This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

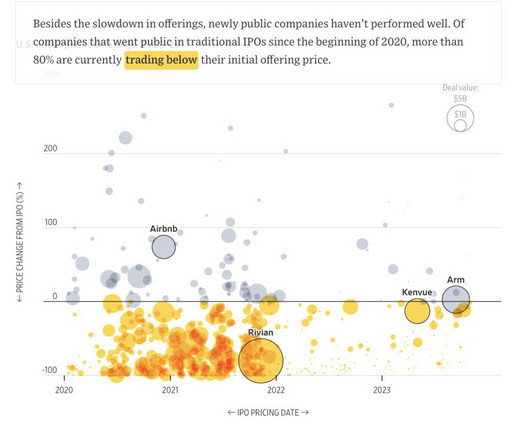

To me, the most jarring statistic was this one: 80% of IPOs since 2020 are trading below their IPO price, or “broken ”: So what, you might think? The post 80% of IPOs Since 2020 Are “Broken” appeared first on SaaStr. So the Wall Street Journal did a great job slicing and dicing IPO data recently. Buyer beware?

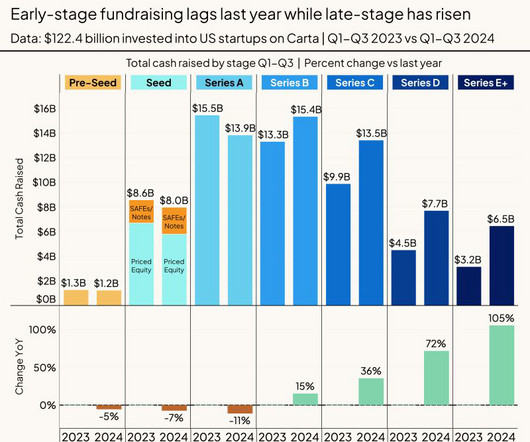

Early-stage fundraising overall hasn’t bounced back to its earlier 2020-2021 highs. Net net, if you’re hot, it’s as easy to fundraise as ever. But don’t let those headlines confuse you. Nor is there any real reason it should. The post Carta: Pre-Seed to Series A Funding is Down -9% in 2024 appeared first on SaaStr.

Yesterday, we shared the Top 10 Learnings from the 2020 Redpoint GTM Survey at SaaS Office Hours. The presentation is embedded below. It contains data on go to market team structure, performance by sales function, marketing spend benchmarks, and customer success priorities.

You can see here how events and trade shows are what helped put Datadog on the map: And yet, I see so many marketers putting less energy there than pre-2020 especially. And we all got out of practice here in 2020-2022. Not because events don’t work, but because they are a lot of work. But they are … work.

Speaker: Peter Cowen, Managing Director, Sutton Capital Partners & Ben Narasin, Venture Partner, NEA

May 13, 2020 @ 10 AM PDT - Tim Draper, Founder of Draper Associates. May 20, 2020 @ 10 AM PDT - Mark Mullen, Co-Founder of Bonfire Ventures. May 27, 2020 @ 10 AM PDT - Arlan Hamilton, Founder & Managing Partner, Backstage Capital. June 3, 2020 @ 10 AM PDT - Ben Narasin, Venture Partner at NEA.

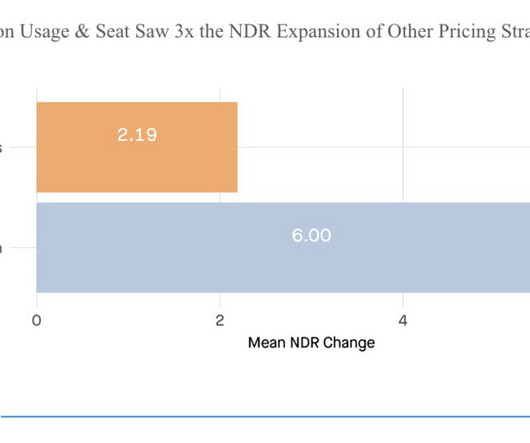

In 2020, we transitioned from a physical selling universe to a virtual selling universe. If you look at the net dollar retention change, the top quartile used to be 130% pre-2020. . #1: Founders Are More Positive The average founder’s outlook increased from 6.1 at the height of 2022 to 6.7. Now, it’s about 120%.

From 2020-2022, the top 20 deals were just 6%-8% of all VC capital. But just how much of venture capital overall is going to … the top names? Far more than ever, per Redpoint’s latest data. In 2024, 31% of all VC capital went into just 20 deals.

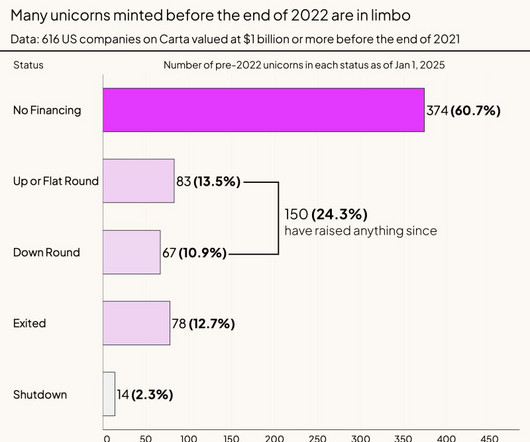

That a lot of unicorns that hit $1B+ valuations in 2020-2021 … probably aren’t really unicorns anymore. So there’s an uncomfortable truth that VCs don’t discuss outloud that often, but everyone has sort of accepted. Everyone resisted in 2022 and into 2023, but by 2024 they began to capitulate.

So Cloud and SaaS have had a bit of a rollercoaster the past 4 years, from the boom times of 2020-2021, to the tougher times overall of 2023, to the AI boom of 2024+. But one thing has done well through all of it: security. We always need it, and the threats keep coming. And Cloudflare has been one of the biggest beneficiaries.

May 13, 2020 @ 10 AM PDT - Tim Draper, Founder of Draper Associates. May 20, 2020 @ 10 AM PDT - Mark Mullen, Co-Founder of Bonfire Ventures. May 27, 2020 @ 10 AM PDT - Arlan Hamilton, Founder & Managing Partner, Backstage Capital. June 3, 2020 @ 10 AM PDT - Ben Narasin, Venture Partner at NEA.

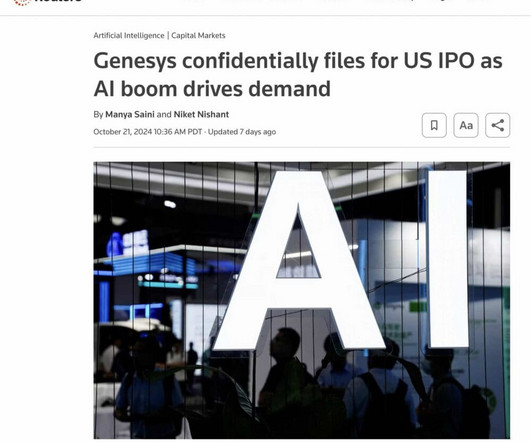

Others will have to accept much lower returns, at least for folks that invested in 2020-early 2022. It’s just time. OneStream was arguably one of these, and PE made a big gain on the IPO. Genesys may be the first of a flood of these PE-backed SaaS IPOs in 2025. It just filed to IPO.

And there is also a quiet wave of apathy in B2B outside of AI. If SaaStr disappeared, would it matter? Maybe that’s a different way of answering the question.

And there hasn’t been for a while: It was great times for SaaS liquidity in late 2020 through the end of 2021. And what you can see is there is really almost no liquidity for startups and scale-ups in SaaS and Cloud at the moment. Epic times.

Up From Almost None in 2020 to 295 Today. Artificial Intelligence Platform (AIP) is a Year Old But Fueling $159m in Q2 Bookings Alone To some Cloud and SaaS leaders, AI is a table-stakes addition. But for Palantir, it’s a true accelerant. #3. Commercial Customers Fueling Growth. Fast forward to today, they are closing 300 of them.

Speaker: Peter Cowen, Managing Director, Sutton Capital Partners & Mark Mullen, Co-Founder, Bonfire Ventures

May 13, 2020 @ 10 AM PDT - Tim Draper, Founder of Draper Associates. May 20, 2020 @ 10 AM PDT - Mark Mullen, Co-Founder of Bonfire Ventures. May 27, 2020 @ 10 AM PDT - TBD. June 3, 2020 @ 10 AM PDT - Ben Narasin, Venture Partner at NEA.

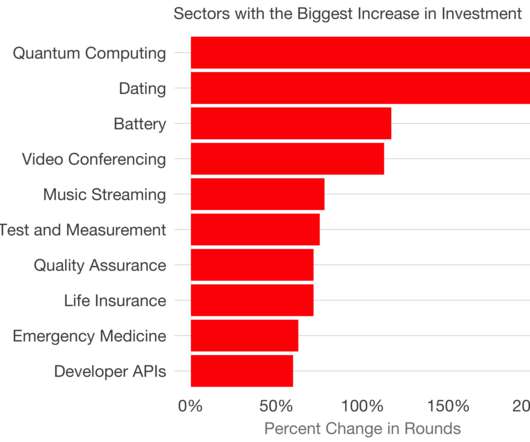

From time to time, I chart the fastest growing categories of startup investment in the US for seed through Series C. Here are 2015 , 2017 , This year, I was certain the categories would have been influenced by COVID19.

of GDP in 2020 to 4.0% Morgan Stanley said recently AI spend is about 50% new, 50% repurposed from the rest of the IT budget. That 50% new is enough to fuel the growth we see above. AI driving software from 2.0% in 2030 would be huge. It would be the New Golden Age of Software. That may be just what we’re seeing.

“The universe slammed SaaS down at the beginning of 2020, then splashed it way up, then slammed it down again. “It felt like we came out of the recession in Q3 of 2024,” Brian noted. Now it’s flashing back up.”

While CFOs have regained some control post-2020, one thing remains clear: if you don’t have buy-in from the technical developers and engineers actually using your product, you won’t get the deal done.

Speaker: Peter Cowen, Managing Director, Sutton Capital Partners & Tim Draper, Founder, Draper Associates

May 13, 2020 @ 10:30 AM PDT - Tim Draper, Founder of Draper Associates. May 20, 2020 @ 10 AM PDT - Mark Mullen, Co-Founder of Bonfire Ventures. May 27, 2020 @ 10 AM PDT - TBD. June 3, 2020 @ 10 AM PDT - Ben Narasin, Venture Partner at NEA.

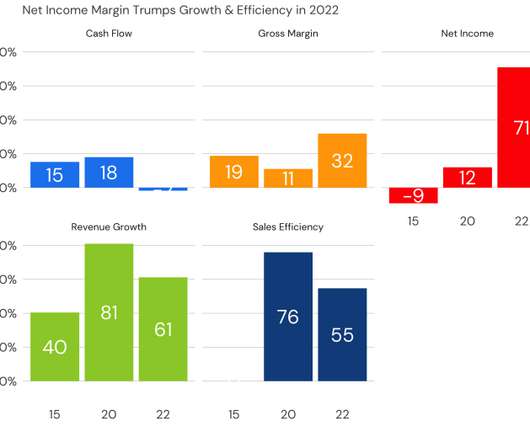

In 2020, revenue growth was the most important factor explaining a public software company’s forward multiple. The formula has changed since then. Net income has surged to the highest correlate of a public software company’s multiple surpassing revenue growth. Preference changes pop out of the data. Net income surges to 0.71

The late stage venture market is on pace to set a record in 2020. Through Q3 2020, late stage investors have invested as much as the entirety of 2019, and should things continue linearly we should expect the final tally to exceed $100B. Last, 2020 is on track to set a record for total IPO proceeds in a year. Check check.

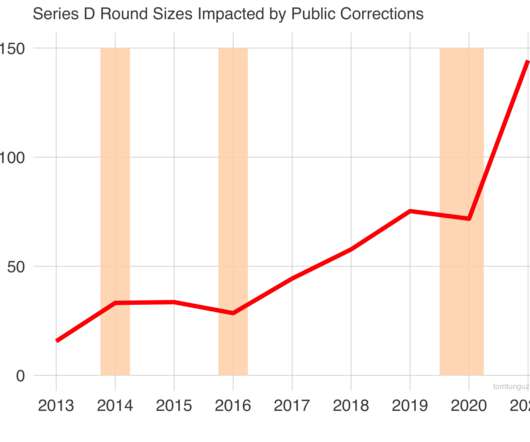

For the next 3 years, Series Ds increased in size until the late 2019/early 2020 correction of 41%. Ds doubled in 18 months starting in 2016, and again doubled from $75m to $150m in 2020-2021 - so the growth has been steeper on the way up and that may suggest a more sudden correction on the other side of the peak.

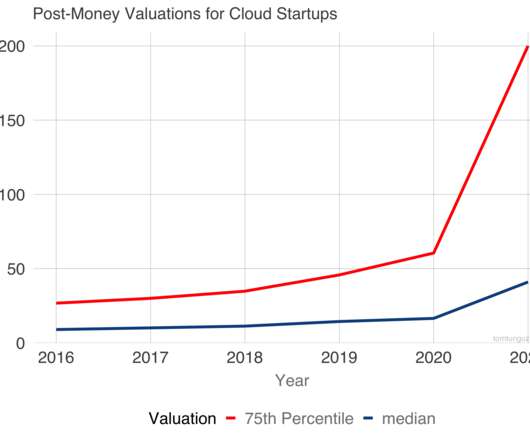

Till 2020, the growth rates of the private market valuations and the public valuation multiples paralleled each other at the highest level. This chart shows the median and the 75th percentile of enterprise value/forward revenue multiple for the basket of public stocks which were public at that moment in time. Correction Year.

Is your team focused on building a reliable tech stack for 2020? Forward thinking sales leaders are starting to prioritize technology initiatives. As organizations chase new revenue targets, B2B sales leaders must examine cutting edge prospecting solutions that proactively help reps identify, connect with, and close qualified buyers faster.

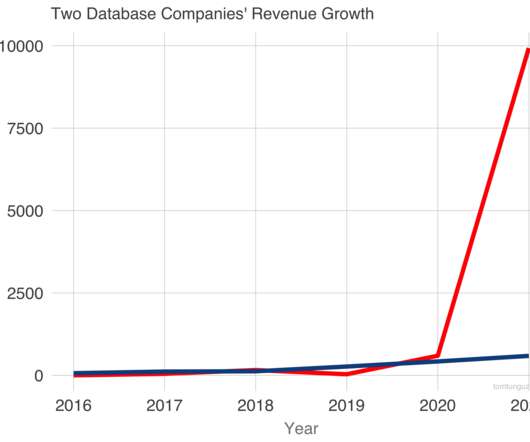

In fact, their revenue trajectories through 2020 are nearly identical. They would both exceed $400m in 2020. Both have grown very fast. Both companies employ a usage-based pricing model: pay for what you use. In 2016, each company recorded less than $50m in revenue. In two years, both would near $200m in revenue.

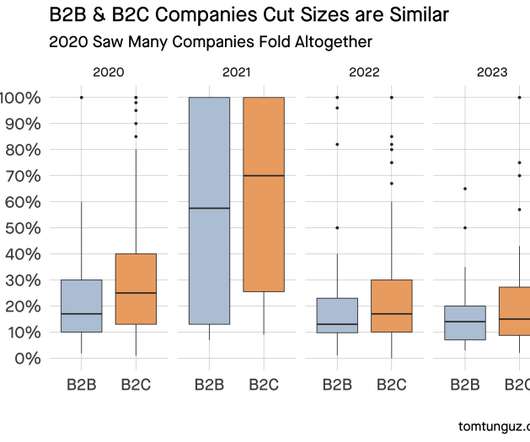

B2B companies have reduced headcount to a greater extent than at any time since 2020. In 2020, B2C companies cut 8.8x The current wave of layoffs, a difficult component of the innovation boom/bust cycle, differs from the previous years’ dynamics. the number of B2B employees. in 2021, & 6.9x

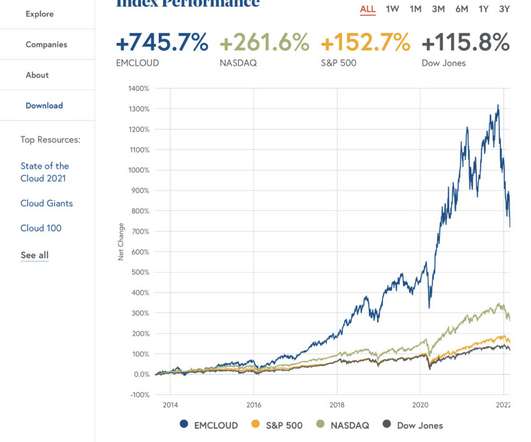

No, this SaaS Crash is so tough on VCs and public market investors because the market was just so, so high for Cloud stocks from mid-2020 to late 2021: You can see above in the BVP Nasdaq Cloud Index that while these are still Great Times in SaaS, they aren’t the crazy days that peaked around Thanksgiving 2021. I really do.

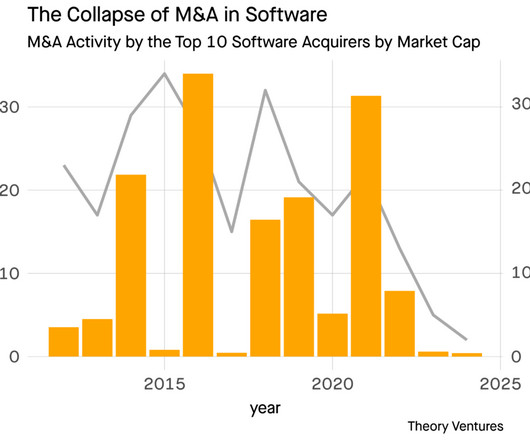

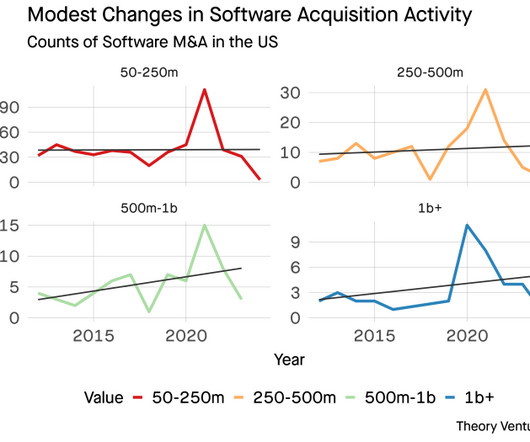

In 2014, 2016, 2020, 2021, these big mergers drove the figures into the tens of billions. X 2019 23.4% - 2020 61.1% Multi-billion dollar acquisitions, the blue bars, are the largest contributors to this swing. It’s no surprise that in those years, the biggest acquisitions accounted for more than 53% of dollars on average.

Speaker: M.K. Palmore, VP Field CSO (Americas), Palo Alto Networks

Thursday September 10th, 2020 at 11AM PDT, 2PM EST, 6PM GMT. In this webinar, you will learn: The future of data security. Preparing for crises that lead to security threats. How to update existing tech stacks to optimize data security. And much more!

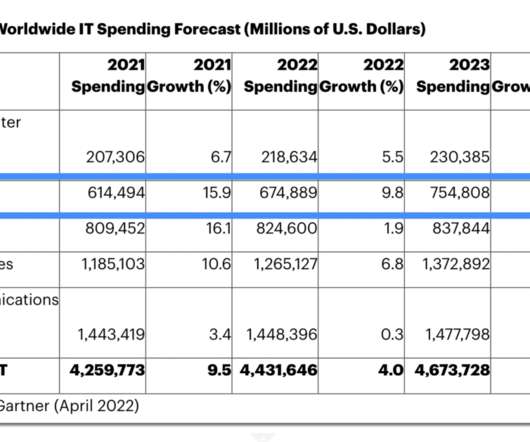

Enterprise software spending globally was $529B in 2020, per Gartner. Put differently, enterprise software spending globally was $529B in 2020. In 2023, it will be $750B. That’s a tailwind almost all of us are drafting on. — Jason BeKind Lemkin #???????????? jasonlk) April 13, 2022. in 2022 and 11.8% In 2023, it will be $750B.

Million Paying Users ARPU increased substantially from 2020 to 2023, and is up modestly again in 2024. #3. Even Box really is an enterprise player, and much of Microsoft’s and Google’s usage is presumably package in and not paid for discretely. #2. ARPU Continues to Slowly Increase Across 18.2 43% of Revenue Outside Of U.S.

So many of the things we learned from mid-2020 to early 2022 … just don’t apply anymore. It’s tough to say this “aloud”, but the truth is, a lot of folks just didn’t work all that hard from mid-2020 to late 2022. The unicorn age is over, at least for now, but many still don’t totally get it.

And interesting, this stacked chart shows 2020 funds and 2021 funds … when things got a bit loopy in venture … aren’t looking too good. And 2020 and 2021 funds look a little … rough right now. But it does show just how hard it is to do well in venture. The median 2017 fund is up after 7 years. But not by enough.

2020 was a year unlike any we've seen in our lifetimes. Will these unprecedented times expedite the rise of branded communities? What can organizations do to ensure their business remains relevant? This year's Community Predictions has all the answers!

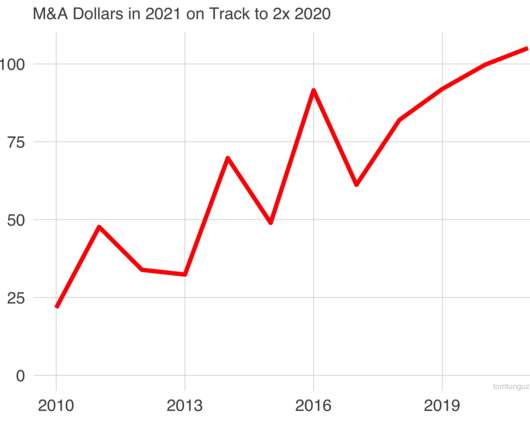

They’ve raised 3x as much year-to-date in IPOs as all of 2020, which was a healthy market. The M&A market is not far behind; it’s on track to double 2020’s decade high of M&A value transacted. Startups are basking in the IPO market. Where will the tally end the year? See that blip in 2012?

As a result, it’s quite profitable, with $150m in free cash flow in 2020. #2. This ecommerce revenue was $143m in 2020, about 22% of total revenue. Website revenues grew only 18% in 2020, while ecommerce revenue grew 78%. Over $500,000 revenue per employee. Squarespace has 1,200 employees and $700m in ARR.

This retrospective analysis compares Crunchbase data from April 1, 2020 to data from October 10, 2020 across three dimensions: round counts, investment total, and median round size. There’s a risk to those assessments: the data is incomplete since not all rounds founders close within a quarter are reported in that quarter.

This already had started to break pre-2020, as the war for talent drove up costs in these “secondary” sales centers. And then of course, post-2020, the world changed for sales reps. Second, sales comp expectations ballooned in the Boom Times of mid-2020 to early 2022, and haven’t really come down.

Tuesday December 15th, 2020 at 11AM PST, 2PM EST, 7PM GMT A roadmap to business excellence by understanding the importance of harnessing data, and automating processes. Keys to achieve the level of growth, cost optimization, and agility you want for your business.

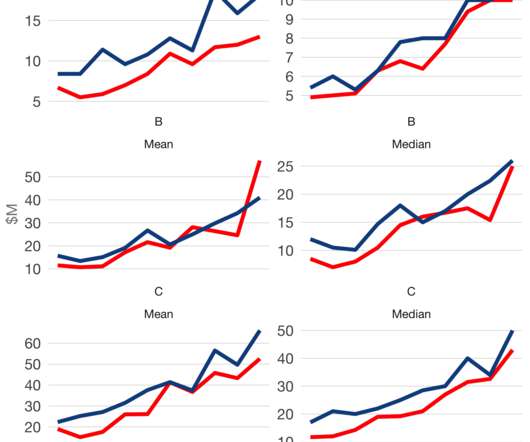

In 2020, they are 40% larger, a $33M swing in round size. In 2020, Series A investors have changed their behavior at the Series B. However, Series B data suggest insiders are leading aggressive rounds into compelling businesses. Witness the red line in this Series B Mean chart. Inside rounds have skyrocketed. What does this tell us?

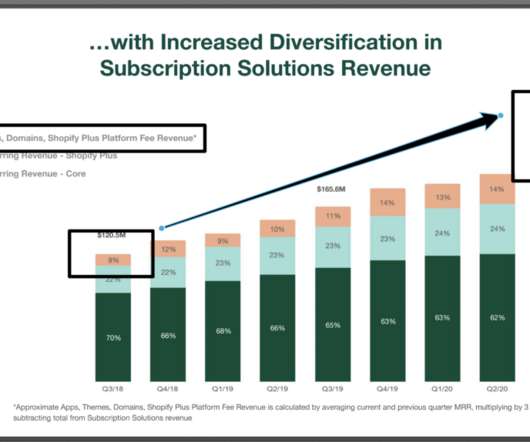

We can this clearly with Shopify, which waiting all the way until 2020 to really monetize its partner base heavily. 20% of their 2020 revenue, up from just 8% in 2018: Want more? What matters most is your ARR later, and dominating the market today. And the payoff was big.

The last IPO of the 2020-2021 era was HashiCorp in December 2021. And it’s one of the first to be acquired! IBM just closed on its $6.4 Billion acquisition of HashiCorp. And CEO David McJannet came to SaaStr Annual a little ways back to share his top scaling learnings.

So there’s a curious thing anyone close in venture capital fundraising and rounds today: Valuations for Hot VC Deals remain far higher than pre-March 2020 … even though growth for the overall public SaaS and Cloud companies has slowed to … all time lows. So you can discount some of this as outliers, even the outliers of the outliers.

Speaker: Jared Johnson, Director of Product Strategy, Kin + Carta

Thursday August 13, 2020 11AM PDT, 2PM EST, 6PM GMT. How to factor new societal changes and customer behaviors into new continuum design. What is an omni-channel experience and how does it set the standard for CX.

Input your email to sign up, or if you already have an account, log in here!

Enter your email address to reset your password. A temporary password will be e‑mailed to you.

We organize all of the trending information in your field so you don't have to. Join 80,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content