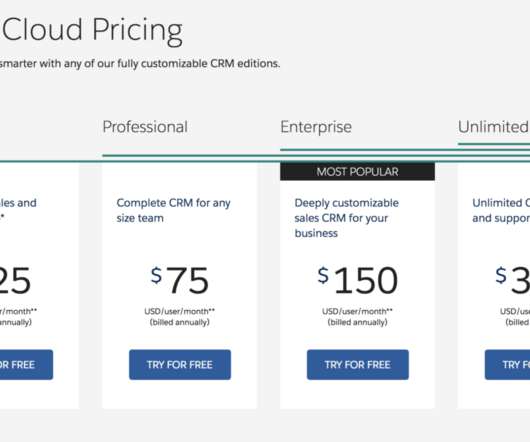

You could spend days reading about pricing and pricing strategies in software on the web, but a lot of this content doesn’t really hit one, basic fundamental point — there is no real reason any particular piece of software should cost anything in particular. Real software has basically zero core cost to deliver.

The chart above shows the most recent enterprise value to forward multiple for a basket of next-generation software companies. The worst of them was in February 2016 when multiples fell by approximately 60%. Last week, SaaS stocks fell by about 18% on average. As of Friday, the median forward multiple is 9.3x

Every week I’ll provide updates on the latest trends in cloud software companies. Some of these drops rival one of the worst ever software earnings reaction of Tableau in 2016! On Thursday the software index (WCLD) was up ~3%! So what’s holding up software stocks valuations?? Atlassian was down ~10%.

The increasing focus on vertical software startups shouldn’t be surprising. Many of the most of apparent and immediate opportunities in the software market have been filled by now SaaS incumbents. Artificial intelligence is to be a big trend in the SaaS world, a theme that matured in 2016 but will very much continue through 2017.

When I analyzed the SaaS fundraising market in 2016 , three trends emerged. Across all rounds, both lines are up into the right, despite some volatility in 2016. In 2016, venture capitalists reduced their investment in staff companies by 1 ⁄ 3 , falling to $2.8 Meanwhile, round sizes swelled. billion from $4.2

As the overall venture market environment evolves in 2016, so too does the SaaS and Software segment. The number of Series A, B, C, and D investments in software companies stabilized at roughly 170 per quarter from mid-2013 through mid-2015, before falling 17% in Q4 2015 to a two year low.

We organize all of the trending information in your field so you don't have to. Join 80,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content