This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

With Databricks now one of the largest pre-IPO technology companies, with $10 billion of expected non-dilutive financing and a valuation of $62 billion, Ron’s insights are gold for any revenue leader looking to scale. Our founders focused on adoption first, not revenue, Ron explains. The takeaway? The takeaway?

Subscribe now Azure Report - Cloud Infra Looks Good! For software, all eyes were on Azure - which grew 31% YoY (ahead of expectations closer to 29%). Azure doesn’t disclose exact Azure quarterly revenue (they disclose growth rate in absolute terms and in constant currency), but there are good estimations.

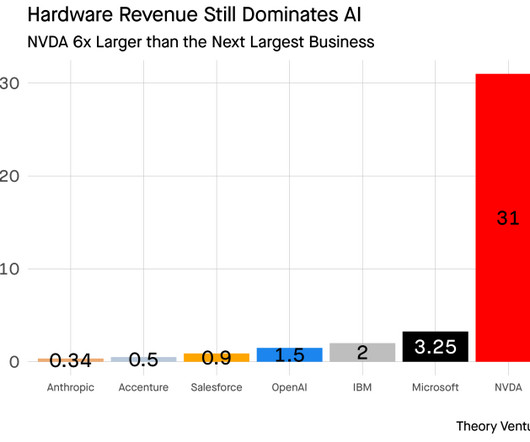

I analyzed Q4 revenue data from publicly traded companies across multiple sectorssoftware companies, consulting firms, and hardware manufacturers to determine which segment dominates the AI market. NVIDIA’s data center business dominated the field, generating $31b in Q4 revenue with impressive margins exceeding 70%.

Nvidia, Google Cloud, Azure, etc. Only 21% of Salesforce’s Revenue is from … Sales This has been true for many years, but it often comes as a surprise to those that don’t know the company as well as they know its CRM. #2. They still do some for their largest customers, and it’s down to about 5% of revenues.

“Because of our overall differentiation, more than 18,000 organizations now use Azure OpenAI service, including new-to-Azure customers.” ” “Higher-than-expected AI consumption contributed to revenue growth in Azure.”

But fast forward to today, and Microsoft truly is a Cloud and SaaS company, with Azure and LinkedIn its fastest growing business units! Azure and other cloud services grew a record 40% and the total Microsoft Cloud grew to a $90 Billion run-rate. MSFT Q4 2022 – Revenue up 12% to $51.9 LinkedIn revenue grew a stunning 37%.

Google Cloud Platform (GCP) & Microsoft Azure had strong quarters with about 28% annual revenue growth each. The total customer count for Azure’s OpenAI has grown dramatically. In Azure, we expect revenue growth to be 26% to 27% in constant currency, including roughly 1 point from AI services.

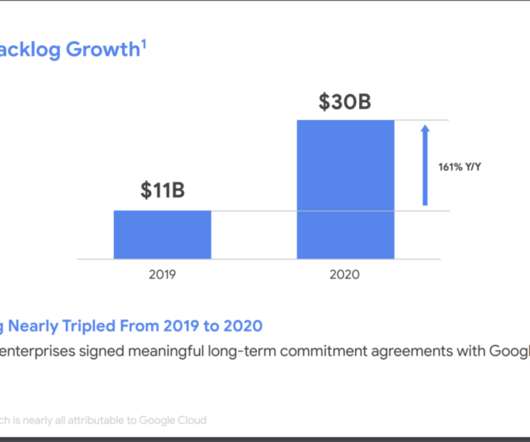

But are AWS, Azure and Google Cloud just too big for us to learn from? Google Cloud sees Cloud revenues tripling in the next 5 years. Google Cloud continues its march upmarket, competing with Azure. You can see that here vividly, with Google Cloud having a $30B backlog of signed revenue on top of its $13B in ARR.

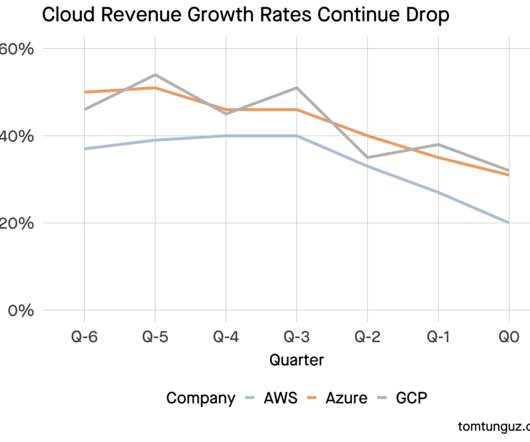

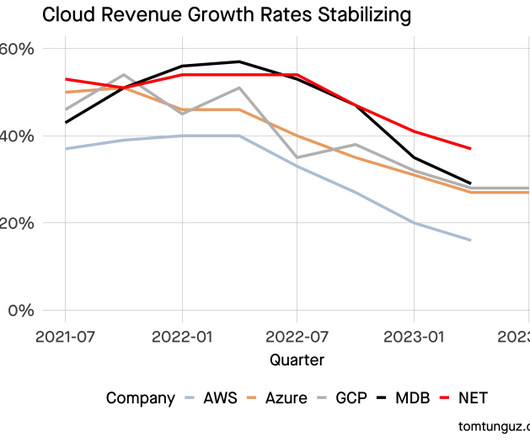

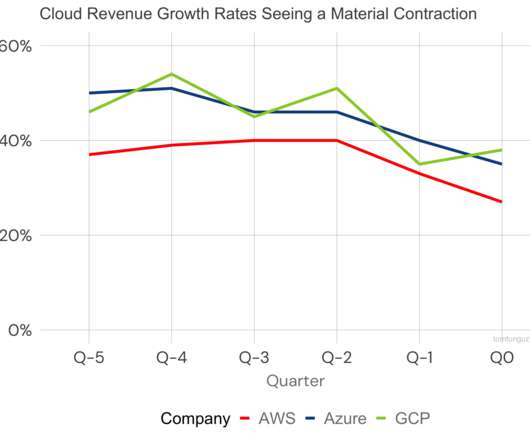

So follow AWS, Azure and Google Cloud. Let’s look a whole level up to the real canaries-in-the-coalmine: AWS, Azure and Google Cloud. And AWS grew 37% at a $74B run-rate , down a bit from 39% the prior quarter but still adding an insane amount of new revenue. If they stumble, we’re in for a rough patch. They are the Cloud.

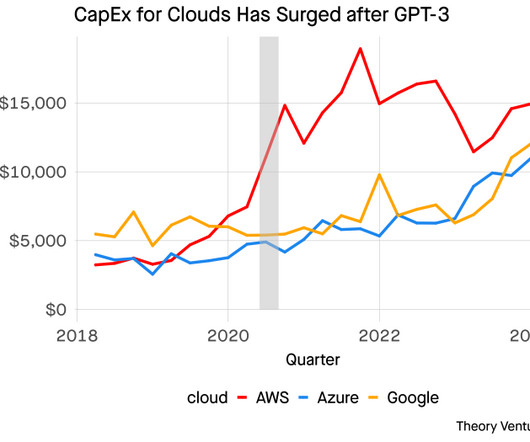

Cloud Capex in Q1 AWS $14 billion Azure $14 billion Google Cloud $12 billion These are not one-time investments, but part of a broader trend that started to occur after the introduction of GPT 3 in mid-2020 Amazon was the first to invest significantly. Each of these businesses are large enough to justify it. “Moving to AWS.

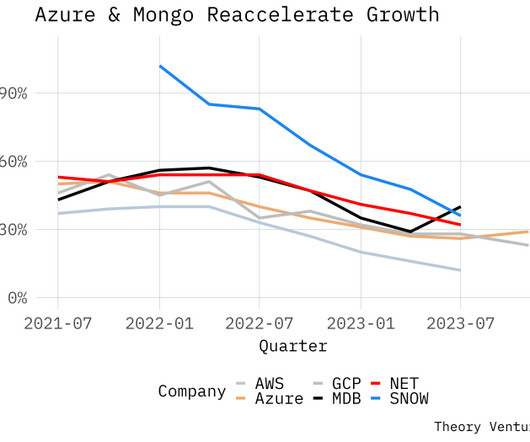

And broader Cloud players had great years too, from MongoDB to Cloudflare to Azure, if not quite as crazy as at the peak of 2021. But then in 2023 — it just plummeted.

The charts below show the change in quarterly revenue YoY (so Q1 ‘24 rev - Q1 ‘23 rev) going back to 2017. It’s worth pointing out that Azure is a bit above the long term trendline, while AWS is still below (but accelerating up). Beating consensus revenue estimates is the first aspect of a successful quarter.

We saw moderated consumption growth in Azure and lower-than-expected growth [elsewhere]. Segment Expected Growth Productivity 12% Office Commercial 6% Office On-Premise -25% LinkedIn 5% Dynamics 13% Intelligent Cloud 18% Azure 26% Server -3% Services -3% 2. At some point, the optimizations will end.

. “[We’re] not fighting those headwinds”: Given that customers sign 3+ year, $1m+ contracts, one wouldn’t expect any massive decline in revenue from any shorter-term macro effects anyway. 20,000 employees, so about $350,000 revenue per employee. But new bookings aren’t really down, either. to $4m ACV. #4.

Billion in ARR GitLab is growing 30% at $730m ARR Microsoft Azure, Google Cloud are on fire, fueled by AI But others are seeing more headwinds due to downturns in the “B2B2B” segment of tech. Revenue growth has slowed from epic rates on the way to $1B ARR, to a still stunning 29% at $1.5B Cloudflare is growing 30% at $1.6

If it wasn’t clear before, AI is the single biggest revenue driver in cloud. Microsoft’s Azure is winning share directly from Amazon. “The number of $100 million-plus Azure deals increased over 80% year-over-year, while the number of $10 million-plus deals more than doubled. of revenue in a year.

A year ago, AWS, GCP, & Azure averaged 44% annual growth. So far in the first month of the year, AWS year-over-year revenue growth is in the mid-teens. in revenue, GCP is at -7%, not far off breakeven, but a long way from AWS’ 30% profit margins. Today, that figure has dropped to 27%. Amazon: Net sales increased $21.4

Focusing on smaller developers, in some ways it’s been a bit overshadowed by AWS, Azure, and Google Cloud. DigitialOcean doesn’t want to take AWS, Azure and Google on in the enterprise and doesn’t really try. They are only 15% of the customers, but 83% of the revenue. Only 38% of revenue in North America.

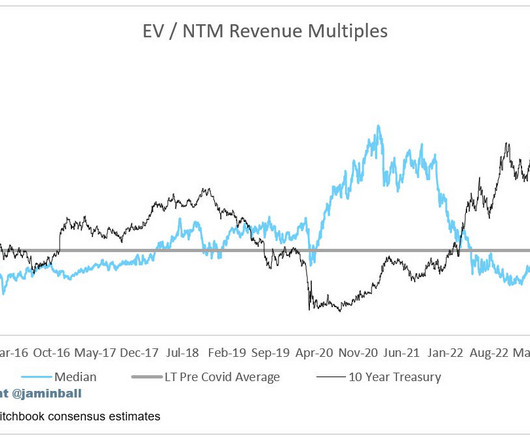

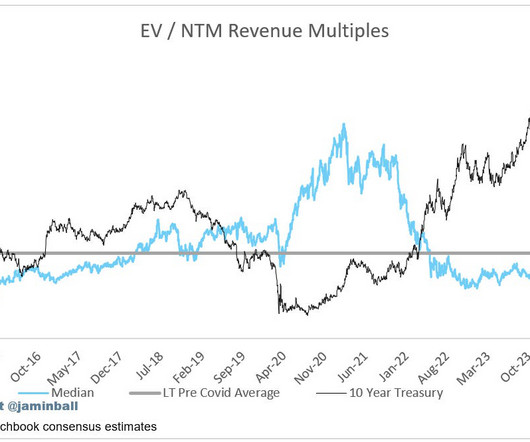

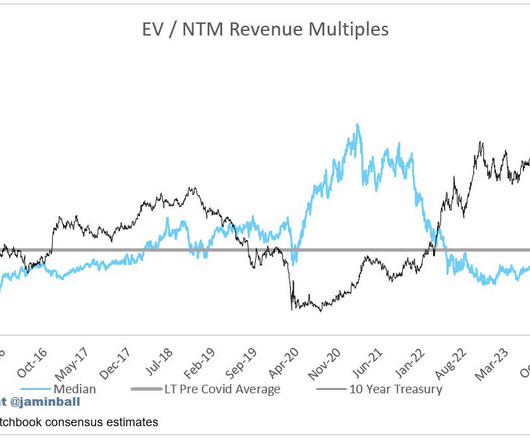

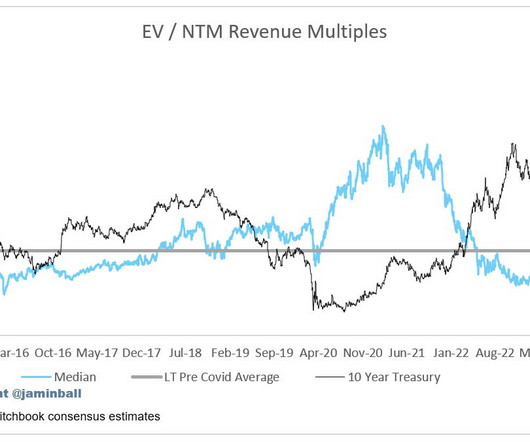

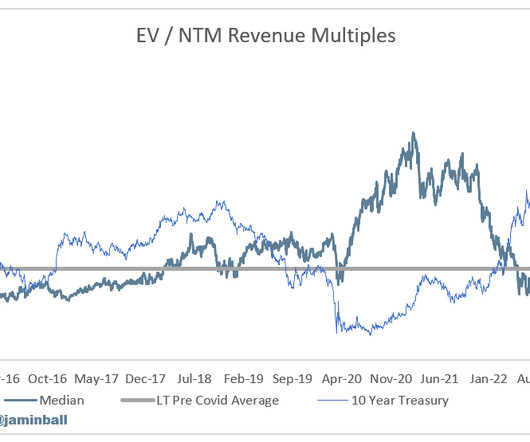

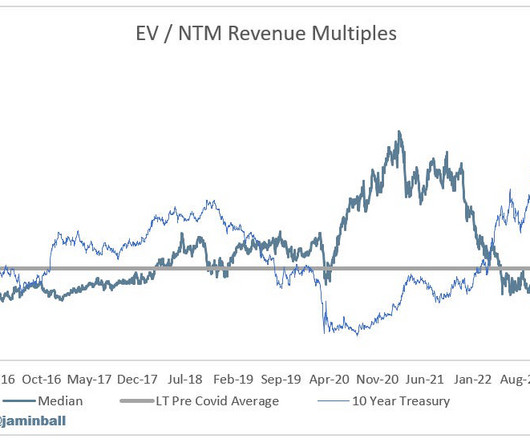

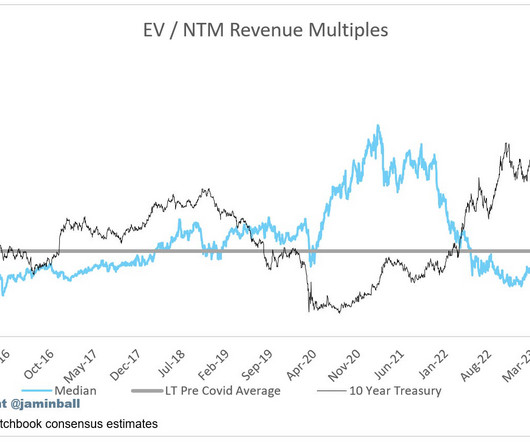

They each have some of the largest cloud businesses in the world in AWS, Azure and Google Cloud respectively. Revenue multiples are a shorthand valuation framework. Multiples shown below are calculated by taking the Enterprise Value (market cap + debt - cash) / NTM revenue. Overall, there was weakness across the board.

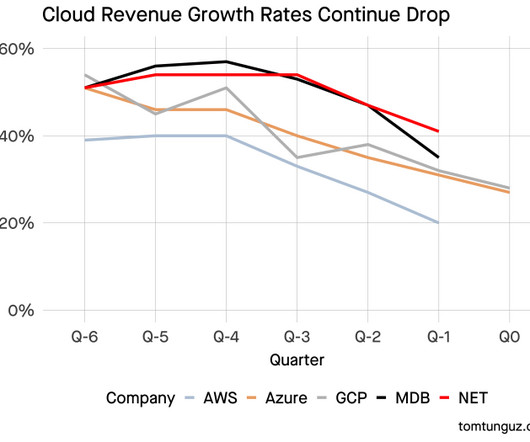

Microsoft Azure. Microsoft Azure grew 40% y/y, tying the fastest quarterly growth rate in the past 5 quarters. Google’s growth rate fell to 35%, a 29% decline from the trailing 4 quarter average of 49% annual revenue growth. Here are some hypotheses: Google may have greater customer concentration in GCP than Azure.

Both Google & Microsoft announced growth rates in GCP & Azure that held steady from one quarter to the next. Microsoft’s Azure Open AI customer base grew 4x by count, up from 2500 last quarter : We have great momentum across Azure OpenAI Service. The desire for AI is broad. The acceleration is really quite broad.

Only 12% service revenue, despite being so enterprise. Partners are key — Baker Hughes (a customer and partner) makes up a massive 30% of revenue, and claim Microsoft Azure has contributed $200m in total bookings. And a few bonus notes: #6. Re: Baker Hughes, oil and gas is its largest vertical. #7.

Amazon Web Services and Azure, the business units inside Amazon and Microsoft serve and sell to small, medium, and large companies in every major geography. Microsoft Azure. Here are the revenue growth rates for these businesses broken out by software and infrastructure. Fortunately, it exists. So do Salesforce. ServiceNow.

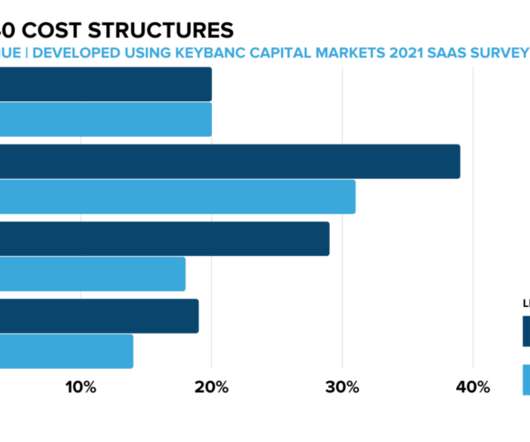

Typically support consumes about perhaps 5%-7% of your revenue at scale (excluding customer success) in most SaaS models. Another 5%-7% go to core infrastructure costs (AWS, Azure, Snowflake, etc). Dear SaaStr: What is The Average Ratio of Support Staff to Customer Count in SaaS?

Look no further than the massive companies pushing the public & the private market forward: Snowflake, Databricks, Amazon, Azure, Google Cloud. Cloud databases generated $39b in spend , about half of all database revenue. On October 25th, I’ll share my 10 predictions for data in 2023 at The Impact Data Summit.

Microsoft Azure. Infrastructure revenue growth averaged 33% this quarter, which is astounding considering we’re talking about businesses that sum to more than $50b of revenue per quarter. At a 7x multiple of revenue, that is another $84b of market cap creation, in theory. Google Cloud Platform. Amazon Web Services.

Ultimately — revenue multiples. Revenue multiples are how much VCs, investors, and ultimately, an IPO and public markets will value each dollar of revenue. Revenue multiples don’t affect customers, or even revenue itself. That revenue multiples should rise from where they were in 2019.

As a result, software vendors often see an uptick in revenue and bookings during these periods. Top 10 EV / NTM Revenue Multiples Top 10 Weekly Share Price Movement Update on Multiples SaaS businesses are generally valued on a multiple of their revenue - in most cases the projected revenue for the next 12 months.

Just about everything in Cloud, SaaS and AI is firing on all cylinders at Microsoft: Azure and Cloud up +30% (!) 60,000 AI-on-Azure Customers, and Accelerating — Up a Stunning 60% Year-over-Year We all sort of knew this, but helpful to see the numbers here. #3. So it’s a great and important one for us all to learn from.

Many have used Digital Ocean at the cheaper, simpler version of AWS-Azure-Digital Ocean to get going fast and quickly. But it’s raining cash, and earnings per share is growing 22% — faster than revenue. And if so, maybe that’s Digital Ocean. If you haven’t heard of Digital Ocean, ask your developer.

Have you ever wondered how you could turn PLG concepts like the freemium model into a fast-growing revenue driver for your company? With a PLG-heavy background, first working at Microsoft Azure and again with Atlassian, the PLG pioneers, he gives insights into leveraging PLG for the growth of your organization.

Calendar Quarter Azure OpenAI Orgs, k CoPilot Users, m Power Platform Orgs, k 1/1/24 53 1.3 “In Azure, we expect Q3 revenue growth in constant currency to remain stable to our stronger-than-expected Q2 results.” Many companies are moving in this direction. 230 10/1/23 18 1 126 7/1/23 11 63 4/1/23 2.5

Using the Drift Conversation Cloud, businesses can personalize experiences that lead to more quality pipeline, revenue and lifelong customers. More than 5,000 customers use Drift to deliver a more enjoyable and more human buying experience that builds trust and accelerates revenue. Usually, it takes a paradigm shift to grow.

Which means better customer relationships, more data, and new sources of revenue. Secureframe allows companies to get compliant within weeks, rather than months and monitors 100+ services, including AWS, GCP, and Azure. StratusGreen is a leading provider of cloud computing solutions and services for emerging and mid-sized businesses.

Microsoft has published Linux and FreeBSD for Azure. To migrate enterprise on-prem code to Azure is a huge competitive advantage. Mix the two, chill, and shake, and you have a new billion dollar revenue business unit for Microsoft. Elegant on-ramp for a developer to become a paying Azure customer. M &A Intelligence.

You need an efficient way to keep your customers successful, reduce churn, drive adoption, and increase net revenue retention. Secureframe allows companies to get compliant within weeks, rather than months and monitors 100+ services, including AWS, GCP, and Azure.

Subscribe now ARR (Annual Recurring Revenue) vs ERR (Experimental Runrate Revenue) ARR (Annual Recurring Revenue) is one of the most popular SaaS (Non-GAAP) metrics. Many investors laugh (and some rightly so) at the fact that software companies’ valuations are often described as a multiple of revenue.

In simple terms, the “Rule of 40” states a healthy SaaS company’s a) revenue growth rate plus b) profit margin should exceed 40%. . In equation form, Revenue Growth % + Profit Margin % > 40%. When investors place an extra premium on revenue growth, the capital allocation calculus for SaaS CEOs and CFOs changes.

We help B2B SaaS marketers turn organic search into a source of repeatable revenue through software and coaching. The platform automates the provisioning of your application to the cloud (AWS, GCP, Azure), integrating cloud ops, DevOps, and security/compliance with 24×7 monitoring and support.

Subscribe now Cloud Giants Report Q3 ‘23 Not a great signal for software this week from the Cloud Giants (AWS, Azure and Google Cloud)…After Q2 (3 months ago), the tone from the Cloud Giants around optimizations was largely: optimizations have started to ease, and net new workloads have picked up. Staggering scale already.

Large customer revenue contribution increased again sequentially to 63% of revenue, up from 57% in the fourth quarter last year. For fiscal 2022, large customers represented 61% of total revenue compared to 54% of total revenue in 2021 and 46% in 2020… Overall NDR fell, but enterprise spending remains steady.

In my 148 public SaaS companies (including most of the categories of this list but not AWS, Azure, GCP) the aggregate revenue is $185B. No matter what, the wave of enterprise spending that fueled 100 SaaS and Cloud unicorns is just getting bigger and strong. This is your time, folks. Go make it happen.

” Microsoft on Azure : “And I think last quarter, we said one, we are going to continue to have these cycles where people will build new workloads. They also are seeing AI revenue (largely compute) show up sooner than anyone else. Revenue multiples are a shorthand valuation framework. Top 5 Median: 17.2x

We now have results from the three hypersclaers (AWS / Azure / GCP). Quarterly Reports Summary Top 10 EV / NTM Revenue Multiples Top 10 Weekly Share Price Movement Update on Multiples SaaS businesses are generally valued on a multiple of their revenue - in most cases the projected revenue for the next 12 months.

We organize all of the trending information in your field so you don't have to. Join 80,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content