This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

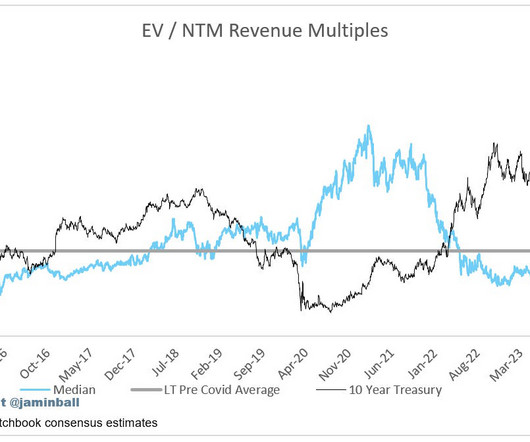

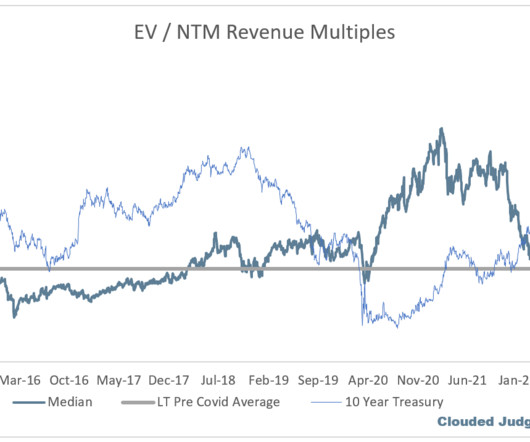

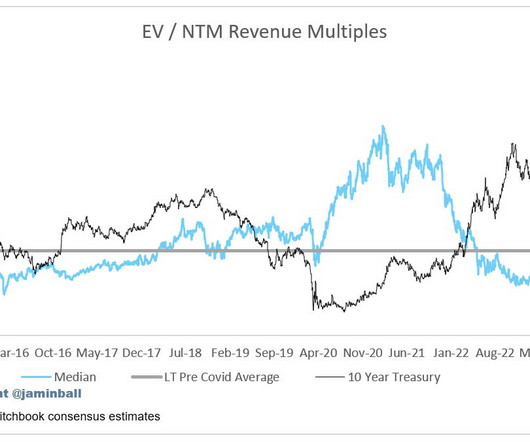

Q1 earnings season for cloud businesses is now behind us. These charts clearly show the ZIRP pull forward, the ensuing cloud cost optimizations, and then the recovery. GCP data is a bit more noisy as they don’t disclose GCP itself, but rather Google Cloud which includes GSuite.

So lately I’ve listened to a few calls from churned customers from portfolio companies. economy remains strong, the stock market is at all-time highs, AI is fueling Cloud growth, and yet … many folks are cutting their tech budgets, and especially, those that sell to startups are struggling. Not shrinking.

Every week I’ll provide updates on the latest trends in cloud software companies. And very well may lead to better “other” metrics like retention or churn. Subscribe now Share Clouded Judgement Leave a comment Follow along to stay up to date! ” It’s just too early draw any long term conclusions.

Every week I’ll provide updates on the latest trends in cloud software companies. What excites me is the strength of these platforms are reflected in new customer adds and stable gross churn. Subscribe now Share Clouded Judgement Leave a comment Follow along to stay up to date!

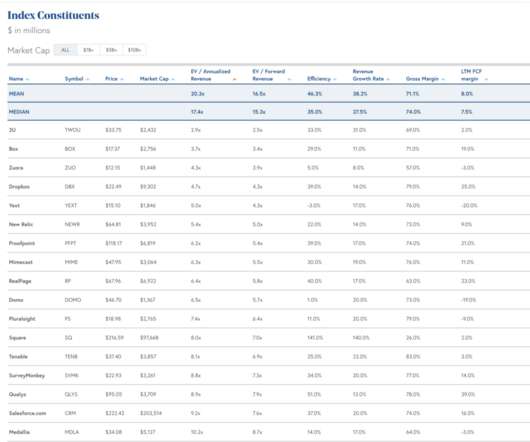

There’s a lot of info to digest, so in the sections below I’ll try and pull out the relevant financial information and benchmark it against current cloud businesses. The purpose of the detailed information is to help investors (both institutional and retail) make informed investment decisions.

5 Tips To Minimize “Churn and Burn” Behavior in Your Sales Team. “State of the Cloud with Bessemer Venture Partners” The most recent update on where the Cloud is — and is going. #2. And Most Co-Founders Are Not Equal (And That’s OK). 5 Interesting Learnings from GitLab at $250,000,000.

Unparalleled Networking Opportunities SaaStr Annual brings together thousands of SaaS, Cloud and AI executives, founders, VCs, and industry leaders under one roof across our 40+ acre campus, May 13-15 in SF Bay! VIP Networking app for B2B founders and execs attending (no service providers, sorry!) And the VCs that want to fund them!

With each passing year, more and more of our online existence becomes tethered to the cloud. But how does the cloud take shape, and what can companies do to position themselves at the heart of its growing infrastructure? Infrastructure: Reloaded for the Cloud. Pro Tips for Modern Cloud Infrastructure.

This trend has been true for a while, and now both its Service Cloud and its Platform group are bigger and faster growing than the classic CRM product we all know and use. It’s super interesting that today, Salesforce is more of a Service Cloud than a Sales Cloud. Churn Still a Bit Elevated Since Covid.

When products and services fail, customers can’t buy online or use their software, they churn, and the company suffers brand damage. Many businesses are moving their infrastructure and software to the cloud to adopt Kubernetes and microservices. Those technologies offer terrific benefits in exchange for some complexity.

Again, the latest crop of Cloud IPOs shows SMBs seem to have no limit in terms of TAM, with SMB growth at Shopify and Zendesk keeping up with enterprise, and even at Asana, SMB growth is still impressive at $250m ARR. We’ve seen this with almost all cloud leaders except Slack. Revenue growth far outpaced new customer growth.

So is it possible to be too efficient in SaaS and Cloud? Digital Ocean is only growing 16% now at $700m ARR, and churn is up and NRR down. Still Pushing ARPU Up, Churn Stable — But NRR Way, Way Down This Year Digital Ocean has small customers and tiny ARPUs, but pushing the ARPU up a bit has a huge impact on a percentage basis.

UiPath is one of the most amazing not-really-an-overnight success stories in Cloud, SaaS and software. It was founded way back in 2005 as an outsourcing company, then developed Windows software to automate scripts and more, and turned this into a powerhouse for automating complex functions integrating Cloud and on-prem. ” #5.

With 100+ public Cloud companies, it’s now a bit clearer that at least after a certain point in time, SaaS vendors have a lot of stability. Second, few SaaS companies past $20m in ARR with negative churn seem to fail. Some do fail, but they are generally ones with low NPS / high churn and other customer issues.

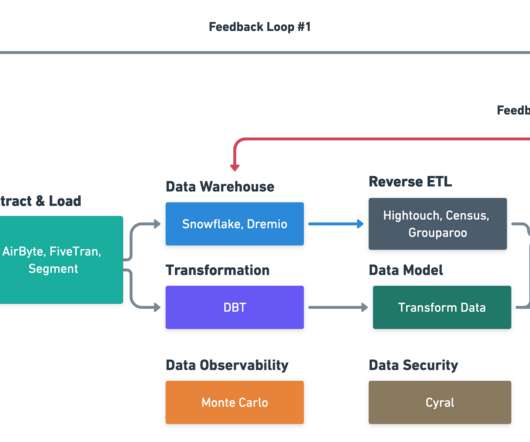

I thought it would be cloud-prem and customers driving SaaS products to use a single database. Here’s a schematic (click to enlarge) that describes how data flows with a cloud datawarehouse (CDW) fed SaaS app. A data scientist might develop a churn prediction algorithm. This may be the next shift.

running across multiple clouds. The size and power of the Cloud is just awesome these days. Breathtaking acceleration of MongoDB downloads — a good proxy for acceleration in the Cloud overall. Multi-cloud is one of their top accelerants. Multi-cloud is one of their top accelerants. Mongo shows very.

You know your new growth rate, your new retention rate, your new churn rate. Cloud is on fire. First, maybe model a material uptick in churn going into next year. It can’t hurt to model a return to a higher churn phase next year. SaaS and Cloud can’t escape the mass bankruptcies coming. Build One Now.

New Relic is one of my favorite Cloud stories. Times have changed, the Cloud has gotten a lot bigger, and there are many more vendors, including the red-hot DataDog, to grab mindshare. Do whatever you can to drive up NRR / net negative churn. Today New Relic is worth more than 10x that, at $4.3B. An incredible streak.

Q3 earnings season for cloud businesses is now behind us. Commentary from the cloud providers seems to be that the major macro headwinds around optimizations and new deal scrutiny have started to abate. ” 3 months later, what happened to those green shoots? So we’d expect the YoY growth rate to pick up in Q3 ‘23.

Q4 earnings season for cloud businesses is now behind us. The first few months of this year felt like a lot of churning in the market. We then dipped below the trendline as we hit the period of “cloud optimizations,” and things have started to rebound. net retention and CAC payback). Is Software Rebounding?

What we learned from ’08-’09 in SaaS: First, SMB churn went through the roof — as SMBs went under much more quickly and often. Anyone processing a lot of SMB and credit-card deals saw churn probably double. Assume SMB churn doubles — and quickly. Cloud is a tidal wave. Which was brutal.

Q2 earnings season for cloud businesses is now behind us. As you can see from the data below most cloud businesses beat the consensus estimates for Q2. For businesses selling predominantly to SMB customers, these benchmarks are all slightly lower given the higher-churn nature of SMBs.

Every week I’ll provide updates on the latest trends in cloud software companies. On top of that, churn and expansion tend to be quite predictable with low volatility. Subscribe now Share Clouded Judgement Leave a comment Follow along to stay up to date!

Q2 earnings season for cloud businesses is now behind us. Extra pressures around optimizations still exist, however gross churn levels have stabilized, and commentary on earnings calls suggest conversations around new bookings are starting to pick up. We will see this show up in revenue figures in a quarter or two.

Q4 earnings season for cloud businesses is now behind us. As you can see from the data below most cloud businesses beat the consensus estimates for Q4. This quarter more than half of cloud software businesses missed next quarters consensus. They do this to set themselves up to consistently beat estimates, demonstrating momentum.

If your net churn is negative, you have a superpower. Yes, these are the Best of Times in Cloud. With the Cloud being bigger than ever, the leaders in SaaS are growing faster than ever. If you fall out of hyper-growth mode, still go long. That will bail you out. Even if there is a stretch you are unfundable.

When it launched in 2011, Treasure Data’s positioning was a Hadoop-based big data warehouse in the cloud. Commoditization From AWS & Google Cloud. As a result, the logo churn went up, the NRR stopped increasing, and the deal rate decreased as the sales cycle got longer. The Platform: $0 – $5 Million ARR.

And the key difference market researchers say between Behavioral and Attitudinal loyalty isn’t what you’d expect – the churn rate. The logo churn rate is often similar in the short-term. We buy more modules, e.g. for Salesforce, the Service Cloud, and now, the Marketing Cloud. We take site licenses.

Ok so what are the top 5 learnings here for SaaS and Cloud founders? Zendesk’s churn is still a bit higher than pre-Covid, but is almost back to pre-Covid levels. So if you sell to SMBs, or a mix of SMBs and enterprise like Zendesk does (with 160,000 total customers), well … enough with the excuses on churn.

You get a complete overview of your global subscriber base; MRR, ARPU, ASP, churn and LTV are presented in a beautiful and easy to use dashboard. Our mission is to build powerful and secure cloud software for subscription businesses of all sizes, with a strong emphasis on good design and ease of use.

You get a complete overview of your global subscriber base; MRR, ARPU, ASP, churn and LTV are presented in a beautiful and easy to use dashboard. Our mission is to build powerful and secure cloud software for subscription businesses of all sizes, with a strong emphasis on good design and ease of use.

There’s a lot of info to digest, so in the sections below I’ll try and pull out the relevant financial information and benchmark it against current cloud businesses. Our cloud-based platform enables a modern and expanded approach to finance and EPM, which is sometimes also referred to as corporate performance management, or CPM.

So few Cloud software companies have had a more interesting history than UiPath. While UiPath hasn’t yet hit the 20%+ that Wall Street wants for Cloud companies at scale, importantly, it’s on the way. It took them a full 10 years to get to $1m in ARR (!). And then after that, explosion. Targeting 9.5% They were 6% the prior year. #5.

Almost every Cloud leader is growing like a weed. Churn went way up, for sure. And there’s still always at least a small but engaged group of customers looking for a better solution. From Datadog to Snowflake to Zendesk to Box to Twilio. Some are much more impacted post-Covid, like Shopify and Zoom.

Atlassian has gone almost 100% Cloud since then, and has held up nicely in the overall public markets even as others have taken bigger hits. Cloud product pricing went up 5% a year last year, and legacy server products went up much more. Transition to Cloud takes time at scale. 5%+ pricing increases help fuel growth.

So … if you just keep doing what you doing well, keep the net churn negative, then wherever you are today, should grow 2 x 5 x 3. It’s why all the Cloud leaders today are marching to $1B+ in ARR or have blown past it, from Zendesk to Twilio to Hubspot and more. That’s 30x. 10m ARR today x 30 = $300m ARR.

With the Salesforce IPO in 2004, we saw the first sign that institutional investors were comfortable with a standard set of SaaS metrics: Churn, sales efficiency , ARPU, LTV, customer acquisition cost , and so on. . The SKYY First Trust Cloud Computing ETF has grown to $3.3 Churn under 10% annually? Why Let Banks In?

Q1 earnings season for cloud businesses is now behind us. As you can see from the data below most cloud businesses beat the consensus estimates for Q1. For businesses selling predominantly to SMB customers, these benchmarks are all slightly lower given the higher-churn nature of SMBs.

Why Peter Gassner Built The Most Important SaaS Company You’ve Never Heard Of — And Turned It Into a $30B+ Vertical SaaS Cloud Giant Before founding Veeva, Gassner’s experience was marked by significant positions at major software companies. Instead of building generic enterprise software, he went all-in on life sciences.

Every week I’ll provide updates on the latest trends in cloud software companies. Here are the four data points: Net New ARR: Net new ARR added in a quarter represents new customer ARR + expansion ARR - churn / contraction ARR. Subscribe now Share Clouded Judgement Leave a comment Follow along to stay up to date!

OK Gartner is NOT a SaaS or Cloud company. About 104% Effective NRR Gartner sees about -18% gross revenue churn, but price increases add +3% back, and additional research and purchases add +19%. But — it’s one that is very important to many of us that sell into the enterprise. Gartner’s research does. #4.

In 2015, SaaS cloud-based content management tool Box went public. We restructured all of our messaging around our Content Cloud to create a simplified go-to-market message that says what it does, and does what it says. At Box, we’ve found a lot of success in getting customers to adopt new features within Content Cloud.

The rumor mill churns with whispers Salesforce will acquire Slack. Microsoft has amassed the most extensive channel for SaaS companies, and each of these vendors pushes teams to current customers, many of whom are moving to the cloud and relying on Microsoft for guidance.

Almost everything is going well in SaaS and Cloud these days — except multiples. Consistent growth, insanely high GRR, almost no churn, and deal sizes going up. Yet, the markets are down for eveyone, and Jfrog is only worth $2.2 Billion as I type this. It should be worth more. Multiples are brutal. 5 Interesting Learnings: #1.

We organize all of the trending information in your field so you don't have to. Join 80,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content