This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Subscribe now Azure Report - Cloud Infra Looks Good! For software, all eyes were on Azure - which grew 31% YoY (ahead of expectations closer to 29%). Azure doesn’t disclose exact Azure quarterly revenue (they disclose growth rate in absolute terms and in constant currency), but there are good estimations.

So Salesforce has now grown into the active granddad of SaaS. Nvidia, Google Cloud, Azure, etc. 1% Dilution Many faster growing public SaaS and Cloud companies aim for 2% a year dilution or less from employee grants, down from the 10%+ common at start-ups. Not moving, er growing, as fast as it once did. But how about 2026+?

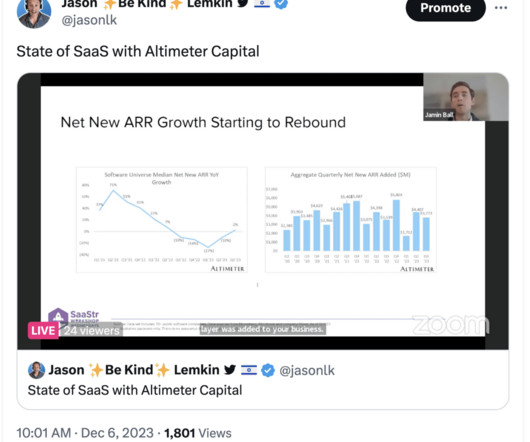

Shopify, Canva, Monday and tons of other SaaS leaders less focused on tech and startups had big years. And broader Cloud players had great years too, from MongoDB to Cloudflare to Azure, if not quite as crazy as at the peak of 2021. Altimeter: SaaS Growth Has Finally Rebounded. So 2023 wasn’t a rough year for everyone.

But fast forward to today, and Microsoft truly is a Cloud and SaaS company, with Azure and LinkedIn its fastest growing business units! Azure and other cloud services grew a record 40% and the total Microsoft Cloud grew to a $90 Billion run-rate. But the Cloud and SaaS parts of Microsoft are firing on all 8 cylinders.

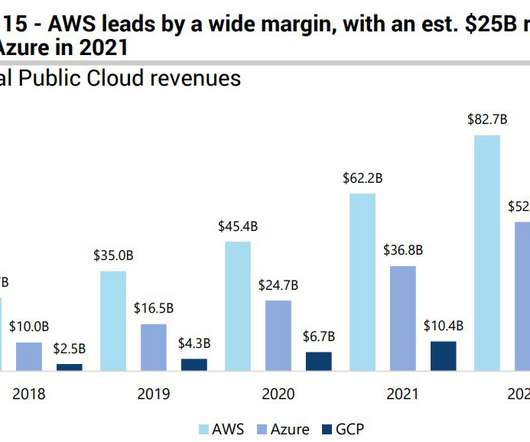

So there’s no doubt things are a bit harder for everyone in SaaS and Cloud right now. A few of us are seeing no macro impacts, but probably the biggest tell are Cloud platform giants — AWS, Azure and Google Cloud. SaaS spend is still growing. All are still growing at very strong rates. But they are still growing.

The “Rule of 40” is one of the most commonly cited valuation benchmarks in SaaS for both public and private companies. The SaaS “Rule of 40” has gained popularity due to its simplicity, requiring only two common financial metrics to be added together. What Is The SaaS “Rule of 40”?

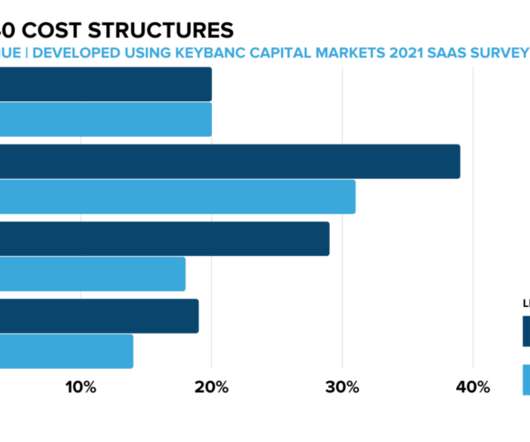

Dear SaaStr: What is The Average Ratio of Support Staff to Customer Count in SaaS? Typically support consumes about perhaps 5%-7% of your revenue at scale (excluding customer success) in most SaaS models. Another 5%-7% go to core infrastructure costs (AWS, Azure, Snowflake, etc). Have instant support while you can.

Many SaaS and Cloud leaders are down more than 50% from their all-time highs. A Covid Hangover in SaaS stocks.’ Amazon AWS, Microsoft Azure and even Google Cloud are on fire, adding insane amounts of revenue this year. The top SaaS and Cloud leaders are even accelerating at $1B in ARR, for goodness sakes!!

So follow AWS, Azure and Google Cloud. So there’s much angst and even panic with so many SaaS and Cloud public stocks down 50% or more from their peaks. Will things get worse for SaaS products themselves on a day-to-day basis? And is buying of SaaS and Cloud products accelerating, decelerating, and/or flattening out?

o this was an interesting week in terms of reading the tea leaves on what’s going on in SaaS, Cloud, the economy, and all that. Second, AWS, Azure and Google Cloud all grew nicely, and are still growing like a weed — but the growth rate slowed. So the good news is the bellwethers in SaaS are still growing at strong rates.

There are many ways to slice-and-dice public market data, but the headline one Bessemer called out is the most visceral I’ve seen: Public SaaS and Cloud companies lost $1 Trillion in market cap so far in 2022. And the number of public SaaS and Cloud decacorns has fallen from 50 to 17. Strange Days, Indeed.

So is it a downturn in SaaS or Cloud — or not? There are so many mixed signals: Unicorn product is up 2x over last year, but layoffs continue AI spend is fast and furious, with Google Cloud, Microsoft Azure, etc. Overall, SaaS leaders tied to non-tech buyers or tied to AI are still growing at epic rates.

We saw moderated consumption growth in Azure and lower-than-expected growth [elsewhere]. Segment Expected Growth Productivity 12% Office Commercial 6% Office On-Premise -25% LinkedIn 5% Dynamics 13% Intelligent Cloud 18% Azure 26% Server -3% Services -3% 2. At some point, the optimizations will end.

So we’ve had a lot of fun in our 5 Interesting Learnings profiling the top SaaS and Cloud companies at scale, from Slack to Zoom, from Shopify to Datadog, from Box to DropBox. But are AWS, Azure and Google Cloud just too big for us to learn from? Google Cloud continues its march upmarket, competing with Azure.

SaaS outside of classic “B2B’ is often holding up well. And AI is obviously on fire, pulling up AWS, Google Cloud, Azure, etc. But classic B2B SaaS is definitely in many cases seeing tougher times. So not everyone is seeing tougher times these days. Klaviyo, Toast, etc. just had very strong quarters.

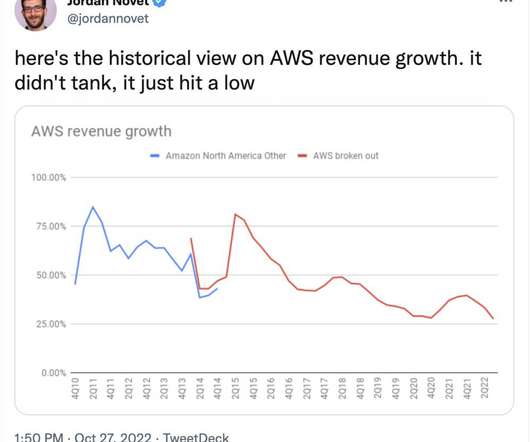

So with the latest batch of earnings out, we can get a sense of where the leaders are in SaaS. Again, epic growth but a material slowing from what AWS cited as “economic headwinds” Still — Google Cloud didn’t see a slowing of growth, and Azure’s growth rate barely budged. pic.twitter.com/a6BKk61LQR.

Zoom is growing at rates we’ve never seen before in SaaS and Cloud. But when two of the blue chips in Cloud and SaaS say darker clouds may be coming … it’s worth paying close attention. Azure and Google Cloud also saw growth begin to slow. Shopify grew 100% at $3 billion in ARR. It could just be a bump.

SaaS products and services like Pilot track the finances of 1,000s of SaaS and other startup so they’re an interesting source of hard data. SaaS and Cloud growth overall will remain strong. Shopify , Datadog, Crowdstrike , Google Cloud-Azure-AWS, Snowflake , etc. What does Pilot’s latest data say?

How about the big platform SaaS companies: Salesforce, Workday, ServiceNow, and Microsoft? ZDNet reported demand for Azure is up 775%. Everyone but Microsoft is flat. The difference in query volumes might be due to a similar phenomenon to Slack because of Microsoft’s Teams product.

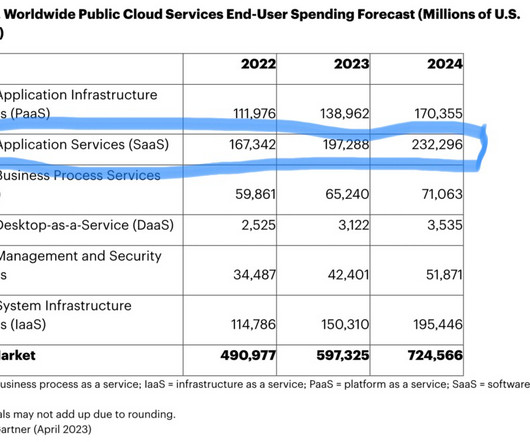

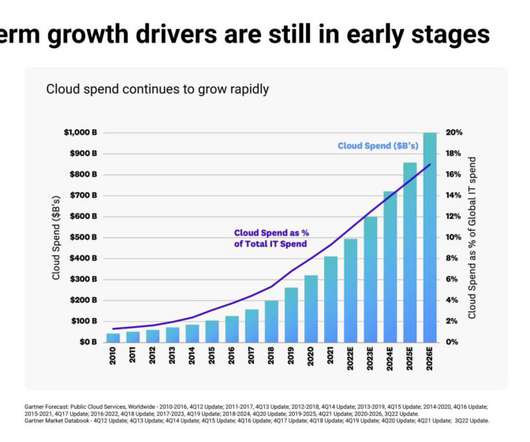

Just how fast is SaaS and Cloud growing? After polling CIOs, Gartner found that total SaaS spend will grow from $100B in 2020 to $140B in 2022: A few interesting implications and learnings: The growth in SaaS buying should give you a +20% a year boost on top of your other sales and marketing efforts. Go grab your piece.

In 2015, Microsoft wanted to help accelerate its SaaS / Cloud strategy and made a bunch of bets. Once Office 365, Azure, etc. But an experiment. They didn’t all have to work out. And in the end, have too many products is a distraction. You have to eventually close one down if it’s not a winner.

That’s pretty efficient for SaaS. #5. But many in SaaS are seeing tougher times in Europe than North America. Microsoft also reported strong growth overall and for Azure and Cloud especially. As you can see, ACV has grown ~20% over the past 2 years, from $3.4m to $4m ACV. #4. Some softness in EMEA. But ServiceNow?

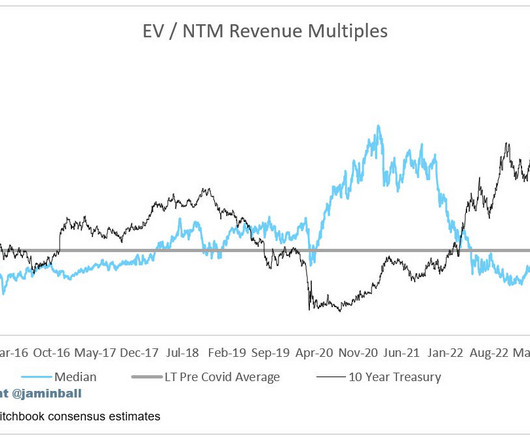

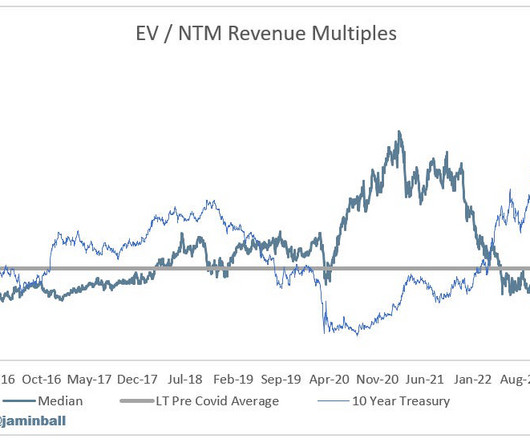

My hope is that this analysis can provide startup entrepreneurs with a framework for how to manage their businesses around SaaS metrics (e.g., It’s worth pointing out that Azure is a bit above the long term trendline, while AWS is still below (but accelerating up). net retention and CAC payback).

Focusing on smaller developers, in some ways it’s been a bit overshadowed by AWS, Azure, and Google Cloud. DigitialOcean doesn’t want to take AWS, Azure and Google on in the enterprise and doesn’t really try. Another great challenge to the idea growth has to always slow in Cloud and SaaS.

Just about everything in Cloud, SaaS and AI is firing on all cylinders at Microsoft: Azure and Cloud up +30% (!) 60,000 AI-on-Azure Customers, and Accelerating — Up a Stunning 60% Year-over-Year We all sort of knew this, but helpful to see the numbers here. #3. And at $260 Billion in ARR, what’s the #1 learning?

So we’ve talked about it often here at SaaStr, but things are just so … odd right now in SaaS. And while AWS’s growth is down a bit, it’s still at epic levels, Azure isn’t even really down, and Google Cloud is growing faster than ever.

Look no further than the massive companies pushing the public & the private market forward: Snowflake, Databricks, Amazon, Azure, Google Cloud. It’s quite possible that data products have created more market cap than any other subsegment of SaaS in the last five years.

Large SaaS and IaaS vendors are precisely that: indexes of software buyers. Amazon Web Services and Azure, the business units inside Amazon and Microsoft serve and sell to small, medium, and large companies in every major geography. Microsoft Azure. That should bode well for SaaS startups. Fortunately, it exists.

They each have some of the largest cloud businesses in the world in AWS, Azure and Google Cloud respectively. The promise of SaaS is that growth in the early years leads to profits in the mature years. It shows the number of months it takes for a SaaS business to payback their fully burdened CAC on a gross profit basis.

Currently, we offer Apache Kafka, Apache Cassandra, PostgreSQL, MySQL, OpenSearch, Redis, InfluxDB, Grafana, and M3 in more than 90 regions around the world on AWS, GCP, Microsoft Azure, DigitalOcean, and UpCloud cloud platforms. We’ll see 10,000 of the best SaaS founders, execs and VCs Sep 13-15 at 2022 SaaStrAnnual.com !

Nimble has migrated its market-leading SaaS CRM from Amazon Web Services (AWS) to Microsoft Azure. The migration enables Nimble to tap into Microsoft’s world-class Azure platform and partner ecosystem to scale.

We’ll see 2,500+ of the best SaaS founders, execs, and VCs June 6-7 at 2022 SaaStr Europa ! ChurnZero is the Customer Success platform and partner for growing SaaS and subscription businesses. From discovery to purchasing, management and cancellation, Cledara is the All-in-One SaaS management platform that companies love.

So is it possible to be too efficient in SaaS and Cloud? Many have used Digital Ocean at the cheaper, simpler version of AWS-Azure-Digital Ocean to get going fast and quickly. And if so, maybe that’s Digital Ocean. If you haven’t heard of Digital Ocean, ask your developer. It’s gotten crazy good.

The hyperscalers (AWS, Azure, GCP) are always some of the first companies to report earnings during earnings season (coming up in 2 weeks), and there’s always a read through for consumption names (meaning people believe there’s a correlation). Cloudflare is up 17%. Datadog is up 14%. Mongo is up 16%. Snowflake is up 14%.

We help B2B SaaS marketers turn organic search into a source of repeatable revenue through software and coaching. The platform automates the provisioning of your application to the cloud (AWS, GCP, Azure), integrating cloud ops, DevOps, and security/compliance with 24×7 monitoring and support.

With a PLG-heavy background, first working at Microsoft Azure and again with Atlassian, the PLG pioneers, he gives insights into leveraging PLG for the growth of your organization. Atlassian, Microsoft Azure, and Zoom are good examples of that. How PLG Evolved First, let’s start with PLG and its evolution.

In the cloud, AWS, Azure, & GCP have created about as much market cap as all the top 100 B2B & B2C publics built on cloud (Netflix, ServiceNow, AirBnb, etc). Usage & distribution, like in classical SaaS, are likely the most sustainable & repeatable. Layer : application, platform, or infrastructure?

Subscribe now Cloud Giants Report Q3 ‘23 Not a great signal for software this week from the Cloud Giants (AWS, Azure and Google Cloud)…After Q2 (3 months ago), the tone from the Cloud Giants around optimizations was largely: optimizations have started to ease, and net new workloads have picked up. Staggering scale already.

” A surprising impact of the cost-cutting may be increased margins for SaaS providers on infrastructure as their own cost reductions manifest as margin improvements. “Yes, we actually saw quite a bit of energy coming from the Azure platform this quarter. Consumption of unstructured data was up 17x year-over-year.”

DigitalOcean is growing more slowly than its mega competitors Azure, AWS, etc. Especially in a growing market, like most SaaS categories, you can both grow and fall behind at the same time. . $4B BigCommerce is growing more slowly than its $140B bigger rival, Shopify. That’s a big, big gap. More here. #2.

” Microsoft on Azure : “And I think last quarter, we said one, we are going to continue to have these cycles where people will build new workloads. Azure (excluding Azure AI) continued to decelerate, and while AWS did come in ahead of expectations, it wasn’t a blow out.

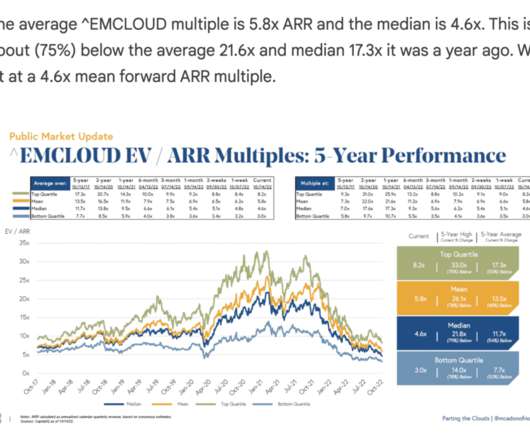

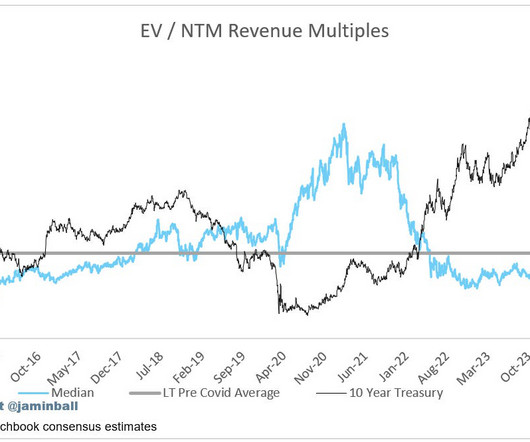

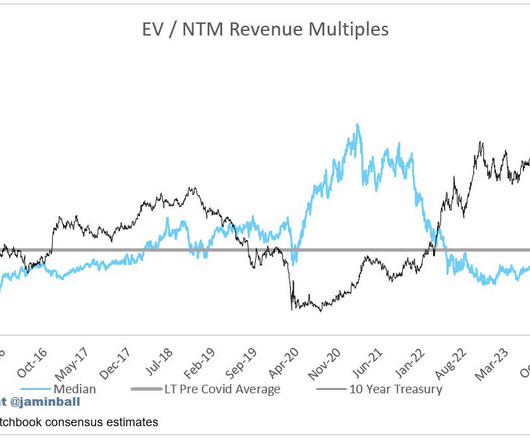

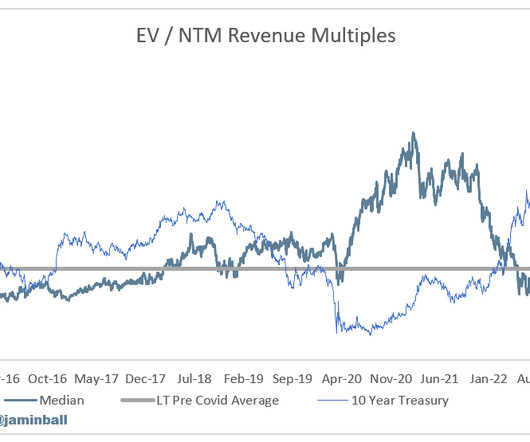

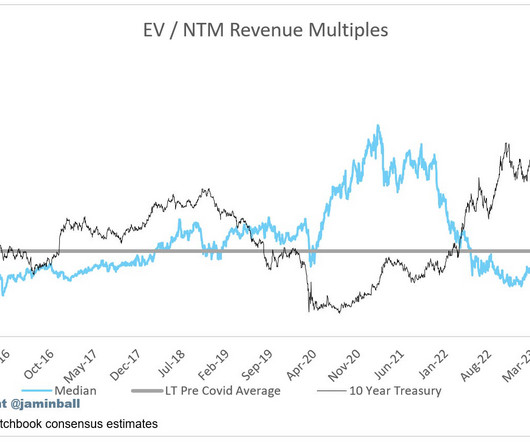

We now have results from the three hypersclaers (AWS / Azure / GCP). Quarterly Reports Summary Top 10 EV / NTM Revenue Multiples Top 10 Weekly Share Price Movement Update on Multiples SaaS businesses are generally valued on a multiple of their revenue - in most cases the projected revenue for the next 12 months.

Azure’s marketplace has over 4 million monthly visitors. million subscriptions transacted and Google’s marketplace has seen 3X growth in SaaS sales. And there’s just a lot of opportunity for SaaS providers or ISVs in general to take advantage. AWS’s marketplace has seen 1.5

Despite economic headwinds, SaaS spending continues to grow, with most companies having self-reported increasing or maintaining SaaS spending. G2 track, their proprietary SaaS spend management platform. This includes data from companies on how they utilize SaaS and their spending.

We organize all of the trending information in your field so you don't have to. Join 80,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content