This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

in revenue. Then, in 2017, with around $50M in revenue, BILL added payment capabilities. Businesses take time to adopt, unlike consumers who joined TikTok by the tens of millions. If you screw up one payment, customers are going to be angry. Be prepared for that if you move peoples’ money as a business.

But what has changed in the last five years is that you have all now embedded financial services (Stripe, etc.) Consumers now also expect to talk to businesses through digital means. Now, there’s payroll processing, payments online or in person, recurring billing, and so on — effectively expanding the market and TAM.

In this episode of PayFAQ: The EmbeddedPayments Podcast, host Ian Hillis welcomes Matt Downs, President of Worldpay for Platforms, to discuss software-led payments predictions for 2025 and beyond. This cycle promises significant advancements for end-users and software platforms alike.

So theres a theme Ive been working on with all the SMB-focused founders I work with and have invested in: # 1. The Goal for SMB SaaS is 100%+ NRR. Easy in enterprise, hard in true SMB. # However, SMBs have a certain level of inherent churn. And then your NRR will cross 100% with SMBs. Thats often 3% a month or so.

ServiceTitan, the operating system for the trades, continues to scale impressively, with $772M in FY25 revenue, $800m+ ARR and a clear path to $1B ARR. Net Dollar Retention >110% and GDR of >95%: The Power of Being a True Operating System ServiceTitans NRR consistently exceeds 110%, even with SMB-heavy customers. Thats rare.

So in theory, SMB SaaS is better than enterprise, at least 9 times out of 10: Deals close much faster. But beyond all the other Pros and Cons of SMB vs enterprise, there’s one looming issue with SMB SaaS: Churn. SMBs go out of business, and quickly. SMBs pay monthly, and often scrutinize every expense.

They prioritize revenue growth, market share and profit maximization differently. Maximization (Revenue Growth) - maximize revenue growth in the short term. Many mid-market software companies price with the goal of revenue maximization, negotiating for the highest possible price in each sale.

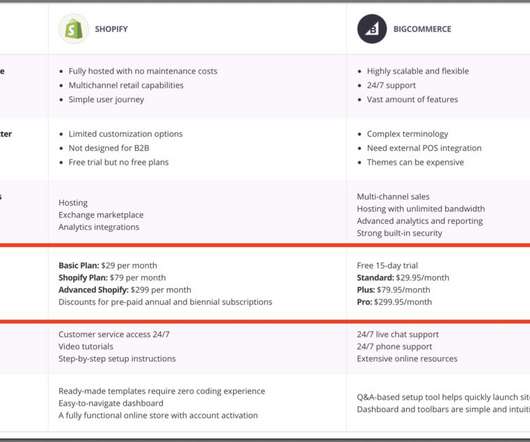

But, there are still many interesting things we can learn from Shopify, especially since it sells to so many SMBs, has been late to go upmarket, and combines a payments/fintech element with pure SaaS. So are you sure your trial needs to be so short? Subscriptions can fuel payments and merchant revenue.

Over $500,000 revenue per employee. Monetizing ecommerce via subscriptions, but not paymentprocessing. Billion in GMV processed, up a stunning 91% from 2019. But in contrast to Wix and Shopify, it doesn’t keep much of the revenue from merchant services itself. 30% of its revenue outside the U.S.

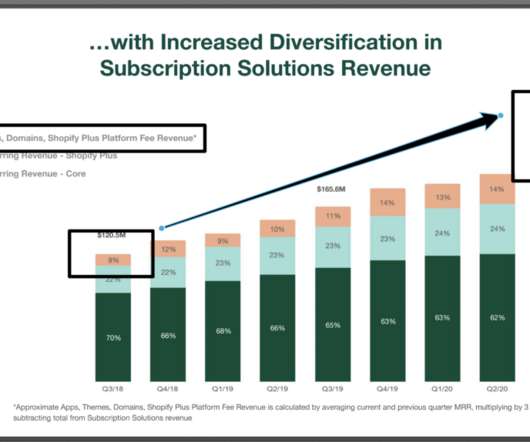

That’s not just pretty epic growth at almost $7 Billion in revenue, it’s one heck of a comeback. But a Smaller and Smaller Percentage of Revenue. From a business model perspective, Shopify has in essence been a fintech and merchant product first and a SaaS product second for quite some time. A tough transition.

But launching your eCommerce store is just half the equationaccepting payments efficiently and effectively is a whole different ball game. On the surface, it seems effortless, with customers only taking a few seconds to initiate and complete payments. The eCommerce payment solution infrastructure involves several key players.

It’s done it by going more upmarket, and better monetizing partners and services. Having said that, the average ACV here is $14,615 … so that’s at the high end of a traditional SMB spend, which probably accounts for the high NRR. Driving existing customer revenue up more than new logos.

Well, fast forward to today and it’s truly an SMB powerhouse. How is SMB SaaS doing today? Both Bill and Shopifty have morphed over the years from almost pure SaaS companies to paymentsplatforms built on top of a SaaS core. The rest of the growth is from its Divvy platform, which is bought in 2021 for $2.5

So one of SaaStr Fund’s latest investments is Mangomint, a vertical SaaS platform for spas and salons. And yet, today Mangomint is at eight figures in ARR, growing 100%+, with 110% NRR from SMBs. You really have to do it all now to build a true platform for SMBs: software, payments, payroll, marketing, workflow and more.

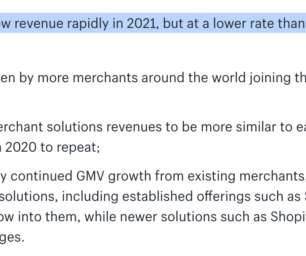

Shopify’s first quarter revenue: Q1 2021: $989 million Q1 2020: $470 million Q1 2019: $321 million Q1 2018: $214 million Q1 2017: $127 million Q1 2016: $73 million Q1 2015: $37 million Q1 2014: $19 million Q1 2013: $9 million. When you add in payments, i.e. merchant services, NRR for 2018+ is about 110%, based on the below new chart.

Bill.com has become an SMB powerhouse, with 120,000+ customers and a stunning $25B+ market cap. Bill.com had to develop a network that today has millions on vendors processing bills and payments on it. So they let folks use the platform the way they wanted, from paper checks to fax and more. #2. But it paid off.

And with that, it seemed a good time to dig in with one of the great SMB leaders Bill. With a super impressive 111% NRR from SMBs. From SMBs. A reminder and a challenge to not settle for < 100% NRR from SMBs. Fast forward to today, and only 20% of its revenue is from software subscriptions.

Now they’ve scaled to $200m+ ARR growing 38% selling just to 100,000+ SMBs, solving a hard problem (i.e., automating the back office and payments and billing for SMBs), and doing it with 120%+ NRR. 121% NRR from SMBs — up from 110% at IPO. Making more and more money on each payment. Pretty impressive.

SMB SaaS has a lot going for it: – Millions of them – Short sales cycles – Easier compete. But, it's often hard to get to $100m ARR selling just to SMBs. sell just to SMBs pic.twitter.com/Po1I2aMaBK. So many VCs and others have gotten more and more excited about SMB SaaS. Millions and millions more.

They are at 2,000 customers, a stunning 40% revenue and 46% billings growth, at $700m in ARR. Network effects are real in Spend Management. Coupa isn’t as much a fintech as SMB players like Bill.com, but it’s getting there with Coupa Pay. This is a bigger task than SMB, but a huge market. And a few bonus notes: 6.

SMB customers. Your suppliers might actually be your customers 30% of Bill.com’s core revenue comes from suppliers making payment choices, completely reframing their TAM calculations. “It’s a lot of human capital to make it work across 50 states and a trillion dollars of revenue.” From Zero to $1.4

They want a slick site that does more, from eCommerce to payments to marketing and more. And SMBs are back in SaaS. That’s the power of recurring revenue. eCommerce and Business Tools Are Key Drivers to Accelerating Growth. Efficient at SMB marketing — an ~8 month CAC. But much lower in Payments.

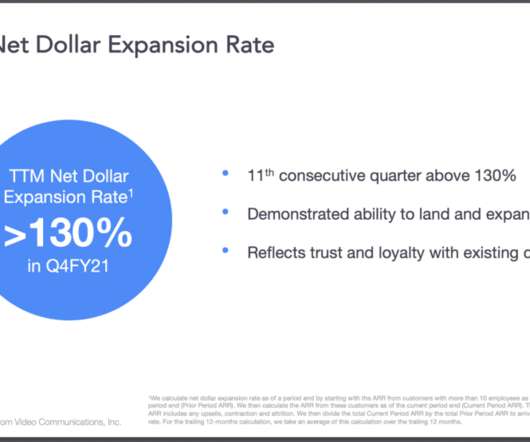

So when we first started writing about Bill.com at its IPO , it was a sleep SMB accounting product. And its payments network to roll out. But yes, it’s the most incredible SMB growth story in SaaS we’ve ever seen. Don’t let anyone tell you it can’t be done with SMBs. #2. 131% NRR.

Gorgias, an eCommerce customer service platform, discovered that their customers’ main pain points were a lack of centralized customer support channels and poor integrations. Platform: Will any integrations or partnerships be beneficial or a “must” to attract customers? Firstly, payment should be easy for customers.

SMB sales (most of Toast) is very tough to do without a highly efficient and effective sales force. At least 20% of your customers from referrals and second-order revenue. #4. Many SMB leaders have to get very, very good at outbound because of the limited deal sizes. 20% of new customers / locations come from referrals.

EmbeddedPayments have become a popular initiative among vertical specific software companies looking to deliver a more seamless customer experience, introduce new revenue into the business, and stay competitive in today’s digital world. How do they think about attaching payments to those existing customers?

GRR of 86% and NRR of 119% are very impressive for SMBs … although they only count customers with 5+ seats. Still, 119% NRR from SMB is world-class even for 5+ seats accounts and sometime to strive for if you have similar sized customers. #4. But after adding more credit cards and payments, and coming out of Covid … boom!!

In particular: Hybrid SaaS with payments and fintech usually has far, far lower gross margins than pure software. See, e.g. Shopify, whose blended gross margins with payments even at its scale are still less than 50%. Non-Recurring Revenue Doesn’t Count, At Least Not as Much. Pass-Through Revenue Simply Doesn’t Count.

Adding PayPal to your list of accepted payment methods opens up a range of benefits for you and your merchants alike. Benefits for merchants Increase conversions – The primary advantage of adding PayPal, Venmo, and Pay Later as payment options is that they enable merchants to boost conversions.

Embedded Finance is more than just a buzzword; it represents a fundamental shift in how financial services are delivered and consumed today. Ian Hillis, Head of Growth at Worldpay for Platforms discusses this new term and what the opportunity may await software providers on our latest episode of PayFAQ: The EmbeddedPayments podcast.

Weave started off as a dental ERP and comms platform (including VoIP / phone), and then expanded beyond that as it scaled. While these aren’t great metrics if Weave was enterprise, they are still solid for SMBs. Many SMB SaaS companies struggle to hit 100% NRR and 80% GRR. A fairly standard SMB price point.

110% Net Revenue Retention and 8 2% Customer Retention from 81,000+ SMB Customers. Bill.com sells to very small businesses that do churn at a higher rate. But that also proves that’s no excuse to drop below 100%+ net revenue retention. Bill.com manages 110% Net Revenue Retention on 82% Customer / Logo retention.

One leader in SMB commerce is Lightspeed Commerce, founded way back in 2005. And their mix of software, payments and hardware revenue drives up the total deal size — but puts a lot of pressure on margins. 39% of their revenues from software, and going down. Driving up ARPU at scale key to growth with SMBs.

No one knows this better (or more intimately) than a software company Chief Revenue Officer (CRO). Adam Tesan, CRO at Worldpay for Platforms, is a seasoned executive leader with decades of experience in sales, marketing, and revenue in the software space. It was an Embedded Finance play starting with payments. [It

Its growth has been more slow-and-steady than traditional rocketship, crossing $69m in Q4 revenues (let’s call that $280m+ in ARR, so soon to be $300m) — growing 17% a year by revenue, and 10% a year by customer count. That is a similar revenue growth rate to Salesforce’s core CRM product. A few learnings: 1.

In 2023, the Embedded Finance market was valued at $73 billion and projected to grow to $523 billion by 2032, growing at a compound annual rate of 24%, according to a recent report. It’s still early days for Embedded Finance, but the preliminary statistics coming out of this space are rather significant.

Fast forward to today, and we can add an important nuance to that: a second core product not only helps you grow faster at scale (a bigger TAM), but it drives up NRR and more revenue from your existing customers. Pretty good for SMB SaaS. Box at $800m ARR is about 30% SMB / 70% enterprise, the inverse of Shopify.

What we learned from ’08-’09 in SaaS: First, SMB churn went through the roof — as SMBs went under much more quickly and often. As soon as the economy went south, SMBs started to simply go bankrupt and/or shut down. And even before they did, panic set in in businesses with no cash reserves. functioned.

In the latest episode of PayFAQ: The EmbeddedPayments Podcast, host Ian Hillis sits down with Candice Raybourn, Head of Partner Activation at Payrix and Worldpay for Platforms, to discuss the crucial topic of PCI compliance. What is PCI DSS? Candice explains the basics of PCI DSS. The shift to PCI DSS 4.0 is essential.

With nine figures in revenue, Ariel and SaaStr founder and CEO Jason Lemkin talk about all things Navan, rebranding when you have brand equity, building B2B software for people, pricing and business models, and much more. Before Navan, there were different apps for managing expenses, events and meetings, payments, etc.

ContaAzul is a business management platform for small businesses created in Brazil. Its focus is on helping companies handle financial routine and streamlining processes related to accounting, banks, stock, and electronic invoicing, among others. Vindi is a PCI-certified online paymentplatform for recurring billing.

If Momentive / SurveyMonkey had stayed 100% self-serve and low end, it likely wouldn’t be growing much at all, with self-serve revenue now only growing 7%. Far forward to today, 1/3 of its revenue is sales-driven, but it’s the core growth driver, up 35%. #2. It’s not always best to force annual payments.

The SMB segment of Zoom has stopped growing, so going from ~0% growth to 7% growth actually might end up being huge. Merchant payments have become the bulk of not only its revenue, but importantly, have been growing twice as fast as SaaS revenues). Because with those apps, we see second-order revenue spread quickly.

SaaS is about creating long-term value for your customer, and being compensated appropriately for that value as a business. Learn actionable monetization tips from a Product/Growth operator turned VC. This is a mobile solution for SMB’s to send an invoice and get paid. Want to see more content like this? Hi, everybody.

We organize all of the trending information in your field so you don't have to. Join 80,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content