This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

We go to market with our platform in three ways: Core, Pro and FinTech products. Together, we refer to our Pro and FinTech products as “add-on products.” Together, we refer to our Pro and FinTech products as “add-on products.”” trillion on trades services annually.

So, which fintechs offer the best PayFac-as-a-Service? Extra Goodies: Invoice print & mail (yes, theyll mail 100K+ invoices for you), prepaid card issuing, and tailored support for healthcare, legal, logistics, insurance, CRMs, ERPs, fintechs, SaaS and many others. But not all PFaaS providers are created equal. Lets break it down.

So in the Boom Times of later 2020 and 2021, almost every VC pushed SaaS companies to at least become a little bit of a fintech. And Fintech when you really hit it can be incredible profitable. Ok now let’s look at some pure-play Fintechs: PayPal: 47% Gross Margins. And indeed, sometimes it can be. Look at Adyen.

Treasury Prime, a leading banking-as-a-service SaaS company I’ve invested in, is hosting the Night Before Annual (Monday Sep 12) a great meet-up for Women in Fintech with Chime and Digit at one of our favorite venues, Wursthall. Sign up here. See everyone soon!!

SaaStr Founder and CEO Jason Lemkin and Partner at QED Investors Amias Gerety chat on the Fintech Beat podstream about all things SaaS, money, and what makes a great founder. Too many investors were tourists in fintech and convinced themselves that fintech margins were like software margins. Let’s dive right in.

Fintech entered the SaaS landscape with startling speed, and it’s continued to pervade every piece of our lives. CNBC Technology Reporter Kate Rooney interviews Eric Sager, the COO at Plaid, asking for his take on the state of fintech today and tomorrow. Fintech has evolved in stages. Observations and Predictions About Fintech.

Fintech coming into play has changed the trajectory of what vertical SaaS companies can be. Bolting payments or fintech onto SaaS isn’t going to work if it’s not effortless. Consumers now also expect to talk to businesses through digital means. They don’t want to call at 9 a.m. to book an appointment. on their iPads.

5 Interesting Learnings from ServiceTitan at $700,000,000 in ARR And a few other learnings we have now from those that have IPO’d in vertical SaaS or are near: Adding a payments and fintech layer can really help. At two different price points. Toast and Shopify and Bill are really more payments companies today than SaaS companies.

And yes, Shoptalk for e-commerce and SaaStr for SaaS, Money 20/20 for fintech, etc. If they are smaller events, even better. But in general, they go to the biggest ones. They go to Reinvent and Dreamforce. Not everyone goes. But a critical mass goes to the biggest in the industry. Our data shows it.

From Parabus to Ramp: The Power of Asymmetric Bets When Karim Atiyah, CTO and co-founder of Ramp, first arrived in the United States from Lebanon in 2007, he couldn’t have predicted he’d build not one but two successful startups in the fintech space.

Compete with neobanks and fintechs by offering fast money movement. SaaS Platforms: Enable Instant Payouts Use Case: SaaS platforms in gig economy, marketplaces, or fintech. Payment Processors and Fintechs: Reduce Friction Use FedNow to: Offer instant settlements to merchants. Improve cash flow visibility.

This first appeared in the monthly a16z fintech newsletter. Subscribe to stay on top of the latest fintech news. Every Company Will Spin Out a Fintech Company. TABLE OF CONTENTS.

Now new fintech infrastructure companies have made it possible for SaaS businesses to add financial services alongside their core software product. By adding … The post Fintech Scales Vertical SaaS appeared first on Andreessen Horowitz.

The Brazilian fintech company Nubank is now the largest neobank in the world, with 33 million customers and a $25 billion valuation. That valuation is already half that of Itau’s market cap , the largest public bank in Brazil, … The post Latin America’s Fintech Boom appeared first on Andreessen Horowitz.

For our last edition of the year, the a16z fintech team weighs in on the big ideas they think fintech will take on in 2021. The … The post The Big Ideas Fintech Will Tackle in 2021 appeared first on Andreessen Horowitz. Check out our big ideas from last year here. Disintermediating the banking system.

… The post El Boom Fintech en América Latina appeared first on Andreessen Horowitz. La empresa brasileña de tecnología financiera, Nubank, es ahora el neobanco más grande del mundo, con 33 millones de clientes y una valoración de 25 billones de dólares.

We are in the early days of consumer fintech — today, only 15% of Americans bank exclusively through fintechs, and Wall Street real estate remains dominated by legacy players. But that is poised to change, and we are seeing the … The post The Rise Of Many in Consumer Fintech appeared first on Andreessen Horowitz.

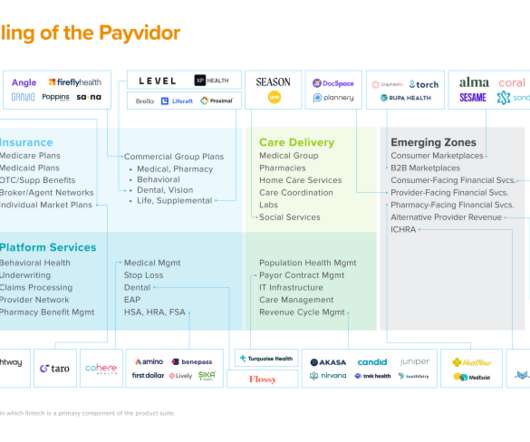

Both exhibit opportunities at the data and infrastructure … The post Payvidors, Unbundled: Opportunities in Healthcare Fintech appeared first on Andreessen Horowitz. Both are massive, regulated markets with technological adoption challenges, legacy oligopolies, and tons of customer pain – and even fear!

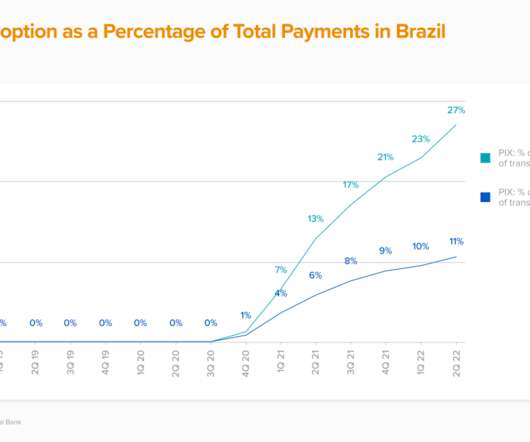

Over the past decade, the government has introduced regulatory changes … The post Brazil’s Surprising Fintech Tailwind appeared first on Andreessen Horowitz. When most people think of Brazil, the country’s golden beaches, world-class soccer players, and famous Carnaval festival spring to mind.

. “Michael is the rare CFO who also leads up marketing, which makes him the perfect person to talk us through the company’s trajectory” As the head of Intercom’s Early Stage program for Startups, the fast-growing fintech startup is one company I’ve been keeping my eye on. Short on time? Tara: We’ll be watching.

With Usio HIPAA-compliant, PCI Level 1 certified fintech payment solutions, youre not just embedding payment functionalityyoure enhancing the entire healthcare payment ecosystem. Why Medical Billing Software Companies Partner with Usio At Usio, we dont just build fintech payment solutions.

This first appeared in the monthly a16z fintech newsletter. Subscribe to stay on top of the latest fintech news. . Fintech pursues vertical banking. Bank of America got … The post New retailer payment methods; Vertical banking; Fintech x government; QR codes’ big moment?

So how many of them are like us — SaaS, Cloud software, or fintech that is SaaS-y? A lot of the Decacorns and top Unicorns are fintech related, and you might not even call them SaaS/Cloud software: And there are quite a few just below $10B, from Klaviyo and ServiceTitan at $9.5B I count about 337 Unicorns and 15 Decacorns ; and.

What we’ve actually seen is a sea change in the way that banks think about FinTech and technology in general. They’re starting to say, ‘FinTech is my innovation lab,’” says Perret. . Banks now see the value of Plaid (and Fintech overall) and leverage it to grow their businesses. .

So if you are outside of fintech and banking, you may not have heard of nCino. International Customers Are Key to Grow at Scale SaaS in regulated industries and fintech is often slower to go international than pure B2B SaaS which is simple to “grab and go” across international lines.

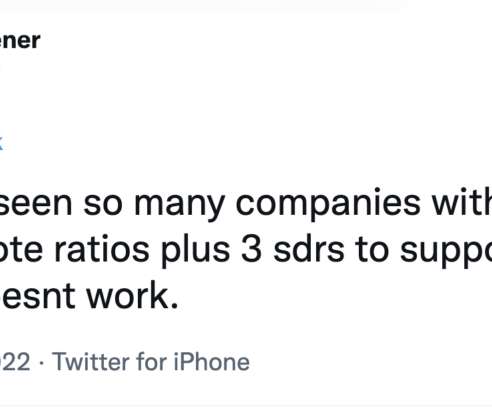

Let’s all be clear, 2021 was insane: * SPACs worth billions with no revenue * Multiples magically tripled * Fintechs with 10% GMs worth same as 80% GMs * #5 in market got same premium as #1 * Growth stage seen as free money * Seed VCs bought in $3B-10B rounds vs sell. — Jason Happy Lemkin (@jasonlk) September 28, 2022. No one cared.

This first appeared in the monthly a16z fintech newsletter. Subscribe to stay on top of the latest fintech news. . Fintech cozies up to the creator economy.

To do this, it played to its structural strengths: The UK was an early adopter of fintech infrastructure. And UK institutions continue to invest: This summer, Mastercard, Barclays and the London Stock Exchange Group announced a £1 billion fintech fund to back British growth-stage fintech companies.

Slowly becoming a fintech. Coupa isn’t as much a fintech as SMB players like Bill.com, but it’s getting there with Coupa Pay. And ARR per deal has gone up every quarter. Coupa shows you can do both even in a complex offering, and has driven up ACVs in the mid-market in particular.

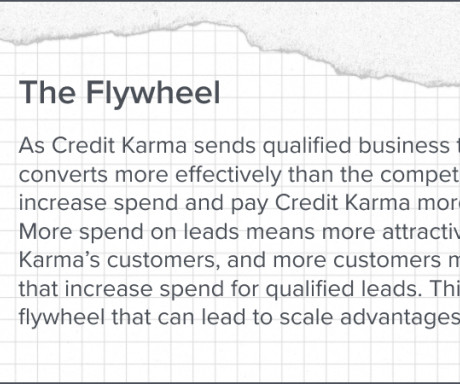

But Expensify, like Bill.com, was also early to the world of the fintech side of expense management. But both $25B+ Bill.com and now Expensify became fintechs, adding credit cards and much more. Fintech is the engine of growth at scale. And Bill even acquired Divvy for $2B.

Imagine you are the founder of a fintech company that’s identified a massive broken market. That … The post Bat Out of Hell: Identifying Your Durable Advantage in Fintech appeared first on Andreessen Horowitz.

You can’t always rush a fintech product. The payments / fintech side of Bill took a decade to come together. But they couldn’t rush it. So they let folks use the platform the way they wanted, from paper checks to fax and more. #2. It was much more than adding an API, especially at scale.

Our focus is on enterprise software and commerce infrastructure such as fintech, and logistics. As an early team member, Andrew has been part of scaling Activant alongside its portfolio companies and established the firm’s fintech focus. What’s your sweet spot for investing — check size, stage, type of deal?

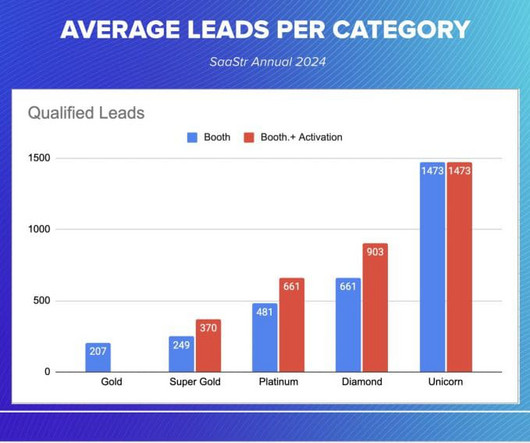

Compared to another leading tech event 2 weeks later, it was night and day in favor of SaaStr Annual” Public Fintech: “Our team buzzed about the event and the people they were able to meet in a short amount of time. ” Public Fintech #2: “Our sales team walked away with over 100 qualified leads.

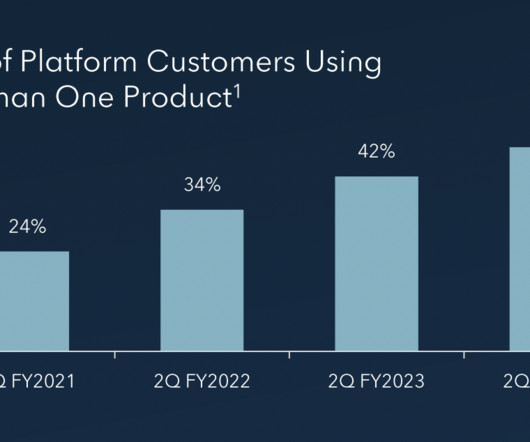

Going global is tougher in payments and fintech. Going international takes a lot of work in many fintech SaaS. Sellers using four or more products generated more than 10x the gross profit on average in 2021, compared to sellers only using one of Square’s products. #3. Only 9% of Square’s revenue is international, but going up.

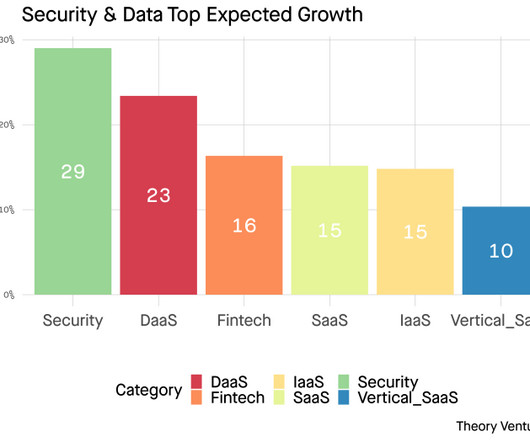

Fintech & SaaS (horizontal) average ten percentage points fewer expected growth. The fastest growing software category in the public markets is security. Data follows. Security companies as a group average 29% expected revenue growth in 2024, compared to 23% for Data (or DaaS which stands for data-as-a-service).

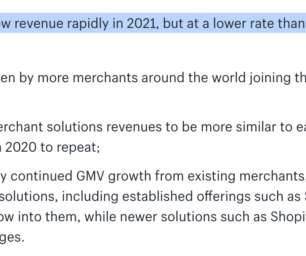

Now clearly a fintech with a layer of software underneath. If you can add a fintech layer to your SaaS product, magic can happen. In 2021 Shopify’s payments and merchant services have pulled even further ahead of its software revenue.

5 “The Non-Obvious things about the Future of Fintech with Plaid’s COO” Plaid’s COO joined SaaStr to talk about the future of fintech. #6 #4 “Why Zoom’s Founder Went Solo & How Being an Engineer Helps You be a Better CEO” A short look back on why Eric went solo. #5 I loved it.

The Non-Obvious things about the Future of Fintech with Plaid’s COO. Fintech founders are experts on their business and target audience, but they generally don’t know nearly as much about banking especially when it comes to compliance, fraud, and risk. Eric Sager, COO @ Plaid & Kate Rooney, Technology Reporter, CNBC.

Everything just diverged from economics that really made sense: Fintech companies and pseudo SaaS companies with low gross margins stiill had to pay the same or similar commissions as high margin SaaS companies to stay competitive. This wrecks the unit economics.

TABLE OF CONTENTS Generative AI is Coming for Insurance Because underwriting, selling, and servicing rely so heavily on humans processing large quantities of written or verbal communication, existing tools have struggled to properly automate these services and materially impact loss … The post Generative AI is Coming for Insurance (May 2023 Fintech (..)

Bancorp, and 15 service … The post What’s Next for FedNow (August 2023 Fintech Newsletter) appeared first on Andreessen Horowitz. After four years of development (and 10 years since its announcement), the Fed launched FedNow this past July with 41 banks, including JPMorgan Chase, BNY Mellon, and U.S.

We organize all of the trending information in your field so you don't have to. Join 80,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content