This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

At Datadog, their first focus was sponsored trade shows – specifically targeting the AWS ecosystem. Scaling Success: The Datadog Re:Invent Story Datadog’s experience with AWS Re:Invent demonstrates this approach perfectly. Schedule regular deep dives into performance metrics to maintain your edge.

Subscribe now Amazon ReInvent This week Amazon had their annual AWS ReInvent conference. ” AWS fully embracing the breadth over depth approach. Looking at the mid to long term, we feel very optimistic about the outlook for strong AWS growth. I created this subset to show companies where FCF is a relevant valuation metric.

For this reason, we chose to run exclusively on AWS and wherever possible, we make use of battle-tested AWS services, be it RDS Aurora for our relational databases, the Simple Queue Service (SQS) for our async workers or ElastiCache for our caching layer. SSM executes the commands using an on-instance daemon agent called AWS SSM Agent.

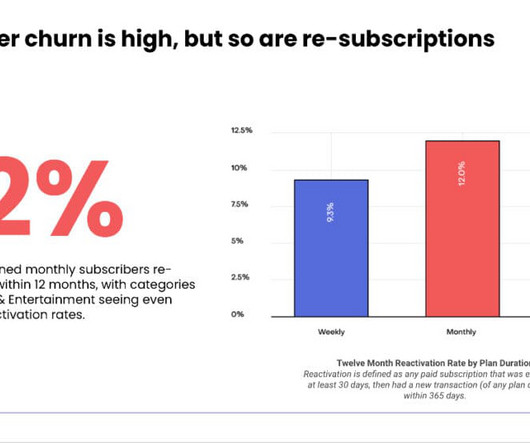

AWS, Twilio, Heroku, etc. The Hidden Costs of UBP While UBP offers many advantages, it does come with tradeoffs: Complicates churn measurement : If a customer uses your product intermittently (every third month, for example), standard monthly churn calculations will show the account churning and reactivating, skewing your metrics.

Through these interactions, I’ve built up mental benchmarks for metrics on which I place extra emphasis. My hope is that this analysis can provide startup entrepreneurs with a framework for how to manage their businesses around SaaS metrics (e.g., This metric is more self-explanatory, so I won’t go into detail.

Check out this 2018 Europa session with Guillaume Princen, Head of France and Southern Europe @ Stripe, where he talks about the metrics you need to be focused on in your startup. If you don’t have the time to watch the whole session, here are the main metrics you should be mindful of. MRR, obviously. We talked about churn.

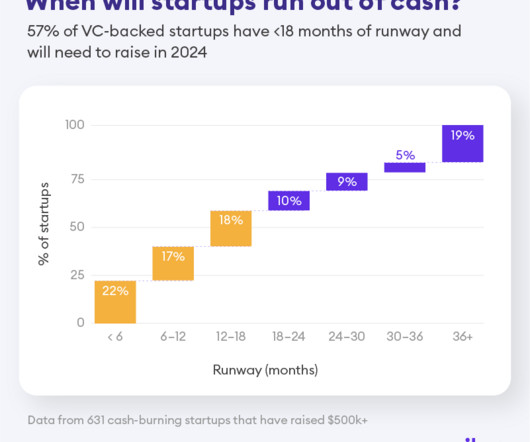

And realistically, most won’t have the metrics to pull off another round. Shopify , Datadog, Crowdstrike , Google Cloud-Azure-AWS, Snowflake , etc. Something that’s both not surprising but also pretty impactful: 57% of venture-backed startups will have to go “back to market” in 2024 to raise more capital.

Recently I was catching up with a good friend who used to be CEO of an enterprise-y SaaS social networking company — and the usage and engagement numbers of his business were just awful. So the buyer really doesn’t even have any success metrics going into the first renewal.

Culture Structure You want a culture of checking results and having metrics to evaluate those results from the LLM or a more traditional model. You want a culture that focuses on your metrics and evaluating what’s important to you. Whatever the metric is, you have to translate that into a concrete metric.

So there are a lot of rough and arm chair metrics for fundraising in SaaS in terms of valuations. Even If It’s Awful for Series A-E Rounds. For years, the standard was “about 10x” Top tier SaaS companies would tend to raise at around 10x ARR, with ones with slightly lower growth often raising at 5x.

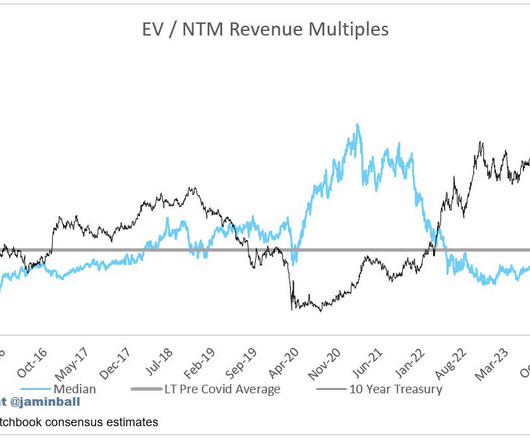

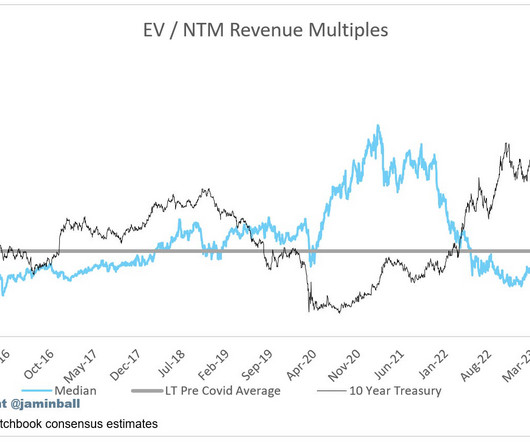

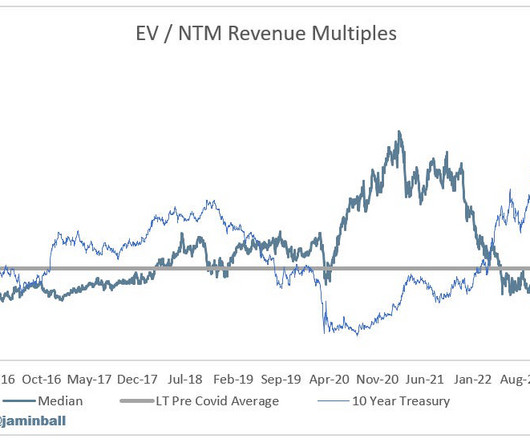

They each have some of the largest cloud businesses in the world in AWS, Azure and Google Cloud respectively. Given most software companies are not profitable, or not generating meaningful FCF, it’s the only metric to compare the entire industry against. Overall, there was weakness across the board.

We work exclusively with AWS as our cloud services provider and currently provide data hosting offerings in three different global regions – US, EU, and Australia – each architected across multiple availability zones for high availability. Our tooling allows for high availability.

So one thing that has exploded in SaaS in the past decade is the role of Private Equity buying both public SaaS companies (to take them private, “fix” some metrics, and IPO or sell them again), and generally later-stage private SaaS companies. You might be worth less ? is interesting to see.

Check out this week’s top blog posts, podcasts, and videos: Top Blog Posts This Week: Datadog, ZoomInfo, Atlassian, AWS: Epic Growth — But Some Real Headwinds For The First Time. Live: SaaStr Workshop Wednesday with Battery Ventures on SaaS Metrics. 5 Interesting Learnings from Duolingo at $360,000,000 in ARR.

The hyperscalers (AWS, Azure, GCP) are always some of the first companies to report earnings during earnings season (coming up in 2 weeks), and there’s always a read through for consumption names (meaning people believe there’s a correlation). I created this subset to show companies where FCF is a relevant valuation metric.

Growing Almost 50% as Approaches $2B in ARR The exact growth rate is based on an The Information report from a few weeks ago, and it seems about right looking at their published metrics. That’s awfully impressive. Importantly, growth has accelerated this year.

This modern architecture for data analysis, operational metrics, and machine learning enables companies to process data in new ways. The conference features talks from practitioners and open-source leaders from the ecosystem from Netflix, Microsoft, Expedia, AWS, and Preset.

However, with the introduction of Events-Based Billing by Chargify, this event-based billing model is now available to small and medium-sized businesses, giving them the ability to offer the same pricing models and bill customers just as precisely as Amazon Web Services (AWS) or the popular voice and messaging platform Twilio.

This is a critical metric. Gross margins have grown to best-of-breed at 83%, after a migration to AWS and more automation in customer support. Aim for that at least in your SMB segment if you can, and if you can provide at least as much value as Xero. Customer Lifetime Value is 81 months, from SMB That’s impressive.

We now have results from the three hypersclaers (AWS / Azure / GCP). The most notable change in tone was Andy Jassy talking about AWS. Given most software companies are not profitable, or not generating meaningful FCF, it’s the only metric to compare the entire industry against.

For example, Google and AWS are already ZoomInfo customers, but only certain sub-segments within those businesses – not the entire org. The Takeaway — While 2024 should be a bit more predictable, the most important metrics ZoomInfo is focusing on now are utilization and engagement.

Commoditization From AWS & Google Cloud. In addition, the SaaS metrics dramatically improved, including increased growth rate, faster pipeline velocity, shorter sales cycle length, and higher gross margin. No matter what VP of Sales they hired, sales consistently failed to meet their quota. Competition in the market rose sharply.

In B2B, the classic metric for this is 2% now and was 2% in 2006. In B2B, you also have fixed costs, but you can diversify monetization based on tokens or seats, or in the case of AWS, however you like. That’s up from 60% in 2023. While free trial offerings have increased, conversion to paid remains fairly low at 1.7%.

And it’s one of the three large cloud vendors that we all know: Microsoft, AWS, and Google. AWS’s marketplace has seen 1.5 But also it’s allowed us to get much closer to our provider, I mean, we host and run 100% on AWS, but pull data from everywhere. It was pretty easy to drive that from our side.

There’s a metric the very top founders track quitely, but ruthlessly, that I find other founders either don’t track, or sort of hide from. DigitalOcean is growing more slowly than its mega competitors Azure, AWS, etc. That’s % of marketshare. And importantly, if it’s growing, or shrinking. Why does it matter?

Now, let’s take this idea and apply it to the world of marketing metrics. Knowing that people are incentivized by what they’re rewarded for, marketing metrics boil down to alignment. If revenue is the North Star metric, everything you do should drive towards that. They are a vanity metric. Our unanimous pick?

Mai-Lan Tomsen Bukovec, Global Vice President for AWS Storage will deliver one of the keynotes. Data modelling companies create single definitions of metrics for consistency across organizations. This time, the conference will build on the foundation from last year’s event. Data engines query the data rapidly, inexpensively.

So I always have to pass here, no matter how good the metrics look today. “Quarterly MRR”, 100% Gross Margins, and Other Crazy Metrics. But if your metrics make truly zero sense, to me, that’s a flag. Gaming the metrics doesn’t help here. This is sort of awful. Not perfectly.

Amazon on AWS : “…customers are continuing to shift their focus towards driving innovation and bringing new workloads to the cloud. Azure (excluding Azure AI) continued to decelerate, and while AWS did come in ahead of expectations, it wasn’t a blow out. Follow along to stay up to date!

Through these interactions, I’ve built up mental benchmarks for metrics on which I place extra emphasis. My hope is that this analysis can provide startup entrepreneurs with a framework for how to manage their businesses around SaaS metrics (e.g., This metric is more self-explanatory, so I won’t go into detail.

Ed Lenta, the SVP and GM of Databricks, had the rare opportunity of scaling three hypergrowth companies — VMware, AWS, and Databricks. Sell To Customers How They Want To Be Sold To When Lenta first started building AWS in Australia, they were crude in how they thought about customers. Of course, we all know how that turned out.

With a background that includes leadership roles at AWS, Microsoft, and Lenovo, Fred brings a wealth of experience in building high-performing teams and driving revenue growth. And I know you’ve had some great experience, particularly while you were at AWS, running different partner sales, channel sales. They cannot resell.

Subscribe now Cloud Giants Report Q3 ‘23 Not a great signal for software this week from the Cloud Giants (AWS, Azure and Google Cloud)…After Q2 (3 months ago), the tone from the Cloud Giants around optimizations was largely: optimizations have started to ease, and net new workloads have picked up. That is not new.”

The Semantic Model Becomes a Must-Have: Semantic models unify a single definition across an organization for a particular metric. BI systems marry the centralized control of data teams with the ability to define and promote metrics at the edge of an organization (Omni). Looker did this within the context of a BI system.

Subscribe now Foundation Models Are to AI what S3 was to the Public Cloud Many people look at 2006 as the birth of the public cloud - the year Amazon launched AWS. Given most software companies are not profitable, or not generating meaningful FCF, it’s the only metric to compare the entire industry against.

Panintelligence recognized as Rising Star Partner of the Year (ISV) – EMEA finalist, one of many AWS Partners around the globe that help customers drive innovation. Geo and Global AWS Partner Awards recognize a wide range of AWS Partners, whose business models have embraced specialization, innovation, and cooperation over the past year.

Hyperscaler Preview Next week Amazon, Microsoft and Google report earnings and we’ll see Q3 data for AWS, Azure and Google Cloud. Given most software companies are not profitable, or not generating meaningful FCF, it’s the only metric to compare the entire industry against. Even a DCF is riddled with long term assumptions.

AWS (Amazon), Azure (Microsoft), and Google Cloud (Google) all reported this week. Then AWS appeared to add fuel to that hope before giving us a huge rug pull. After all, they had a lot of AI tailwinds, and benefited tremendously from consolidation (without a headwind of a larger base of smaller startups, like AWS).

Even if you come up short, and/or even if it takes much longer, you’ll then have a real solid chance of creating something of value. And if you don’t know how to get there … if you can’t honestly build a real, data-driven model that proves it at least to you … then that’s awfully telling.

Cloud Downgrades This week UBS came out with a couple research reports citing concerns in AWS / Azure growth. This brings me back to AWS / Azure downgrades. This was the worst tone that we’ve heard in years from large AWS/Azure partners, a group that usually expresses different shades of optimism about AWS/Azure growth.”

Hyperscalers Report Quarterly Earnings This week we saw AWS (Amazon), GCP (Google) and Azure (Microsoft) report earnings. Overall, it wasn’t pretty… AWS grew 28% when expectations were 30-31%. Every week I’ll provide updates on the latest trends in cloud software companies. Follow along to stay up to date!

5–10+ year leases are awful. Perhaps if there hadn’t been crazy metrics like “Community Adjusted EBIDTA”. But the bet was that, in The Best of Times, the public markets would see WeWork a bit like a crazy Amazon for space, one that would consume billions more, but revolutionize one of the largest markets in the world — office space.

” These are two quotes about AWS on the Amazon earnings call. AWS grew 16% in Q1, but called out growth in April (first month of Q2) was 11%. Given most software companies are not profitable, or not generating meaningful FCF, it’s the only metric to compare the entire industry against.

Alibaba is their AWS (or becoming it): The Cloud is better. Zoom is Growing at A Rate, And With Metrics, As We’ve Rarely Seen Before. Clippy was AI before AI: China is a whole different world for SaaS. It is even cheaper. That doesn’t mean it is cheap, tough. Shopify and MailChimp Go To War. This is a Big Deal.

We organize all of the trending information in your field so you don't have to. Join 80,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content