This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

He had the idea that the Cloud, not called the Cloud back then, would enable two entities to see the same transaction from their perspective. SMB Unit Economics: Why Is 6 Quarters the Right Target for SMBs at Scale? If we go back to 2006, BILL was a cloud-based company. The thing with a moat is that it takes time.

So RingCental is both an incredibly impressive SaaS and Cloud company — but also a bit of a cautionary tale. Even With a Big Enterprise Push for Years, 60% of Revenue Still From Mid-Market and SMB RingCentral closed 20 $1M+ TCV deals last quarter. But even as they push more and more into the enterprise, the SMBs still are buying.

So many curious things have happened as Cloud and SaaS companies have exploded to $2T+ in market cap. Another is a related challenge to the idea that SMBs, since they don’t pay all that much, sort of “max out” These rules are still true in many cases. As Shopify crossed $4B ARR, it actually got a bit more SMB.

With 200+ top AI demos and sessions from leaders like Perplexity, Google Cloud, GitHub, Rubrik and more, youll get the most comprehensive look at how AI is reshaping B2B. 150+ Sponsors Driving Innovation From the biggest names in cloud to the most exciting startups, our 150+ sponsors are showcasing the latest innovations in SaaS and AI.

” I’m going to talk to a bunch of Cloud CEOs in the $2m-$20m ARR range, to really hear what they are doing, how they are changing, what they are learning. 001” with Romain Lapeyre, CEO of Gorgias: 2,500+ SMB E-Commerce Customers appeared first on SaaStr. What they are seeing. The post “What Are You Seeing?

Q1 earnings season for cloud businesses is now behind us. These charts clearly show the ZIRP pull forward, the ensuing cloud cost optimizations, and then the recovery. GCP data is a bit more noisy as they don’t disclose GCP itself, but rather Google Cloud which includes GSuite.

We can see that NRR for tiny customers is probably about 100%, as it is for other SMB leaders. Again, the latest crop of Cloud IPOs shows SMBs seem to have no limit in terms of TAM, with SMB growth at Shopify and Zendesk keeping up with enterprise, and even at Asana, SMB growth is still impressive at $250m ARR.

Mike Wiacek, CEO at Stairwell, Mo Jebrini, CTO at Mashvisor, and Michael Ermolenko, CTO at Inworld.ai, discuss with Helene Ambiana, Global SMB and Startups Marketing Director at Google Cloud, how they overcame the hurdles of scaling and reached their goals. . Build an irreplaceable team .

So is it a downturn in SaaS or Cloud — or not? There are so many mixed signals: Unicorn product is up 2x over last year, but layoffs continue AI spend is fast and furious, with Google Cloud, Microsoft Azure, etc. 70% of Monday’s SMB customers are outside of tech. seeing record acceleration in growth. Billion in ARR.

Upwork is one of those products and marketplaces many of us use all the time — including Team SaaStr — but we don’t often see discussing that much as a public SaaS / Cloud company. Net net, even from SMBs, Upwork manages 100% NRR, just as Shopify and Hubspot do from SMBs. 80% SMB, 20% Enterprise.

That’s crazy growth — almost all fueled by the crazy growth of the Cloud. That’s up from $800 billion just a little while back when we took a look at Cloud Decacorns. RingCentral went from SMB to enterprise-grade contact center. No SaaS company is yet worth $1 trillion, through perhaps that is coming.

Toast’s SMB NRR is 114% today — but it took 4 full years just to get to 100%. A reminder that you don’t need to settle for sub-100% NRR from SMBs. And also that, with SMBs, it can take a while and a lot of value-add and learnings to get that NRR over 100%. And it’s the true magic in scaling SMB SaaS.

Cloudflare is one of those iconic Cloud companies most of us use, and know about as a product and vendor … but perhaps we don’t think as much about as a public company. What can founders learn from them as a public SaaS / Cloud company? We’ve seen this metric vary wildly at public SaaS and Cloud companies.

So DigitalOcean is the quiet Cloud platform that keeps on growing. Focusing on smaller developers, in some ways it’s been a bit overshadowed by AWS, Azure, and Google Cloud. DigitalOcean is growing an impressive 37% at $500,000,000 in ARR, and staying very SMB with 600,000+ customers, but still driving deal sizes up a bit.

So there are two massively different vibes in B2B and Cloud and SaaS today: Folks fighting to keep slowing growth going. Not just for consumer and SMB. Which, perhaps ironically, leads vendors to be less customer-centric. but also In high-growth AI-fueled spaces, massive competition as well. Free and Freemium are back.

If you’re selling software to SMB merchants and outside of tech like Shopify and Toast and Monday , things are pretty, pretty good, if in some ways still harder than before. If you’re selling cloud infrastructure, for the most part, growth may be down a smidge but is still strong, e.g., MongoDB.

Zoom’s SMB base has flattened after exploding like nothing we’ve ever seen before. From HubSpot to Snowflake to Asana to Monday to Gitlab to Cloudflare, the best in SaaS and Cloud aren’t just growing faster than ever. I put together this slide: No doubt, some categories are still recovering from a Covid Hangover.

SMB customers. For SMB SaaS, aim for 6 quarters of LTV:CAC, not 4 Ren adjusted the traditional benchmark because SMB customers stay longer than typically measured. ” This shift is driven by the abundance of choice in the market – thousands of cloud-based companies competing for attention.

From Asana to Zoominfo: this year’s Europa lineup is bringing the best Cloud speakers from around the globe together for two days of incredible learning and insights. There will be over 2,500+ SaaS and Cloud professionals joining us there in person. Get your ticket now and get a front-row seat when the Cloud comes to Barcelona.

Cloud is huge. Coupa isn’t as much a fintech as SMB players like Bill.com, but it’s getting there with Coupa Pay. This is a bigger task than SMB, but a huge market. It’s interesting to see Coupa present its TAM this way in terms of both customer count and market size. And ARR per deal has gone up every quarter.

What we learned from ’08-’09 in SaaS: First, SMB churn went through the roof — as SMBs went under much more quickly and often. As soon as the economy went south, SMBs started to simply go bankrupt and/or shut down. Anyone processing a lot of SMB and credit-card deals saw churn probably double.

Cloudflare is one of those iconic Cloud companies most of us use, and know about as a product and vendor … but perhaps we don’t think as much about as a public company. What can founders learn from them as a public SaaS / Cloud company? We’ve seen this metric vary wildly at public SaaS and Cloud companies.

Cloud and ecommerce may end soon, but it hasn’t ended yet. It would be so helpful to know, as the #1 leader in SMB eCommerce, and also one of the very top leaders in SaaS SMB overall. It would be so helpful to know, as the #1 leader in SMB eCommerce, and also one of the very top leaders in SaaS SMB overall.

So Okta is one of our favorite SaaS and Cloud leaders. Much, Much, Much More Efficient Than 12-24 Months Ago The story of almost every Cloud leader. But like many SaaS and Cloud leaders today, the bigger ones are still growing faster. The story is super inspiring. Then, they brought out a competing product :).

Salesforce: “We’re finally seeing slowdown now in our commerce, media, telecom, and SMB segments”. Salesforce saw demand from SMBs slow, and demandslow in retail, consumer and communications / media. But support and sales clouds remained strong, with little impact on demand. Workday: “There’s no slowdown at all”.

Jessica Alexander, Senior Director Cloud Technology & OEM Partnerships, Crowdstrike. So for the audience, cloud giants are turbocharging startup sales, and the predominant reason for this is because they’re fundamentally changing IT budgets at the customers that we’re all selling to. Rico Mallozzi, Sr.

Its definitely at least a Cloud infrastructure and applications company for SMBs: And its also a great case study of learning how to sell and market to SMBs at scale. SMB growth in Cloud and SaaS is still going strong! At $4B of revenue of scale. Million More Customers in 2020. Freemium is back!

Ok so what are the top 5 learnings here for SaaS and Cloud founders? So if you sell to SMBs, or a mix of SMBs and enterprise like Zendesk does (with 160,000 total customers), well … enough with the excuses on churn. Strive for at least 110% net revenue retention if you sell to a mix of SMBs and Enterprise.

Squarespace is self-service and SMB focused. UiPath is hyper-enterprise ($1m+ customers) and really on-prem software for the Cloud. Maybe the real point is that these 3 different software companies are so different. Procore is vertical SaaS and mid-market (and above).

We’ve recently checked in with a bunch of our Cloud and SaaS favorites as they cross $1B in ARR: 5 Interesting Learnings from Zendesk. But we’ve seen many SaaS and Cloud leaders manage to maintain consistent net retention at $1B+ ARR. But Slack’s SMBs seem to have accelerated, too, since then. Competition?

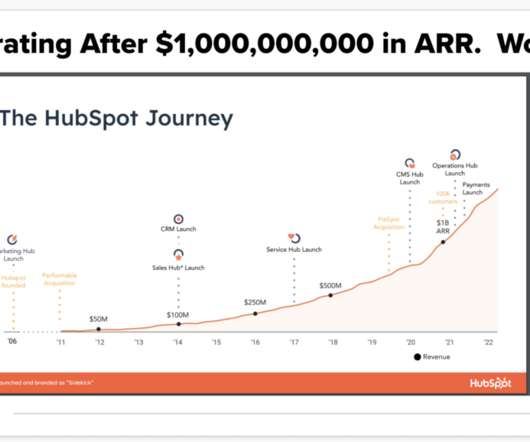

And yes, no one could have predicted the run we’ve seen in Cloud in the past few years. Today, just 2 years after that, Hubspot in a very similar space (just more SMB) and with very similar revenue, is worth $18B. These are the Best of TImes in Cloud and SaaS. Marketo IPO’s in 2013 at $700m market cap.

So look, very few, if any, SaaS or Cloud companies are out there saying times are easier now than 12 months ago. But the thing is, the underlying trends that power SaaS and Cloud are still here and as strong as ever. And there are still many categories of software and businesses just beginning to move to SaaS and Cloud.

Five9 has fully moved from an SMB product to a true enterprise one, now with well over 100 million dollar customers. #2. Some Cloud and SaaS leaders like Twilio have seen bigger NRR hits in the current macro environment, but so far, it’s been muted for Five9. 5 Interesting Learnings: #1. 134+ $1m customers, 86% enterprise.

One thing that is clear is that public SaaS and Cloud stock prices are way down. Note this doesn’t include SMB spend, it’s enterprise focused): In a slightly more dated survey, Gartner found in July 69% of CFOs plan to increase their digital spending in 2023. So are we in some sort of downturn — or aren’t we?

The Last 4 “SaaS Crashes” Barely Made a Dent in the Cloud Boomtimes. The State of Software Buying From SMB to Enterprise with G2’s CMO, Amanda Malko. When Everyone Else Has Gone Home. Is the “Covid Boost” Over in SaaS? It Depends. A Tale of Two Trends. Dear SaaStr: VCs or Founders: Who Makes More?

Let’s take a look at a few Cloud leaders that show this quantitatively: #1 Shopify’s NRR has grown from 100% to 110% as its merchant services (payments) has exploded. Pretty good for SMB SaaS. Box at $800m ARR is about 30% SMB / 70% enterprise, the inverse of Shopify. But then a lot changed in the last few years.

Battery Ventures recently put out its Software 2021 report with a ton of interesting learnings across the leaders in SaaS and Cloud. The average SMB SaaS company has $295k in revenue per employee, and $450k in the enterprise. A few top takeaways: #1. Instead, more dollars are going into the break-out leaders, not more deals.

So it wasn’t that long ago we checked in with Sprout Social, but when we did in June 2021 , the public markets were at their peak for SaaS and Cloud stocks. And Sprout Social seemed like an interesting but small SMB player. But fast forward to today, and Sprout Social is one of the winners in the current market dynamics.

SMB, Mid-Market and “Enterprise” are all about equal segments of revenue: #3. We are seeing this with more and more Cloud leaders. They have 28,000 customers total with plans starting at $99/month. #2. For Sprout Social, a $10k a year customer is a bigger customer, and the fastest growing segment, up 44%.

subscribers to the SaaStr Cloud Daily on Quora , 8,700,000+ views, and are adding thousands of new followers per week. One benefit from Cloud Daily is our community speaks and upvotes their top stories of the week. Why SMB and Enterprise Sales Have Nothing In Common | SaaStr. We now have over 200,000 (!) views · 58 upvotes.

Channel distribution represents one of the biggest and most important changes in customers acquisition for SMB SaaS startups in quite a while. One of the most interesting examples is Microsoft’s Office 365 SMB business. It’s the most successful SMB SaaS acquisition channel ever built. by Thomas Hansen.

New Relic is one of my favorite Cloud stories. Times have changed, the Cloud has gotten a lot bigger, and there are many more vendors, including the red-hot DataDog, to grab mindshare. CEO Lew Cirne, after regretting selling his first startup in the space to CA for $375m, tries again with New Relic. An incredible streak.

Almost everything is going well in SaaS and Cloud these days — except multiples. Channel model and organic approach to SMB and mid-market yields a fairly efficient Sales & Marketing motion. Yet, the markets are down for eveyone, and Jfrog is only worth $2.2 Billion as I type this. It should be worth more.

While the average Cloud stock has fallen almost 50% in 2022, Duolingo’s has stayed up, and is down just 10% in the past 6 months. The core product is very B2C, but the upgrade to paid has very SMB B2B metrics, and 80% of the revenue is subscription based. And in today’s market, that’s strong performance.

We organize all of the trending information in your field so you don't have to. Join 80,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content