This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Subscribe now Amazon ReInvent This week Amazon had their annual AWS ReInvent conference. ” AWS fully embracing the breadth over depth approach. Looking at the mid to long term, we feel very optimistic about the outlook for strong AWS growth. Follow along to stay up to date! This year, there was tons of experimentation.

Within the next 12 months, Adam Seligman, VP of Generative Builders at AWS, believes there will be an inversion of SaaS. Yet, Anthropc sends out a detailed list of everything like the core features of appointment scheduling, treatment planning, supply tracking, and billing and invoicing. What does that mean?

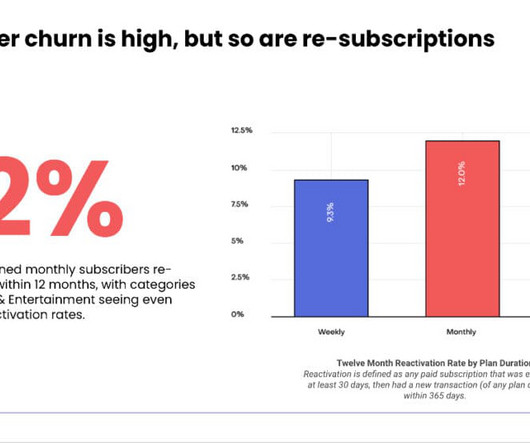

In this week’s Workshop Wednesday, RevenueCat CEO Jacob Eiting and Growth Advocate David Barnard share their annual State of Subscription Apps report with us. So, let’s look at the state of subscription apps and how B2B SaaS can learn from it. Churn is much higher on consumer subscriptions, but you have higher expansion revenue.

One invoice. I would pay each product provider in their own token: one for storage, compute, caching/CDN, email subscription management, etc. That’s much more work than the automatic credit card payment with AWS. When I hosted this blog on Amazon Web Services, I used 5 products.

Head of AI Dialpad: How to Build AI at Scale GTM/ B2B Speakers: CEO HubSpot Yamini Rangan: Going More Multiproduct, Going More AI, and Going More SMB and More Enterprise CEO Dropbox Drew Houston: DropBoxs Third Act: AI & Content Intelligence CEO Calendly, Tope Awotona Open AMA and AI in 2026 CEO Clio, Jack Newton: Reaccelerating Vertical SaaS to (..)

3. “Atlassian and AWS Say: Maybe Worry a Little Bit. Atlassian and AWS, two of the greats, may hold a clue: Atlassian and AWS Say: “Maybe Worry a Little Bit” 4. “A Framework For Your First SaaS Sales Comp Plan” A SaaStr Classic, still going strong in 2020. . “What Are Typical Price Increases in SaaS?”

You pay a subscription for websites to help you sell stuff. But as Shopify scaled, its revenue as a percent of commerce on its sites — “Merchant Solutions” — began to eclipse its recurring SaaS revenues. Fast forward to day, Merchant Solutions is a much larger share of revenue than software subscriptions.

It’s worth pointing out that Azure is a bit above the long term trendline, while AWS is still below (but accelerating up). To calculate implied ARR I take the subscription revenue in a quarter and multiply it by 4. These charts clearly show the ZIRP pull forward, the ensuing cloud cost optimizations, and then the recovery.

8 Out of 10 of Top Deals Were Sourced or Influenced by Partners And more than 40% of their total business is invoiced via channel partners. AWS alone generated $175m of contract value for Okta, growing 130%. So it makes sense, where practical, to split the teams here. And a few other interesting learnings: #6.

Backed by an army of developers, data engineers, and finance professionals, this events-based billing model allowed these large companies to directly link the value that their services provided with the cost presented on a customer’s invoice. How AWS Does It. What Amazon Web Services and Twilio Get Right.

Fast forward to the launch of AWS and the public cloud. Most public companies don’t report net new ARR, so I’m taking an implied ARR metric (quarterly subscription revenue x 4). Companies that do not disclose subscription rev have been left out of the analysis and are listed as NA. So why try and compete now?

They each have some of the largest cloud businesses in the world in AWS, Azure and Google Cloud respectively. Most public companies don’t report net new ARR, so I’m taking an implied ARR metric (quarterly subscription revenue x 4). Overall, there was weakness across the board.

ChartMogul is an analytics platform to help you run your subscription business. Our mission is to build powerful and secure cloud software for subscription businesses of all sizes, with a strong emphasis on good design and ease of use.

ChartMogul is an analytics platform to help you run your subscription business. Our mission is to build powerful and secure cloud software for subscription businesses of all sizes, with a strong emphasis on good design and ease of use.

RevenueCat (where I was lucky enough to be the first investor) is the leading mobile subscription management API and literally processes more API calls a day than Stripe. We’re kicking off a new series on SaaStr on what top SaaS and Cloud leaders (CROs, CMOs, and CTOs) use in their tech stack. It’s the nature of mobile.

The hyperscalers (AWS, Azure, GCP) are always some of the first companies to report earnings during earnings season (coming up in 2 weeks), and there’s always a read through for consumption names (meaning people believe there’s a correlation). Cloudflare is up 17%. Datadog is up 14%. Mongo is up 16%. Snowflake is up 14%.

We now have results from the three hypersclaers (AWS / Azure / GCP). The most notable change in tone was Andy Jassy talking about AWS. Most public companies don’t report net new ARR, so I’m taking an implied ARR metric (quarterly subscription revenue x 4).

And it’s one of the three large cloud vendors that we all know: Microsoft, AWS, and Google. AWS’s marketplace has seen 1.5 million subscriptions transacted and Google’s marketplace has seen 3X growth in SaaS sales. Like I said, we run 100% of our platform on AWS, so the fit was great.

We generate over 90% of our revenue from self-serve channels — users who purchase a subscription through our app or website. As a result, each cohort of new users typically generates higher subscription amounts over time. 8 – Weaning off AWS Look at this. For what it’s worth, this also gives you a hint on the margins of AWS. #9

Amazon on AWS : “…customers are continuing to shift their focus towards driving innovation and bringing new workloads to the cloud. Azure (excluding Azure AI) continued to decelerate, and while AWS did come in ahead of expectations, it wasn’t a blow out. Follow along to stay up to date!

If you are looking for the right billing and invoicing solution for your business, Zuora and Chargebee should be at the top of your list. Do they support the payment platform you desire? Do any of them have what you want in a subscription management service? Zuora These two platforms are quite useful for billing and invoicing.

Subscribe now Cloud Giants Report Q3 ‘23 Not a great signal for software this week from the Cloud Giants (AWS, Azure and Google Cloud)…After Q2 (3 months ago), the tone from the Cloud Giants around optimizations was largely: optimizations have started to ease, and net new workloads have picked up. That is not new.”

Thanks to the evolution of our cost program, we now spend only one hour a week on cost management, with great success” We’ve built our own in-house AWS cost monitoring, but there are plenty of solutions on the market to do this for you, as well as your cloud provider’s own tooling. Zero touch costs. This one speaks for itself.

It looks at the YoY dollar change in quarterly revenue from the hyperscalers (just looking at Azure / AWS because the data goes back further) going back a few years. If we break this down and look at Azure and AWS independently (graphs below), you’ll see how the AWS “swings” were a lot more volatile.

It is the largest in-person event in the country—2,000+ attendees, 800+ companies, and 100+ speakers—along with features such as Betakit Keynote Stage, AWS Pitchfest, Workspaces Tradeshow. Our platform includes branded localized checkout, subscription management, and so much more. Schedule a demo now or at SaaS North in person!

We’ve shared a number of parts of Buffer’s business transparently over the years — and one piece we’ve always wanted to expand on is where your money goes when you pay for a Buffer subscription. Our hosting costs include service providers like AWS, Cloudflare, MongoDb, Twitter, etc.

Subscribe now Foundation Models Are to AI what S3 was to the Public Cloud Many people look at 2006 as the birth of the public cloud - the year Amazon launched AWS. Most public companies don’t report net new ARR, so I’m taking an implied ARR metric (quarterly subscription revenue x 4). Follow along to stay up to date!

Hyperscaler Preview Next week Amazon, Microsoft and Google report earnings and we’ll see Q3 data for AWS, Azure and Google Cloud. Most public companies don’t report net new ARR, so I’m taking an implied ARR metric (quarterly subscription revenue x 4).

Tableau was at >$900m in recurring revenue … growing 41% (!). And subscriptions were growing 115%. There aren’t that many things of true scale, that are strategic, that Salesforce could buy at this stage. Tableau Reports First Quarter 2019 Financial Results. That’s not Twilio growth, but it’s awfully strong.

We chase after potential leads trying to qualify them, we spend a lot of time trying to book meetings and give demos, we spend an awful lot of time simply trying to make a value driven discussion happen at a later date. Second, sales teams spend a lot of time doing laborious, repetitive tasks that don’t always result in much value.

Hyperscalers Report Quarterly Earnings This week we saw AWS (Amazon), GCP (Google) and Azure (Microsoft) report earnings. Overall, it wasn’t pretty… AWS grew 28% when expectations were 30-31%. Companies that do not disclose subscription rev have been left out of the analysis and are listed as NA.

AWS (Amazon), Azure (Microsoft), and Google Cloud (Google) all reported this week. Then AWS appeared to add fuel to that hope before giving us a huge rug pull. After all, they had a lot of AI tailwinds, and benefited tremendously from consolidation (without a headwind of a larger base of smaller startups, like AWS).

Cloud Downgrades This week UBS came out with a couple research reports citing concerns in AWS / Azure growth. This brings me back to AWS / Azure downgrades. This was the worst tone that we’ve heard in years from large AWS/Azure partners, a group that usually expresses different shades of optimism about AWS/Azure growth.”

The GDC Expo showcases the latest game development tools and services from leading technology companies such as AWS, Epic, and Google. We handle every payment need from subscription management to tax collection, remittance and more so your business can go farther, faster. Schedule a demo now or at GDC 2024 in person!

” These are two quotes about AWS on the Amazon earnings call. AWS grew 16% in Q1, but called out growth in April (first month of Q2) was 11%. Most public companies don’t report net new ARR, so I’m taking an implied ARR metric (quarterly subscription revenue x 4).

Over the last decade, recurring revenue has emerged as the preferred model for businesses moving beyond transactional commerce. While the first generation of recurring revenue was defined by simple subscriptions—think Netflix’s original “one-size-fits-all” $7.99 From Static Subscriptions To The Relationship Economy.

Cloud Giants Report Q2 We also got the Q2 quarters from AWS / Azure / GCP this week! Most public companies don’t report net new ARR, so I’m taking an implied ARR metric (quarterly subscription revenue x 4). Companies that do not disclose subscription rev have been left out of the analysis and are listed as NA.

A few months ago, we retired our last pieces of infrastructure on DigitalOcean, marking our migration to AWS as complete. Our journey was not your regular AWS migration as it involved moving our infrastructure from classic VMs to containers orchestrated by Kubernetes. Ultimately, we decided to go with AWS. Team expertise.

” We saw some green shoots in AWS and a few other consumption names, and overall sentiment seemed more positive. Most public companies don’t report net new ARR, so I’m taking an implied ARR metric (quarterly subscription revenue x 4). I’ll post a much longer recap soon, but today I wanted to post the highlights.

Some of that is by launching add-on products that can be priced as subscription fees or transactional per conversation. They just happened to launch AWS and ended up capturing way more value just in themselves than the entire on-prem storage market before them. ARPU, ACV, and LTV are increasing. Drop in costs.

Next week we get all 3 hyperscalers reporting (AWS from Amazon, Azure from Microsoft, and GCP from Google). On AWS, in their Q4 earnings call they said AWS was growing “mid teens” in January (down from 20% in Q4). Companies that do not disclose subscription rev have been left out of the analysis and are listed as NA.

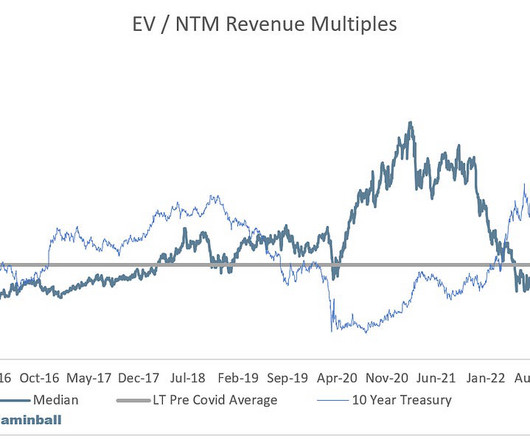

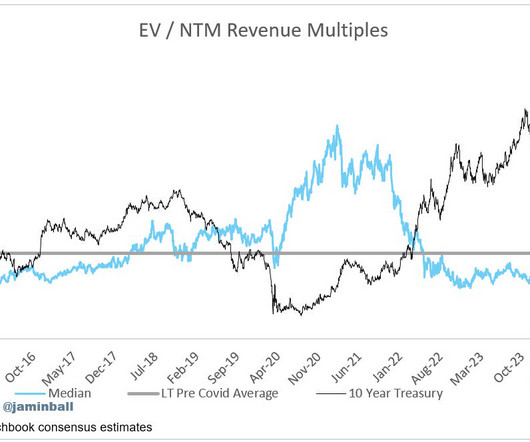

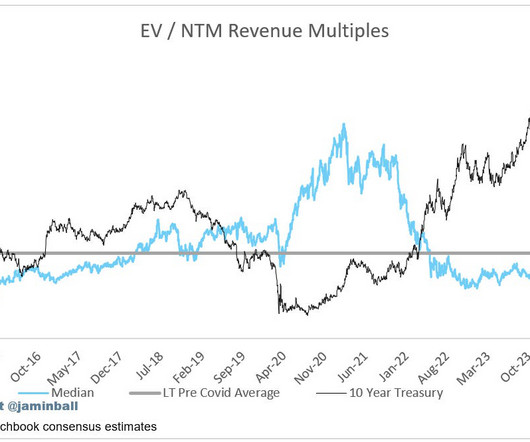

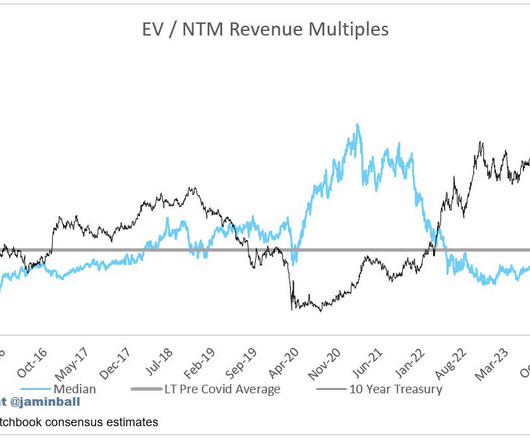

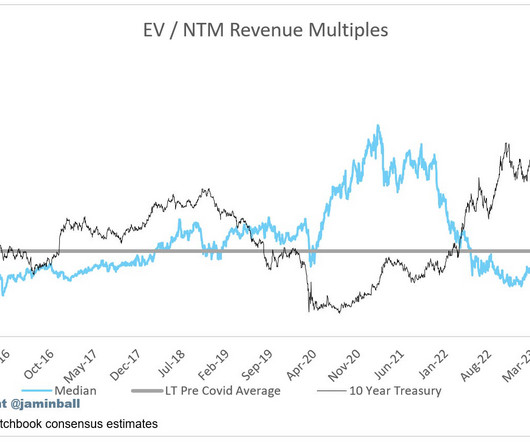

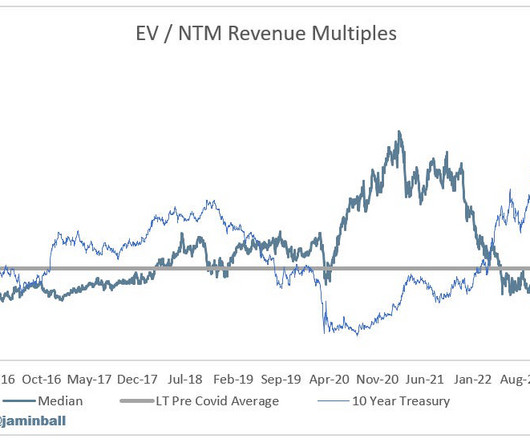

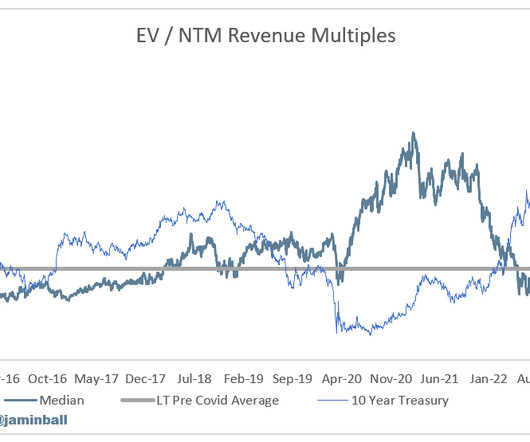

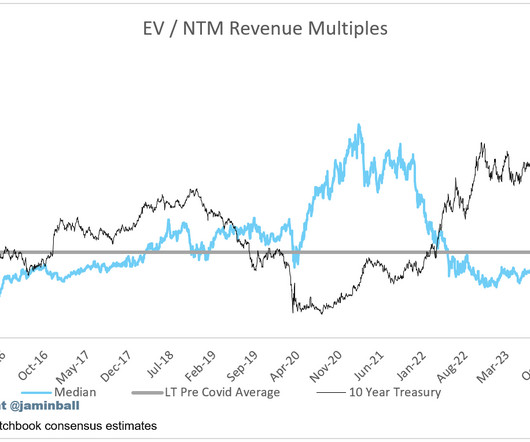

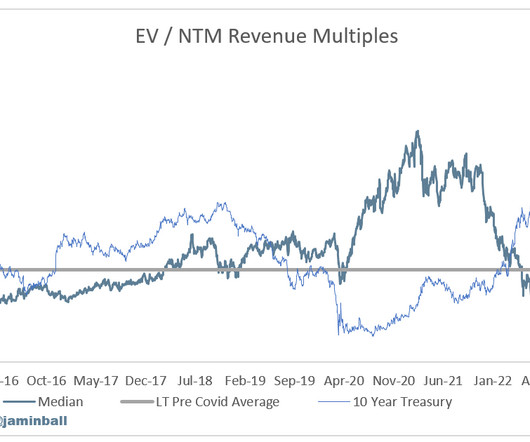

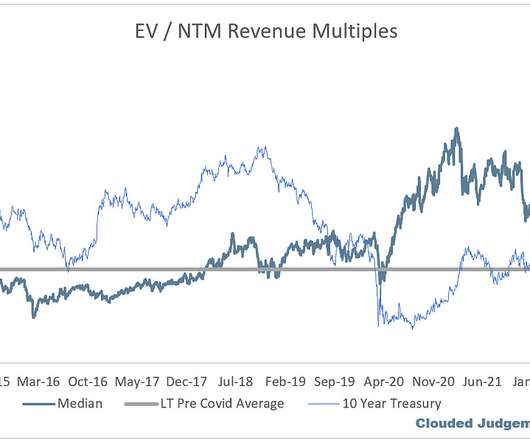

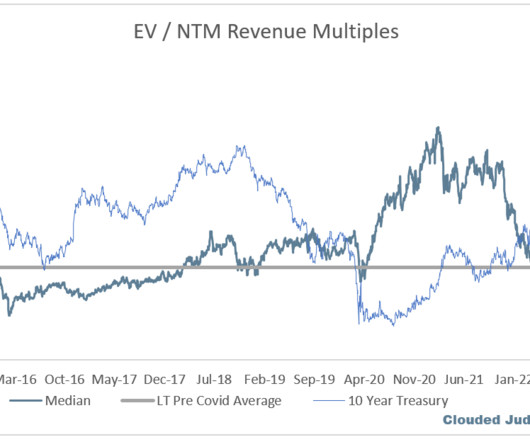

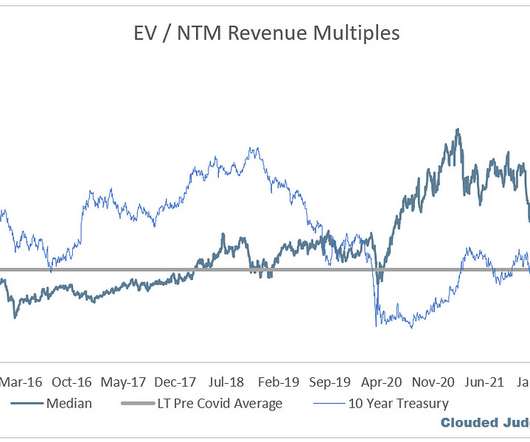

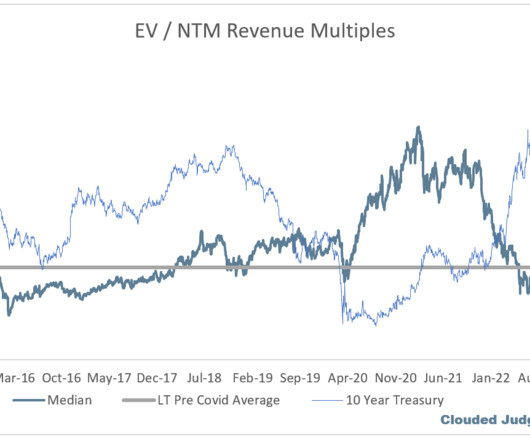

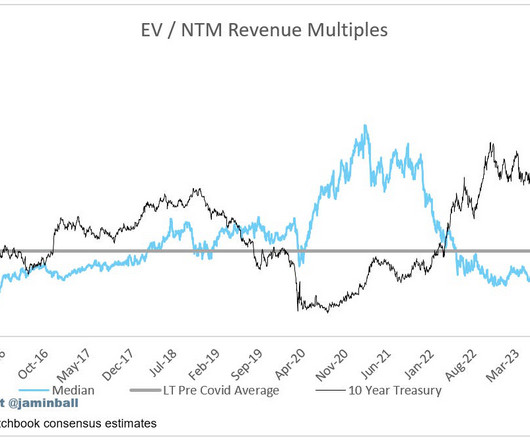

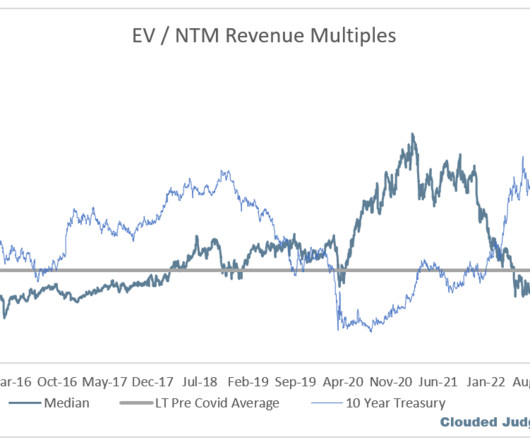

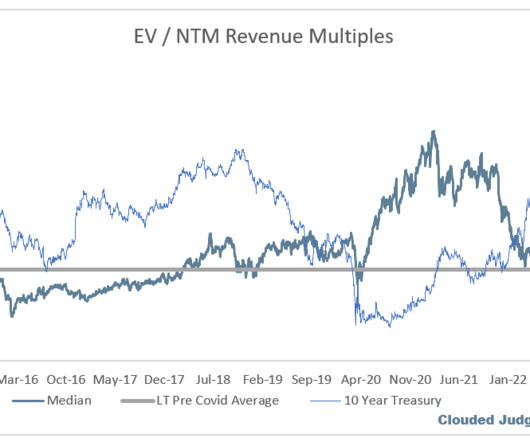

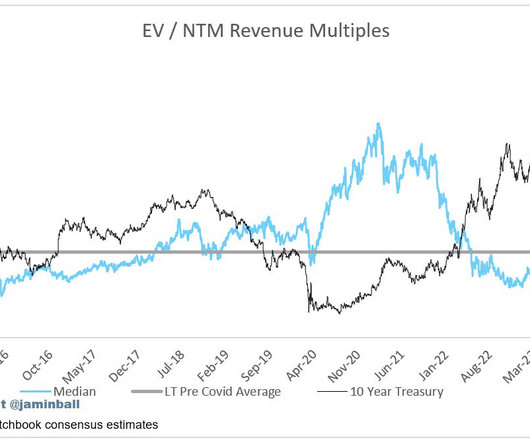

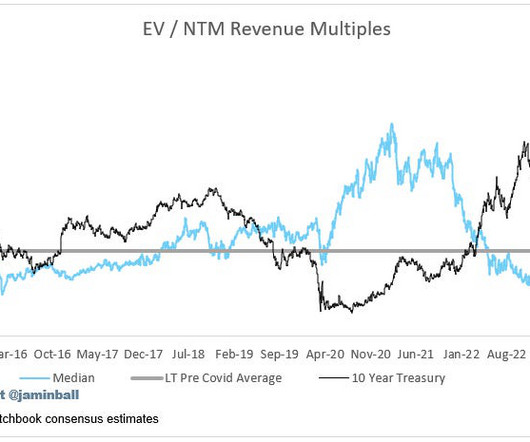

All 3 (AWS, Azure, GCP) saw positive reacceleration Quarterly Reports Summary Top 10 EV / NTM Revenue Multiples Top 10 Weekly Share Price Movement Update on Multiples SaaS businesses are generally valued on a multiple of their revenue - in most cases the projected revenue for the next 12 months.

I’m looking at it and I’m like, “Who’s got the Wall Street Journal subscription? For us, it’s been, “Migrate things that you have on invoice over to card.” We can save companies $100,000 on their AWS bill. Everybody wants to save $100,000 on their AWS bill right now.

” From AWS (paraphrased): They said they expect the reaccleration they saw in Q4 to continue into 2024 2024 Estimate Updates One important metric I’m tracking this quarter is the change in 2024 estimates pre / post earnings. Companies that do not disclose subscription rev have been left out of the analysis and are listed as NA.

We organize all of the trending information in your field so you don't have to. Join 80,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content