This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Today is January 10, 2017. In less earth shattering news, the fact that it's 2017 also means that my "SaaS Funding in 2016" napkin needs an update. Today I'd like to take a stab at the (early) 2017 answer to that question. So, what does it take to raise capital, in SaaS, in early 2017? Here's the 2017 SaaS Funding Napkin!

And this data implies that fewer earlier stage companies raised, which means there will be fewer Series Bs in 2017 and fewer Series Cs in 2018. Despite this increasing amount of capital on investor’s balance sheet, 2016 was a slower year by round count.

It didn’t get the buzz I think mainly because it’s a “Re-IPO” Sailpoint first went public in 2017, then Thamo Bravo took them private in 2022, and now public again in 2025! Sailpoint x Thoma Bravo story is incredible Sep 2014: Thoma Bravo acquires VC-backed Sailpoint Nov 2017: TB takes Sailpoint public at ~$1.1B

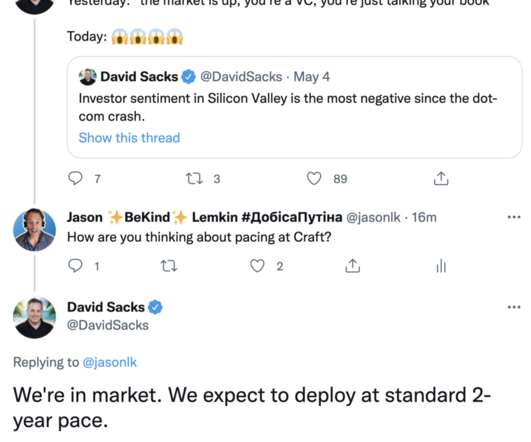

So Carta has some of its latest data on VC performance and it’s pretty interesting: There’s a lot going on this chart but let me break it down from a founder perspective: The median 2017 fund is 7 years into a 10-14 lifetime — and is sitting at 1.8x “TVPI” But it’s not quite that good. So back out 20%.

Think your customers will pay more for data visualizations in your application? Five years ago they may have. But today, dashboards and visualizations have become table stakes. Discover which features will differentiate your application and maximize the ROI of your embedded analytics. Brought to you by Logi Analytics.

Then, in 2017, with around $50M in revenue, BILL added payment capabilities. You have to keep going when you’re doing something that wasn’t done before. There was an inflection point for BILL around 10k customers. The network was growing, and they saw real virality. That was probably 2012. BILL network has 7.1M

I went through my archives and found this post from 2017 that showed that the most expensive stock at the time was Veeva at 11.7x If the valuation environment mirrors 2017, CloudFlare’s multiple would halve again. In 2017, the average company traded at 5.4x Today, CloudFlare tops the list at 22.2x.

After the correction earlier this year, public valuation multiples had reset to those of 2017. Before this announcement, US venture-backed software M&A was tracking to its worst year since 2017, at about $7b, down from $71b last year. Congratulations to team Figma on building their impressive business.

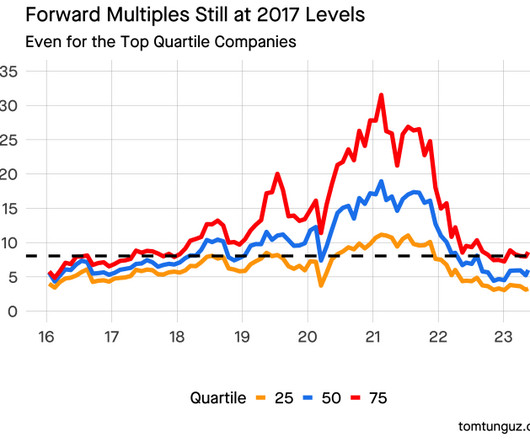

The rest of the top quartile has remained depressed, suppressing the cohort to 2017 levels, just as they were last year. But rally hasn’t convincingly beaten the black line representing the 2017 median. These top five stocks explain the most recent earnings upward in the chart above.

From $8 billion in market cap in 2017 to $117 billion today! A $2 billion market cap is amazing. But $20 billion is now becoming “common”, if that term can be used. Shopify is the crazy one. Most of these names were worth a fraction of their current market cap at IPO. Zendesk IPO’d at $1 billion.

Early businesses tend to create more instruments to hire, grow, and incentivize. tokens resemble equity in most ways, but possess one additional function: they can be used to pay for service. Trailing 2 Year Inflation Rate. Founded Year.

60%+ of our speakers have been less represented speakers since 2017 and all our IRL events since 2017 have had a majority of women speakers.W. Submit for any of our events here. Please also review our detailed guidelines here. In a nutshell: We prioritize diversity. We require fresh content and perspective. No repeats.

One of the crowd favorites has been Mark Roberge, all the way back to 2017. 2017: How the Best Outbound Sales Teams Are Managed. Mark first joined us in a terrific panel session on how the top outbound teams are managed, 2018: Sales Mistakes that Can Kill Your SaaS Business How to Avoid Them. Ok, now a look back!

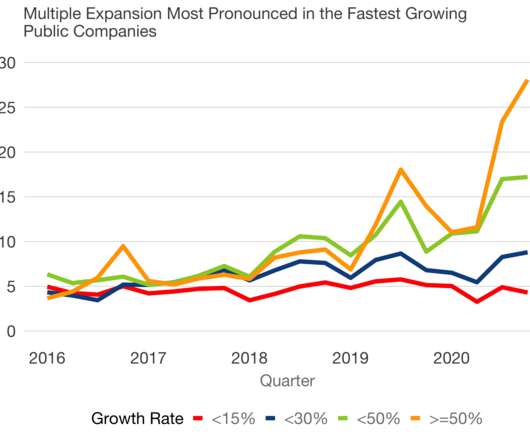

In 2017 and 2018, the median high-growth private company raised at a higher forward ARR multiple than in the public markets. Let’s excise this group of 50% growers from the rest and add Redpoint internal data for forward ARR multiples for later-stage companies, which are all growing above 50%.

And here’s a fun look back to the very first Plato event, back in SaaStr’s original CoSelling Spacem in 2017! They have sessions and roundtables with the VPEs and CTOs of Atlassian, Datadog, Gusto, Box, Coda, Safegraph, Headspace, Flatiron, Lyft, Superhuman, Netflix, PayPal and so much more! It’s epic. Sign up here.

The Rebrand That Changed Everything 2017’s pivot from dapulse to monday.com wasn’t just a name change. Product-Led Growth Before It Was Cool While others were building massive sales teams, Zinman pushed for a product that would sell itself. The result? ARR growth?

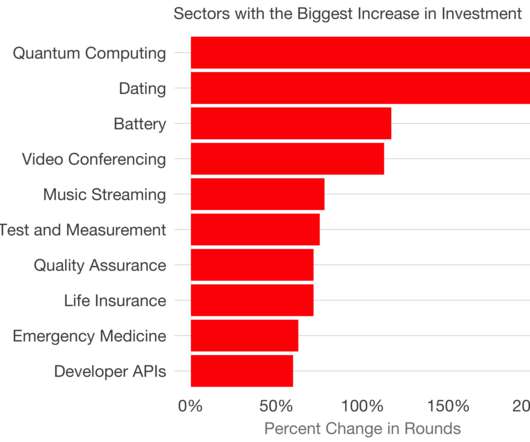

Here are 2015 , 2017 , This year, I was certain the categories would have been influenced by COVID19. From time to time, I chart the fastest growing categories of startup investment in the US for seed through Series C.

The point is that SaaS multiples are still higher than where they were from 2010-2017. Draw a straight line and assume multiples gradually expand at the same rate as they were growing from 2017-2019. The Bear Case: Multiples are still elevated compared to the pre-2018 period. It just went nuts during Peak Covid.

It’s not slowing down Salesforce, Snowflake, or almost any other SaaS or Cloud leader. Salesforce Growth: 2023 $31.8B (guidance) 2022 $26.5B 2021 $21.25B 2020 $17.1B 2014 $4.1B. Thank you Ohana! pic.twitter.com/CMhrBXgHSF. — Marc Benioff (@Benioff) May 31, 2022. We may be headed for a big downturn, we’ll see.

I didn’t calculate this figure in 2017. (note I’m switching from median to average here). In 4 years, we’ve seen a 4x increase in the median MRR of a Series A SaaS company. That’s quite a growth rate. There are two reasons for this increase.

Today, the public markets value companies like it’s 2017. At 28 employees, a $16m Series A fueled the company for 35 months. That’s a lot of buffer to achieve Series B metrics [1]. But we’re no longer in 2021.

Prior to Shopify, Kaz was the Product Lead for Payments and Billing at Facebook and was the former CEO of Kash, a payment technology company that he founded and which was acquired in 2017. During the conversation, we’ll discuss: What does the future of financial services look like?

So the minor point is maybe we’re just back to 2016-2017 in SaaS venture capital for Series A and later rounds. For the best ones. But the bigger point is especially for new founders and execs to just look at the chart above. We’re never “going back” to how things were in late 2020 and 2021.

In 2017, the industry migrated from ASC 605 to ASC 606, which are financial arcana as esoteric as it reads. If that argument is correct, then the average gross margin of a software company in the public domain would fall from 72% to 47%. Quite a stark difference. Profitability for software companies isn’t straightforward.

CEO and co-founder Bill Magnuson was CTO until 2017, then took over as CEO from a co-founder, and owns 4.5%. Bull Wall Street seems fine with it. 60% still “counts” as software. 1,000 employees at $250m in ARR. A good yardstick for more enterprise-focused SaaS. Dilution added up over the years, with Magnuson owning 4.5%

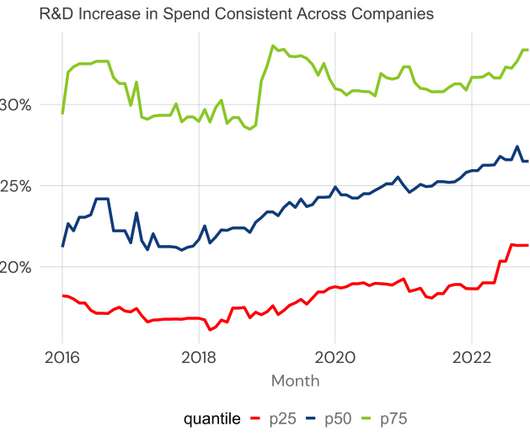

Starting in 2017 when the data is richer, the PLG companies increased R&D spend from 27.5% I categorized these companies by their primary motion: sales or product-led. Sales-led companies have oscillated around the 25% mark. However, PLG companies are a different story.

In 2017, SaaS companies reported their cost of customer acquisition had increased by 65% in the previous five year period. What happened to these figures during Covid? We can examine the sales efficiency of public software companies to get a sense.

Salesforce Growth: 2021 $20.8B Guidance 2020 $17.1B 2014 $4.1B. Thank you Ohana! — Marc Benioff (@Benioff) August 25, 2020. If you haven’t done a SaaS start-up before, it’s different. The reasons are many, but I think they can almost all be summed up in one key factor: SaaS compounds.

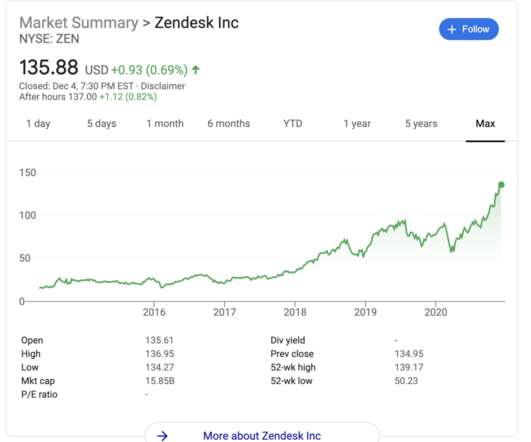

Worth $2B by 2017. $200m from Silver Lake. 2016: IPO at $1.15B market cap. 2020: Worth $7B today. Zendesk : Founded 2006. Raised $500,000 (!) in first angel round in 2007. IPO in 2014 at $1B. Crossed $1B in ARR in 2020. Today worth $16B. Obviously, these are outliers. And revenue has grown to $1B+ ARR for all the winners.

That’s way, way up from just 22% of revenue from $100k+ deals in 2017. He was granted an additional 3m shares in 2017 and 1.3m Today, Slack has 575+ customers paying more than $100k a year, which important now accounts for 40%+ of its revenue. The S-1 is full of enterprise case studies, from Oracle to Fox to Splunk. more in 2019.

We’ve had a majority of women speakers since 2017, and aim for 66% less represented speakers. So for 5+ years we’ve had a very specific set of speaker guidelines at SaaStr Annual and related events. We’re not close to perfect and keep learning. Since Covid hit though, we did a lot of digital events.

rev 2017: $30m rev. UiPath has had an incredible history, taking 10 years to get to that first $1m in ARR … and then turning into one of the fastest growing software companies to $1 Billion in ARR ever ! UIPath History 2005: Started as a tech outsourcing company 2014: $500k rev. seed round 2015: $1m rev. 2016: $3.5m 2018: $155m rev.

But over time, it’s added a large enterprise and B2B component for marketers and others to track, manage and market videos that we’ll spend a bunch of time digging in on, as it’s the fastest-growing segment, growing from little-to-none in 2017 to 25% of revenue today. 5 Interesting Learnings: #1.

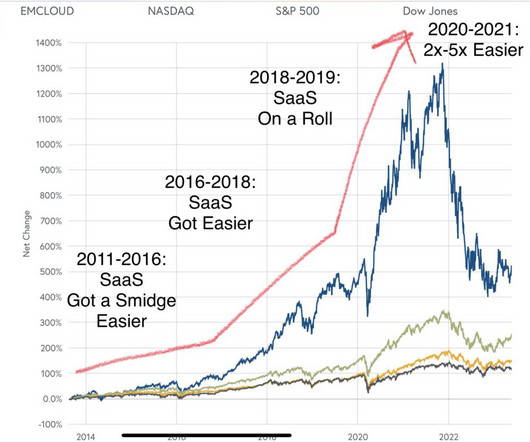

Each year from 2017-2021 was easier than the prior year. The biggest issue though is how long it just got easier and easier. Now we have a whole generation of SaaS employees and execs who have only seen SaaS. Get Easier Every Year. 2022 was harder, but it took a while to see it wasn’t transitory.

#1 source of traffic to [link] : 2022: SEO 2021: SEO 2020: SEO 2019: SEO 2018: SEO 2017: SEO 2016: SEO 2015: SEO 2014: SEO 2013: SEO 2012: SEO. Even Year 1 pic.twitter.com/5FtzBG2v1O. — Jason BeKind Lemkin #???????????? jasonlk) March 15, 2022. So we’re coming up on Year 10 for SaaStr!

In 2017, he was named by LinkedIn as one of the top 5 CMOs in the world to follow for thought-leadership in the digital marketing domain. Chandar also spent years at Andersen Consulting (now Accenture) as a strategic advisor to Fortune 500 companies. He is a Strategic Advisor to the CEO of Freshworks.

Where it Went: $45m revenue in 2017 and reported $100m+ in 2021, but acquired for modest sum in 2021. Where it Went: Acquired for $850m+ by Sage in 2017. Thought this would be about $50m. Where it Went: A $7B market cap and IPO. 557 SEOmoz. in 2011 GAAP revenue. Boy, there is just so much money in marketing. 563 Demandware.

This led to our first meet-ups in 2013 and 2014, the first SaaStr Annual in 2015 , the industry’s leading podcast in 2016, the first SaaS founder coworking space in 2017, and SaaStr Pro , the first learning management system for SaaS founders in 2018. 2017 The Third SaaStr Annual: Scale Together.

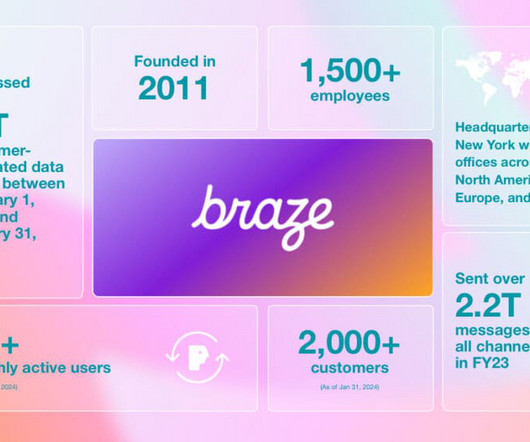

This was around 2017, and CS became simpler and focused on post-sales, retention, and reduced churn. This revenue chart is 2017-2021 before Braze IPO’d. They hired tech support people, and they got re-entrenched into the zero-to-one building mindset rather than the rest of the CSM function, which already had a little scale.

First $100k customer in 2017. GitLab China is a new independent company formed in 2021, both SaaS and self-managed, available only in China, Hong Kong and Macau. We may see this more often. #4. Then 20 by 2018. And 100 by 2020 and 200 by 2021. GitLab lays out a terrific chronology that is similar to how many of us learn to go upmarket.

Up until say 2017–2018 or so, in SaaS, there was a rough rule: a relatively small amount of secondary liquidity ($1m-$2m) would be offered by growth investors in top VC rounds once a startup crossed $10m ARR or so. Dear SaaStr: Can Founders Still Sell Some of Their Shares in Venture Rounds in 2023?

from 2015 to 2017, a compound annual growth rate of 35%. In 2017, Dropbox generated more than $300M in free cash flow from ops, and for the past two years has sustained 30% cash flow from ops margins. MC/2017 Rev Multiple. Dropbox has grown from 0 to 500 million users over that time period. COGs stands for cost of goods sold.

It seems like every market in SaaS is even bigger than we expected, and importantly, able to not just hit $1B in ARR but accelerate afterwards. Seize the day. Salesforce Growth: 2022 $26B (guidance) 2021 $21.25B 2020 $17.1B 2014 $4.1B. Thank you Ohana! From 1st Earnings Call Inside. We’re all vaccinated!) pic.twitter.com/DQAwBNHm2A.

We organize all of the trending information in your field so you don't have to. Join 80,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content