This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

How far along was the typical SaaS Series A in 2018? The chart below shows a representative sample of SaaS Series As’ ARR and projected ARR growth rate for 2018. The median business was at $1.8M in ARR and growing at 250%. Breaking this down a bit more into quartiles, the ARR quartiles were: 25th.

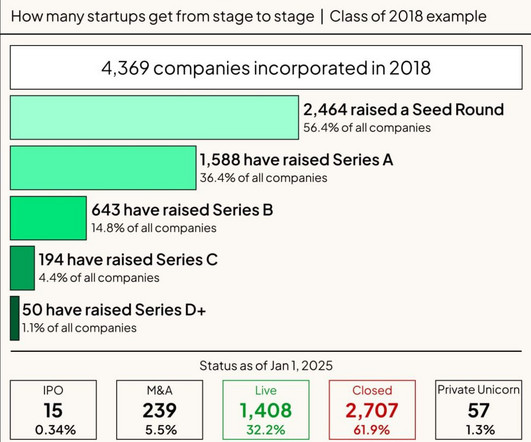

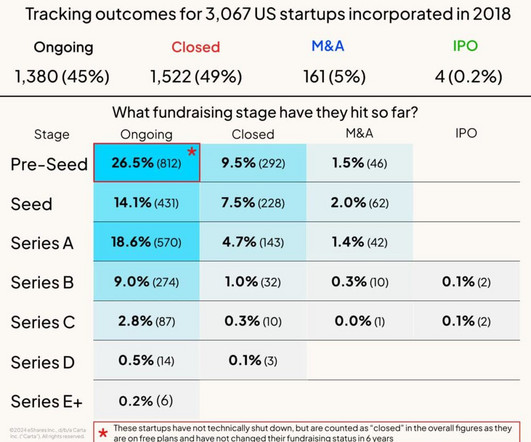

So Carta has some interesting new data from all of its start-ups from The Class of 2018 here. Every start-up dataset is a bit different. Some are broader than Carta, some narrower, but Carta is a good proxy for typical tech start-ups that raise a seed round. And what happens after that seed round? Within 7 years, 62% of start-ups shut down.

The Core Problem: Mobile Changed Everything The Market Forces at Play: Consumer attention was fragmenting Traditional marketing channels were losing effectiveness Mobile shopping sessions exploded: 2014: 15% of shopping on mobile 2018: 40% of shopping on mobile 2024: Nearly 75% of shopping on mobile The Marketing Crisis: Lower ROI on existing channels (..)

I’m fortune that SaaStr Fund was the first investor in RevenueCat in 2018 and today it’s grown into the #1 tool to manage mobile subscriptions, powering 40% of all mobile subscription apps, and even ChatGPT’s mobile app itself. So they see 40% of all mobile subscriptions — and a ton of data from it.

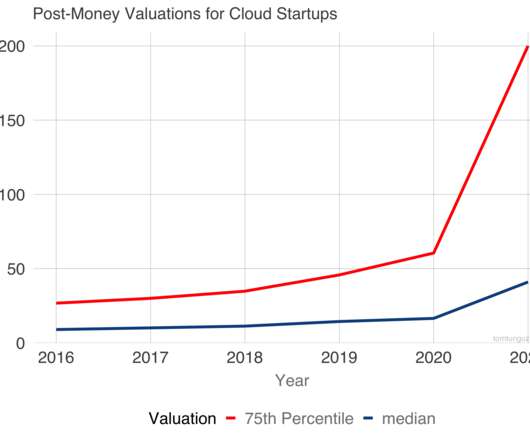

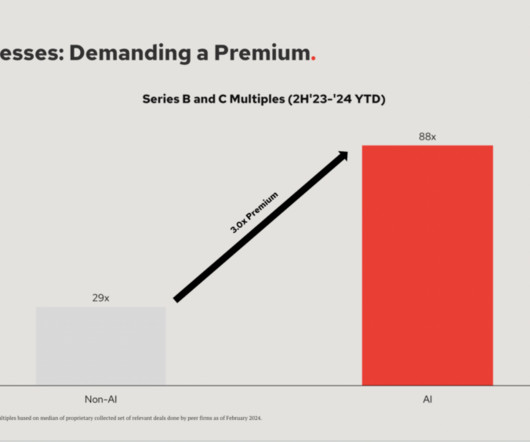

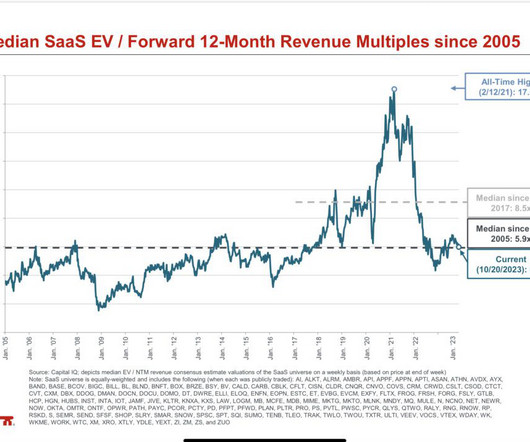

It hovers around 5x until 2018, then spikes to 8x, and despite some volatility, reaches its current zenith at a bit more than 10x. In 2017 and 2018, the median high-growth private company raised at a higher forward ARR multiple than in the public markets. The valuation multiple has doubled in about two years. This is a critical shift.

We are proud that the 2018-2024 SaaStr Annuals have featured over 50% women and multicultural speakers at each event. SaaStr is committed to having the most inclusive community in Cloud, SaaS and AI.

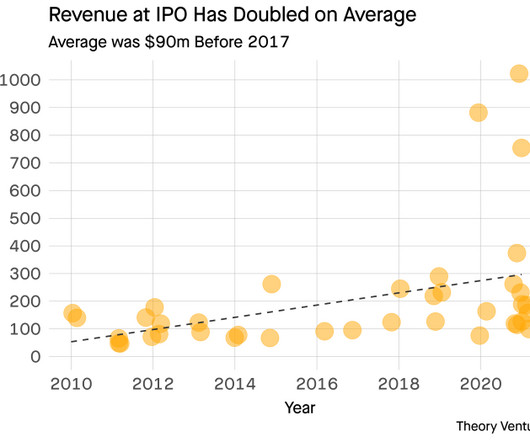

Before 2018, only one company IPOed with more than $200m in revenue. If we divide the data set into two eras : before 2018 & 2018 onwards, we see a clear shift in the average revenue at IPO & the difference is statistically significant with a p value of 0.0063. In fact, the median revenue at IPO at $90m.

In 2018, most Datadog customers used 1 product. 28% of Datadog’s customers use 4+ products, but they make up the vast majority of revenue: And 75% use 2 or more products, up from just 15% in 2018: #4. More product, more products, more products. 10 new products this year. Customers don’t buy all the products at first.

The Bear Case: Multiples are still elevated compared to the pre-2018 period. So they can fall another 20%-30% just to revert back to that mean: SaaS was already on a tear starting in 2018. The argument here is that SaaS even in 2018 was overvalued. You can see a lot of VCs and others talking about this on Twitter.

And so, Cloud multiples have rationally fallen back to where they were in 2018 and 2019. The argument here is multiples have fallen too far, since the best SaaS and Cloud companies are growing so, so much faster than in 2018 and 2019. Multiples exploded when we all lived in the Cloud, quarantined in whole or in part in the Cloud.

Smartsheet went public in 2018. Let me know which you prefer. SmartSheet. TTM Revenue, $M. Revenue Growth. Gross Margin. Net Income Margin. -48%. Cash Flow Margin. -44%. Since its IPO, Smartsheet has increased its market cap 2.6x today, which is a favorable omen for Asana.

Shopify’s first quarter revenue: Q1 2021: $989 million Q1 2020: $470 million Q1 2019: $321 million Q1 2018: $214 million Q1 2017: $127 million Q1 2016: $73 million Q1 2015: $37 million Q1 2014: $19 million Q1 2013: $9 million. NRR of 110%+ since 2018 — sort of. — Jon Erlichman (@JonErlichman) April 28, 2021.

jasonlk) January 18, 2018. #3: jasonlk) September 21, 2018. #4: jasonlk) February 25, 2018. #5: jasonlk) February 25, 2018. #6: jasonlk) September 6, 2018. #7: jasonlk) January 14, 2018. #9: jasonlk) October 3, 2018. . — Jason BeKind Lemkin #???????????? Remind me the other rules again.

Since Paychex acquired Oasis Outsourcing in 2018, Oasis PEO is now a part of the Paychex brand. Currently, the Oasis professional employer. The post Oasis PEO Review appeared first on The Daily Egg.

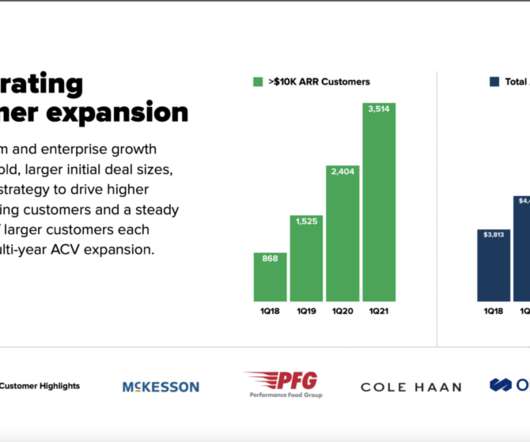

While Sprout Social has “only” added 13% new customers each year since 2018, those customers even with 110% NRR compound, leading to 32% ARR Growth. In 2018, even at $75m in ARR, Sprout Social only had 868 $10k+ customers. A reminder of the incredible power of NRR of 110% over say 100%.

In 2018 at Saastr, Jason Lemkin & I talked about private equity becoming an increasingly aggressive buyer of venture-backed software companies. Last year, private equity firms inhaled $29 billion dollars’ worth of startups - a twenty-year record and 50% more than the previous peak.

This chart shows the median and the 75th percentile of enterprise value/forward revenue multiple for the basket of public stocks which were public at that moment in time. Correction Year. These corrections reduced valuations by between 30% and 60%. These undulations are short-lived.

Early businesses tend to create more instruments to hire, grow, and incentivize. tokens resemble equity in most ways, but possess one additional function: they can be used to pay for service. Trailing 2 Year Inflation Rate. Founded Year.

From $1B Valuation in 2018 to $20B+ Today. But remember it hit a $1B valuation just in 2018. 300 Employees Working on AI Not a surprise, but interesting to see the scale of investment here. #5. Even With Today’s Multiples. In a world where unicorns are struggling, Canva isn’t one of them.

And again, Dec 31, 2018 and Dec 31, 2019. And again in 2018. A Bad Day: When I Had No Salary And Didn’t Get My Requested $10k Bonus Even Though I Brought In an Extra $300k All-Cash Upfront Deal. A Good Day: Dec 31, 2009; Dec 31, 2010; Dec 31, 2011; Dec 31, 2012. When we killed it every year on the last day of the year.

Cloud has been on an incredible tear since 2012 or so, and then even more since about 2016, and then as you can see above, went into hyperdive in about 2018 … and then into true warp speed after Covid. But does it even matter? SaaS and Cloud are up +1000% since 2013. That’s better than almost any venture fund.

Raising a Series A is as hard as it’s been since 2018 is the answer. Not at all: Per there data, there is some modest pick-up at Series B and C , but that’s less relevant to most founders. What’s most important is after a seed round … how hard is it to raise another round? This just makes sense.

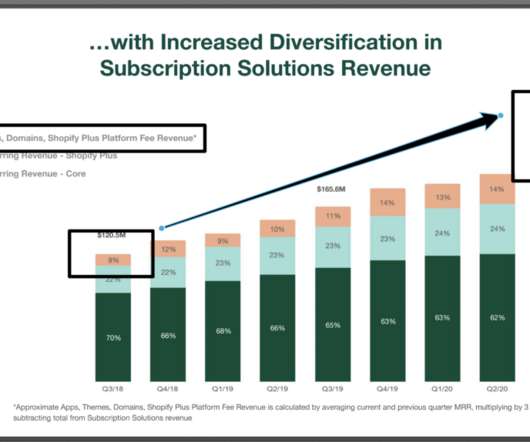

Shopifys partner revenue grew from 8% in 2018 to 20% by 2020, but it took years of investment to get there . Its not a quick win. For example, Salesforces partner ecosystem didnt become a major revenue driver until a decade after the company was founded. Expect your sales cycle to double when working with partner s.

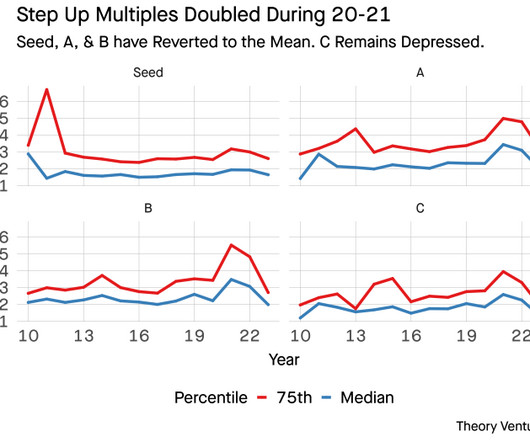

In 2024, I expect most of these figures to revert to the mean - not the peaks of 2020-2021, but more akin to 2018. In almost every category, the time between rounds is also at decade highs. The public valuation environment & pace of venture capital investments mirror those years better than others.

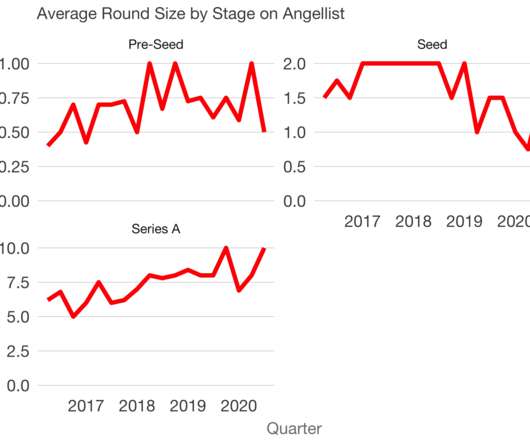

We see pre-seeds have fallen from mid-2018 highs of $10m to about $5m. Second, round sizes are down about 20-30% from highs in the pre-seed and seed market. Series As’s ascent continues unperturbed. Last, the Angellist team provided data on pre-money valuations, which is rare data! Seeds persist at $10m pre-money.

It’s just they sort of have reverted to in many cases as hard as they were around, say, 2018. Folks are still struggling to get used to it. It’s not so much that things are a lot harder now. A lot of folks just don’t want to work hard anymore.

So Carta put out some recent data I found very useful on how many startups raise another round, and how many sort of quietly wind down, in the first 5 years or so after being founded (from 2018 to early 2024): Almost none IPO’d in the first 5 years, but that just makes sense.

As of 2018, the average eCommerce website — both globally and in the US — converted less than four percent of its visitors. eCommerce vendors who aren’t actively improving their landing pages to convert more visitors are almost certainly leaving money on the table.

You can see that fast and steep drop-off from the Q4’21 peak here: It looks particularly dramatic when you zoom into just late 2021 and 2022: But second, really, in many ways it seems like we’re just back to 2018-early 2020 in venture. Let’s look at 2018-202 0. Back to before the Covid Crazies in venture.

We’re proud to have > 60% women and multicultural speakers at the 2019 and 2018 SaaStr Annuals, and we are on track to meet or exceed that again in 2020. Our 2019 and 2018 attendee Diversity and Inclusion programs were fully subscribed and worked well, so we want to go even bigger this year on a number of levels.

It’s not slowing down Salesforce, Snowflake, or almost any other SaaS or Cloud leader. Salesforce Growth: 2023 $31.8B (guidance) 2022 $26.5B 2021 $21.25B 2020 $17.1B 2014 $4.1B. Thank you Ohana! pic.twitter.com/CMhrBXgHSF. — Marc Benioff (@Benioff) May 31, 2022. We may be headed for a big downturn, we’ll see.

Now this isn’t new in venture, but 2017-2018 actually were pretty good times to invest. That gets you to 3x after fees to the VC’s own investors. That’s what it takes to beat Nasdaq materially. So the media fund isn’t close to hitting its goal. And there is still time.

We are proud that the 2022 SaaStr Annual featured a combined 60% women and multicultural speakers and have had over 60% women and multicultural speakers at each SaaStr Annual since 2018, and we hope to do even better in 2023! Our core goals and values at SaaStr include: Putting on the most inclusive events in the industry and.

HubSpot is now on its way to $2B in ARR, but Dharmesh looks back on how they went from startup to scale-up: 2018: Dharmesh came back for the 5th Annual with Chief People office Katie to do a deep dive on how to drive up employee retention, and create values that endure.

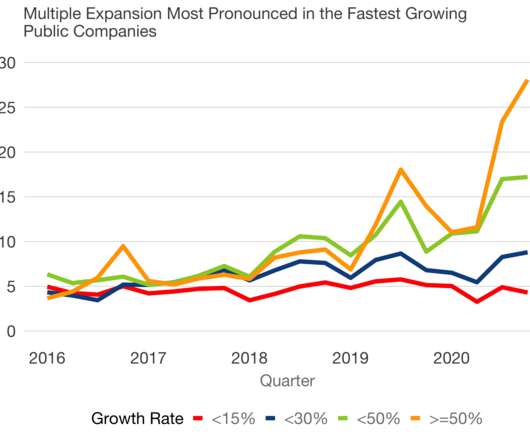

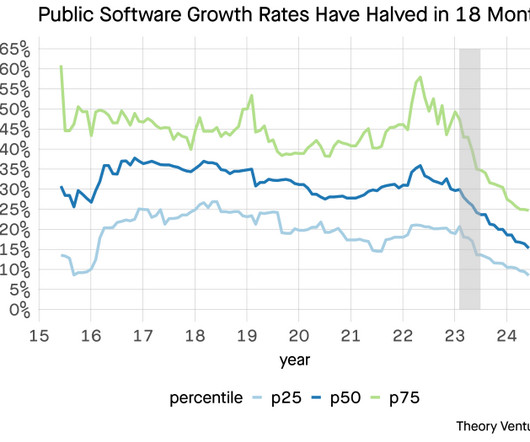

Top quartile companies in 2024 grow at the same rates as bottom quartile companies in 2018. Each of these percentiles is now meaningfully lower than the average over the past decade. Future revenue ramps have been the dominant driver of software valuations for the vast majority of the last decade. When they fall, valuations compress.

February 2, 2018: I shared this post on LinkedIn: I’d started a new job, lucked into the opportunity to advise two founders and companies I think highly of, and committed to pushing forward on a passion project of mine that had stalled for 10 years (kids books about social and environmental issues).

2018: 68 attendees at SaaStr Miami Meet-Up. #2. In 2018, it seems like everyone at our meet-up was either sub-$1m ARR … or had driven or flown in. 2019: 184 attendees at SaaStr Miami Meet-Up. More importantly, the attendee quality has gone way, way up over the years. There just weren’t that many in Miami even in 2019.

Those multiples went up in 2018 and 2019, and things were Better. But I think a lot of us are betting on a return at least to 2018-2019 multiples. The reality is, as you can see in the above BVP chart, the Median public SaaS company — a pretty high bar right there — has traded around 6x ARR. To a 8x-10x world.

Top tier SaaS companies are valued at 34x ARR today, up from a pretty consistent 10x or so through 2018. Valuations are at an all-time high — but you have to bring the growth. That’s incredible multiple expansion. But only the best SaaS and Cloud get these multiples. M&A isn’t keeping up, at least not yet.

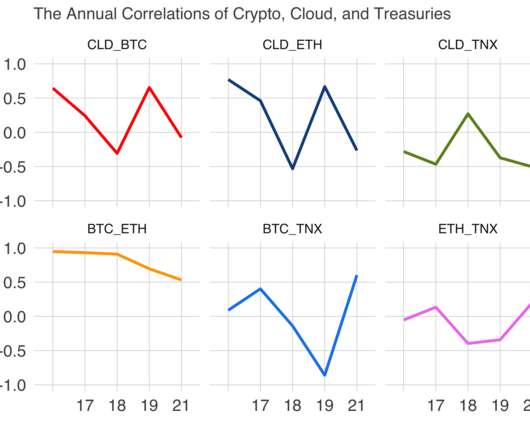

BTC and ETC moved more or less in synchrony from 2016 to 2018. Economics students would argue the discounted cash flow model predicts this behavior. Companies with profits in future years should be less valuable during times of higher interest rates. Three years ago, they went their separate ways.

In 2018-2019, it grew then a bit, and for very top SaaS companies, 20x ARR wasn’t uncommon for Series A and later rounds. For years, the standard was “about 10x” Top tier SaaS companies would tend to raise at around 10x ARR, with ones with slightly lower growth often raising at 5x. And then things just went crazy.

By 2018, it felt like about 50%. MongoDB, Datadog, and others have given New York a stronger and strong place in SaaS and Cloud. In 2013, everyone that could come to the Bay Area to run a SaaS company, did. And yet … and yet … network effects are real. The Salesforce alumns are here in the Bay Area.

20% of their 2020 revenue, up from just 8% in 2018: Want more? We can this clearly with Shopify, which waiting all the way until 2020 to really monetize its partner base heavily. And the payoff was big. We did a great deep dive with Loren Padelford SVP of Shopify Plus / Shopify here: The post 5 Interesting Learnings From Shopify.

We organize all of the trending information in your field so you don't have to. Join 80,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content